Paytm Payments Bank’s shutdown is not an isolated event but part of a larger crisis facing India’s payments bank model

The sector is caught between soaring UPI volumes and weak monetisation, while restrictions on lending continue to squeeze profitability

As regulatory and business pressures intensify, the industry is being forced to reinvent itself beyond payments

It’s over for Paytm Payments Bank. But this isn’t just about Paytm.

Years back, several payments banks like Aditya Birla Payments Bank, Cholamandalam Investment and Finance Company, Vodafone m-pesa Ltd, and others had also felt the heat and shut their shops.

1 August 2026

Get the latest issue of Outlook Business

However, exceptions are always there. Some players like Airtel Payments Bank, India Post Payments Bank, Fino Payments Bank, and others have managed to stay afloat. Their resilience has largely been supported by strong parent ecosystems.

On April 26, the RBI’s decision to cancel Paytm Payments Bank license has put the spotlight back on the long-simmering debate around the concept of payments banks in India. The episode has exposed the fault lines of an entire regulatory experiment.

The timing of Paytm’s exit becomes even more important for India’s digital payments ecosystem. Data released by the National Payments Corporation of India (NPCI) shows that UPI processed over 22.6 billion transactions in March 2026.

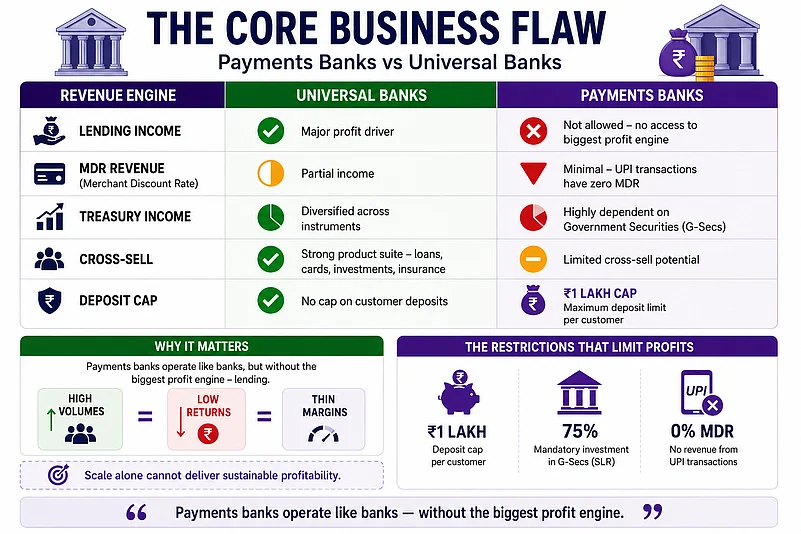

Yet, under the zero MDR (merchant discount rate) regime, the surge in volumes has translated into little revenue for intermediaries like paytm banks. At the same time, payments banks cannot lend, the most profitable arm in banking business.

Advertisement

The whole scenario results is a structural squeeze: high volumes, low returns and limited levers to change either. “The system functions as a utility which operates with high transaction volumes while maintaining low profit margins,” says Siddharth Maurya, Managing Director, Vibhavangal Anukulkara Pvt Ltd.

While governance failures triggered Paytm’s exit from the payments bank model, the question remains the same even after years and incidents — whether it was ever built to last.

The Fall Wasn’t Sudden

The signals for shutdown of Paytm Payments Bank had been building for years. Regulatory concerns around compliance (specifically KYC norms), data integrity and related-party transactions had surfaced well before the final action.

Advertisement

And once again, RBI’s final call reflected how payments banks operate. Unlike traditional lenders, they function under tighter regulatory guardrails, where lapses carry far greater consequences.

As Maurya points out, “The system operated with design integrity, but the problem arises when expectations don’t align with its structural limits”. The regulator, when introducing payments banks in 2014, prohibited them from loan business because it wanted to create a secure system which would allow people to access financial services.

“The objectives of setting up of payments banks will be to further financial inclusion by providing small savings accounts and payments/remittance services to migrant labour workforce, low-income households, small businesses, other unorganised sector entities and other users,” the guidelines read.

But it designed its profit model to generate revenue through transaction fees and float income while using cross-selling as an additional revenue stream. The assumption that these things would produce bank returns at conventional levels created an “operational error”.

This mismatch has become harder to manage as these institutions scale. Payments banks were built to onboard customers quickly and enable frictionless digital transactions. But as user bases expanded into the millions, maintaining strict compliance across accounts became increasingly complex.

At the same time, the cost of staying compliant has been rising. Investments in KYC processes, monitoring systems, and regulatory reporting have increased significantly, even as revenue streams have remained constrained. Industry estimates suggest that cost-to-income ratios for payments banks often exceed 100%, meaning operating expenses outstrip earnings.

Even external factors have compounded the pressure. Kunal Jhunjunwala, founder of airpay highlights returns on government securities — where payment banks must invest a large share of their deposit –- have softened after the RBI cut the repo rate by 125 basis points in 2025.

“For payments banks, this is not just a rate cycle, it directly compresses income with no lending buffer to offset it,” he says. In effect, even as compliance costs have risen, income has come under pressure.

The No-Lending Problem

While payment banks have no loan book, their entire interest income rests on a falling rate curve. “They are trying to operate like banks without the biggest earnings engine that banks typically rely on,” says Jhunjhunwala.

