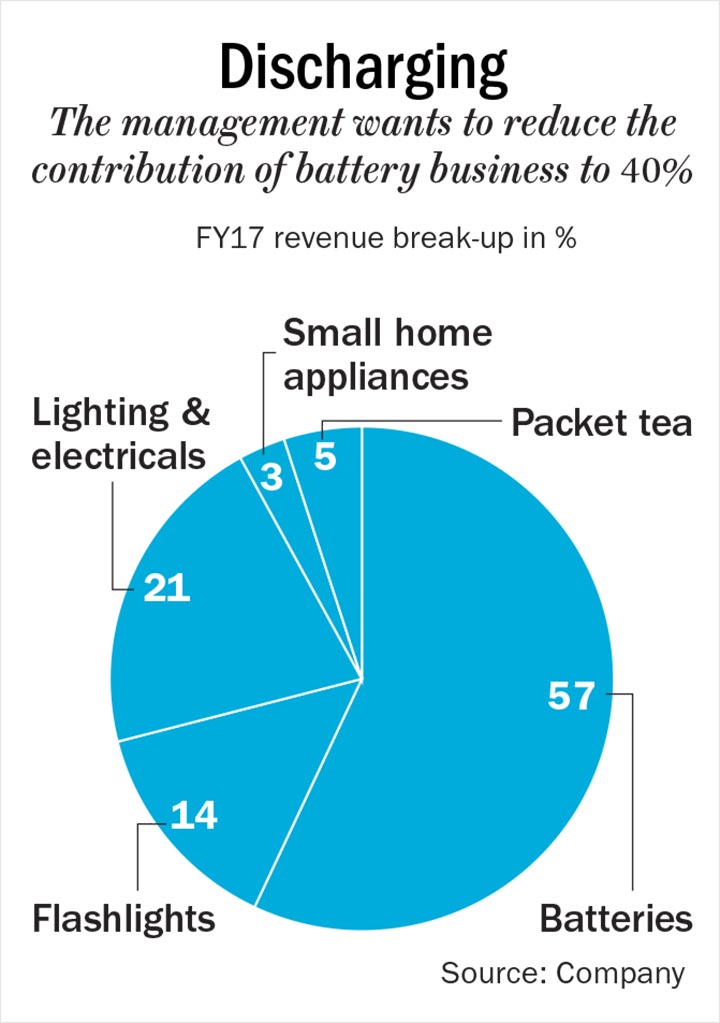

A third-generation entrepreneur, 33-year-old Amritanshu Khaitan is young and articulate. He took charge of the family’s Rs.1,400 crore Eveready Group only two years ago and is now looking to leverage the 110-year-old brand across a whole host of new businesses. The brand known for its iconic ‘Give Me Red’ campaign, commands a 52% share of the dry cell battery market in India. About 57% of its revenue comes from the sale of batteries and flashlights bring in another 14%. “Eveready is an iconic brand selling nearly 2.5 billion pieces and it reaches over 700 million people. However, the category turnover is only about Rs.1,800 crore. Hence, we have decided to leverage the brand to foray into new businesses,” says Khaitan. In 2013, Eveready diversified into the LED lighting market and the home and kitchen electrical appliances in 2016.

