A Dalal street veteran and ardent follower of Warren Buffett, Raamdeo Agrawal has said in the past that the investment mantra of Oracle of Omaha has been a guide for him. And keeping in line with Buffett’s investment strategy of saying ‘no’ to the stocks that don’t fit his criteria, Agrawal in his latest wealth creation report has suggested investors walk away from companies in the hyper-growth mode if valuations hit exuberant levels.

In his 23rd Wealth Creation report, co-founder of Motilal Oswal Financial Services (MOFS), Agrawal says “In the short and medium term, all companies showing earnings growth tend to get rewarded by investors by way of rising stock prices and market value. However, our model suggests that all growth is not good.”

Agrawal explains that if a company’s RoE remains below cost of equity for long, then high growth actually detracts firm value, as the company has to raise significant levels of capital from its equity holders to fund its growth.

1 August 2026

Get the latest issue of Outlook Business

“If a company’s RoE is exactly equal to its cost of equity, then no amount of growth adds any value whatsoever,” adds Agrawal. He asserts that growth adds positive value only when RoE is higher than the cost of equity.

However, sustaining RoE above cost of equity is a challenge for companies. The MOFS report processed the 20-year data of the top 1,500 listed companies to find that on an average, 52% of India Inc has RoE lower than 13% (cost of equity). Only 19% of companies manage RoE of over 25%.

Advertisement

Consider this. There were 188 companies with a net profit above Rs.200 million in 1998. Of these, 136 companies had RoE greater than 13%. But, that the number of companies with RoE above 13% dropped quite steeply in the next seven to eight years and gradually all the way down to a mere 22 by 2018.

RoE and earnings growth are key drivers of value but like RoE sustaining a high earnings growth momentum beyond five to six years is an uphill task. For instance, in 2003, out of the 283 companies with a net profit of above Rs.200 million, 103 clocked annualised net profit growth of more than 25% in the first 5-year period, i.e., 2003 to 2008. Following this, the number of such companies dwindled to 13 in the second 5-year period (2008-13) and to zero in the third (2013-18).

Advertisement

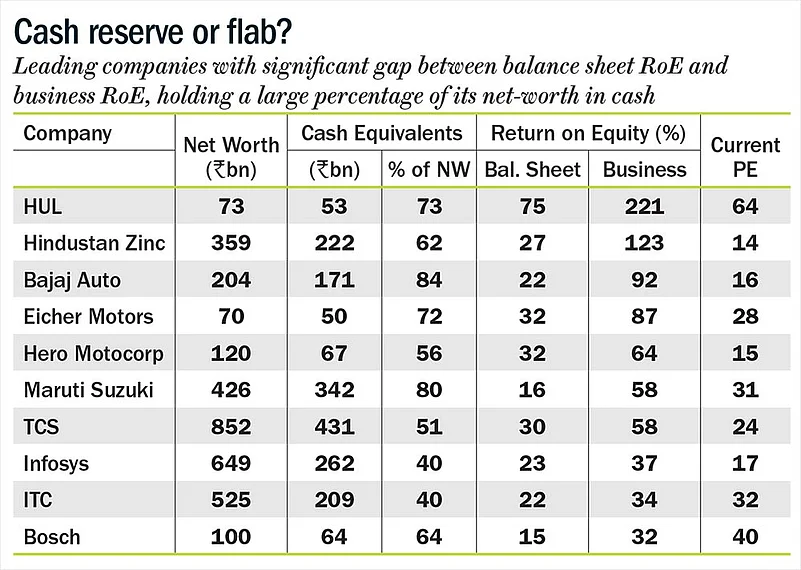

The report also talks about which RoE figure to consider when you value a company — the balance sheet RoE or the core business RoE. Over time, many Indian companies have resorted to holding cash on their balance sheets in excess of their immediate business requirements. This barely earns a 5% post-tax yield which drags down the overall RoE (see: Cash reserve or flab?). While in some cases the market is able to compute the core RoE and value companies accordingly, in others, the report says that the market fears capital misallocation and this becomes an overhang on the company’s valuation. In such cases, the gap between balance sheet RoE and business RoE can be brought down through a combination of higher dividend payout and share buyback.

Having classified all companies based on their 10-year average RoE into high RoE (greater than 15%), low RoE (lesser than 15%) and similarly with their 10-year earnings growth, the report proves that the high-RoE-high-growth strategy has handsomely outperformed the benchmark in all eleven 10-year periods (see: Winning strategy).

The Sensex is currently at a P/E of 21x TTM, which is about 24% higher than its long-period average of 17x. And with the markets in the overvalued zone, if a company is currently in the hyper-growth mode, the market is likely to end up extrapolating this too far into the future, pushing up valuations. “Hyper-growth rarely lasts beyond five to six years and this will prevent smart investors from buying into such stocks based on unrealistic growth expectations. Further, investors already holding stocks of companies in the hyper-growth mode must seriously consider exiting if valuations hit exuberant levels,” warns the report.