Payments banks typically operate with net interest margins (NIMs) of around 2-3%, according to industry estimates, far below the 7-9% margins reported by small finance banks. At the same time, around 70-75% of their deposits must be parked in government securities, limiting their ability to generate higher returns.

The pressure has intensified as interest rates softened. Since early 2025, the RBI has cut the repo rate by 125 basis points, bringing it down to 5.25% by April 2026. For payments banks, which depend heavily on returns from government securities, lower rates directly compress earnings.

Unlike universal banks, where floating-rate loans can be repriced upward as rates shift, payments banks have no such cushion. According to Jhunjhunwala, the rate sensitivity is entirely one-sided.

“The 100 basis points movement in government security yields can materially alter treasury income for payments banks. Rising yields can lead to mark-to-market losses, while falling yields may boost short-term treasury gains but create reinvestment risks over time,” says Loveena Kansal, EVP & Business Head, MegaCorp Ltd.

This shows that the 125-basis-point cut cycle hitting an institution with no lending offset is not a monetary policy event; it is a structural income-erosion event.

The UPI Revenue Trap

In March 2026, UPI transactions volumes grew 24% year-on-year, with a daily transaction value of ₹95,243 crore, according to NPCI data. A large part of this growth is coming from tier 2 and 3 cities, contributing nearly 45% of total transactions. But handling rising payment volumes doesn’t work much for payments banks because scaling is only turning into a profitability trap.

Under the zero MDR model, payment banks earn nothing on this volume. And ironically, this is precisely the customer base payment banks were built to serve and the segment generating the most zero-revenue UPI traffic.

“Payments banks participate in UPI as member banks but do not own the rail. Their retail customer base transacts almost entirely through UPI for person-to-person and merchant payments. IMPS, where fee recovery is possible, handles bulk and institutional flows but accounts for only a fraction of total volume,” says Jhunjhunwala.

The problem becomes even sharper at the customer level. For instance, average balances in payments bank accounts typically remain between ₹500 and ₹2,000, limiting the float income these institutions can generate from deposits. At the same time, the absence of merchant discount rate (MDR) on UPI transactions also wipes out a key revenue stream from payment processing.

The float income generated from such minimal balances falls short of meeting technology, compliance, and operational costs, according to Maurya.

So, this gap widens with every billion new transactions added. In short, more UPI transactions, more spending on infrastructure, servicing, and compliance.

Besides UPI transactions, fee income from remittances and bill payments exists but it also compresses as digital corridors mature. The only income that does not face this structural erosion is “recurring distribution revenue from insurance and financial products”, and that pipeline is not yet the industry's dominant revenue contributor.

The Search For A Sustainable Model

For payments banks that are still operational, survival increasingly depends on becoming something more than just a payments intermediary. Industry executives say the standalone digital payments model is no longer enough to sustain profitability, especially in a market where transaction monetisation remains weak and regulatory restrictions continue to limit revenue flexibility.

The institutions that have managed to stay afloat are largely those backed by deeper ecosystems like telecom networks, government infrastructure, or large distribution channels that can absorb thin margins over a longer period.

That advantage is visible in the sector’s remaining survivors. Airtel Payments Bank benefits from telecom-led customer acquisition and merchant reach, while India Post Payments Bank leverages one of the country’s largest physical distribution networks through the postal system. These ecosystem advantages lower customer acquisition costs and create opportunities to cross-sell financial products beyond basic payments.

“The top players will either break even or generate modest profits because they are supported by parent ecosystems and additional revenue streams such as remittances,” says ]Maurya. For smaller standalone players, however, the economics remain far more difficult.

This, according to experts, has pushed the sector toward a new playbook called “monetising customers outside the payments layer itself”.

According to industry estimates shared by MegaCorp, transaction-linked revenues still account for nearly 50-70% of industry income, while recurring streams such as subscriptions, insurance distribution, commissions, and wealth products contribute a much smaller share.

The challenge is that payments banks continue to operate in a high-volume but low-ARPU environment, where servicing costs remain elevated.

“Payments Banks in India have achieved scale and inclusion, but not economic viability. They now need to evolve into full-stack financial distribution platforms with monetisable ecosystems,” says Kansal.

That shift is already visible across the sector. Payments banks are increasingly partnering with NBFCs, insurers, and wealth platforms to distribute small-ticket loans, insurance products, and investment services without directly taking lending risk onto their own balance sheets.

Industry executives believe such partnerships could become one of the few scalable revenue pools available under the current regulatory structure.

Kansal estimates that even limited balance-sheet flexibility or small-ticket credit participation could significantly improve profitability metrics for the sector. At the same time, executives argue that customer monetisation needs to improve sharply for the model to remain viable.

Estimates suggest average revenue per user may need to rise two-to-three times from current levels, while cost-to-income ratios, often above 100% today, would need to fall substantially through automation and lower compliance costs.

But even these changes may not fully solve the problem unless the regulatory framework evolves alongside the business model.

Some experts believe the long-running debate around MDR on UPI transactions could return to the spotlight as payment infrastructure scales further. Others argue that regulators may eventually need to reconsider deposit caps or allow limited forms of credit participation if payments banks are expected to remain commercially sustainable.

For now, though, the industry sits at an uncomfortable crossroads. Payments banks succeeded in accelerating digital inclusion and pushing millions of first-time users into formal finance.

But after Paytm Payments Bank’s exit, the sector is once again confronting the same question it has struggled to answer since inception: whether scale alone can keep the model alive.