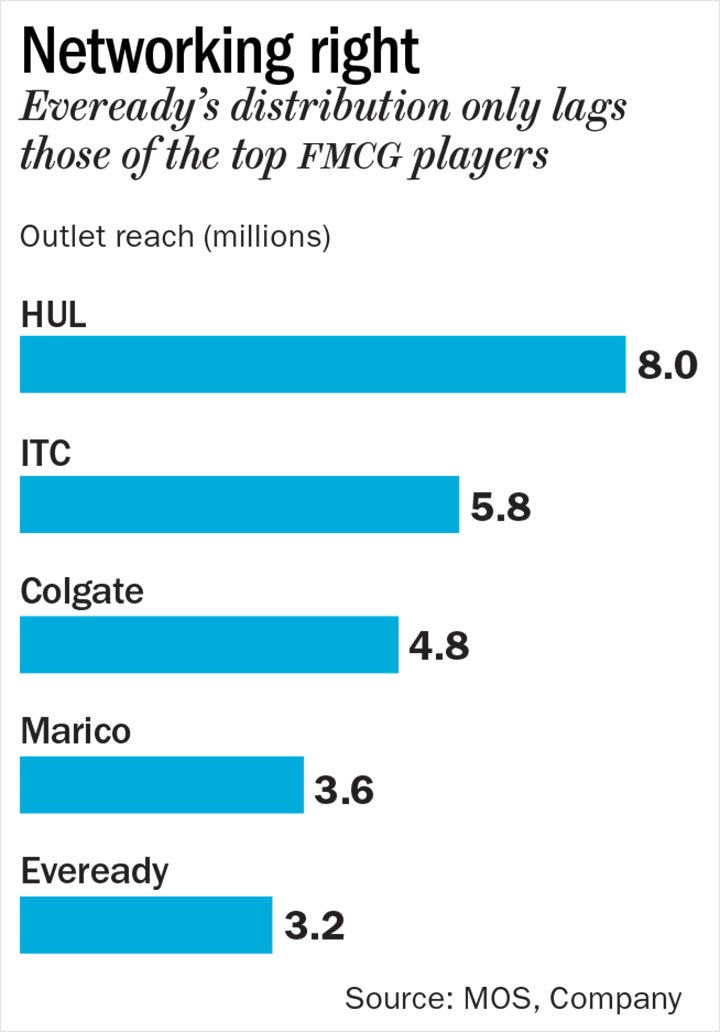

And earlier this year in January, Eveready announced that it was going to enter the confectionery space with the launch of a jelly-based candy called ‘Jollies’. It also formed a joint venture with Indonesia’s Universal Wellbeing for bringing its range of FMCG products to the Indian market. Universal Wellbeing, part of the Wings Group, is Indonesia’s largest FMCG player; offering a whole host of household care, personal care and skin care products. Eveready already distributes its products through 4,000 distributors to 3.2 million outlets across the country (see: Networking right). It is this reach that Khaitan wants to leverage, to scale up the confectionery and FMCG business. But both being highly competitive segments, Khaitan definitely has a challenge on his hands, as he tries to get a toehold in these mass markets.

Lighting up lives

While lighting and household appliances seem like a natural extension for the battery maker, many feel that the company could be out of its depth in the confectionery and FMCG businesses. Khaitan explains his logic in foraying into these segments, “Just because the brand ‘Eveready’ is strongly associated with batteries, it is difficult for people to associate it with any product other than electricals. But the fact of the matter is that batteries are sold through the kirana network all across the country. So in that case, dry cell batteries also fall under the ambit of FMCG.”

3 February 2026

Get the latest issue of Outlook Business

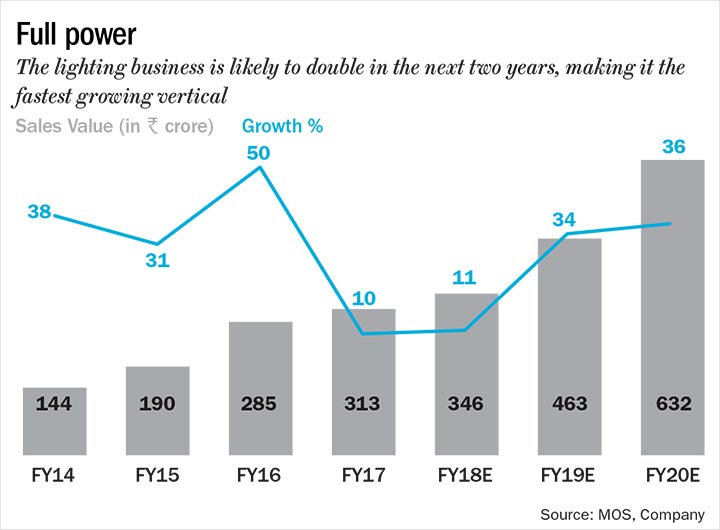

The distribution channel is a legacy, so why take the plunge only now? “The company was going through a rough patch in the late 2000s. Once the battery business started generating sufficient cash flow, the balance sheet of the company became stronger and allowed us to look at diversification opportunities and that’s how the LED business came into being in 2013,” says Khaitan. The LED foray has paid off and now rakes in Rs.300 crore for Eveready. Analysts expect that contribution to double by FY20 (see: Full power).

It also launched electrical and kitchen appliances such as, fans, ovens, irons etc. last year and expects the business to bring in about Rs.100 crore in FY19. Eveready is currently sourcing appliances from vendors in China and India, and markets them under its brand name.

Apart from this, Eveready also has a packet tea business that brings in 5% of overall revenue. In 2004, Eveready demerged its bulk tea business into a separate company called McLeod Russel leaving it with the battery, flashlight and retail tea business. The retail tea business in India is pegged at Rs.10,000 crore and in a bid to grab a large share of this market, Eveready joined hands with group company McLeod Russel to form a 50-50 joint venture. McLeod Russel is the largest producer and exporter of tea in the country and this marks its first foray into the domestic market. Eveready hopes to leverage on McLeod Russel’s expertise in procurement and manufacturing to scale up the packet tea business.

Candyland

For its entry into the confectionery market, the company decided to go with fruit chews or jelly candies. The overall Indian candy market is estimated at Rs.9,000 crore, where the fruit chews segment is Rs.400 crore and growing at 15% per year. Confectionery is already a very difficult market to enter, with both national and international competitors, such as Parle (16%), ITC (10.23%), Perfetti Van Melle (10.20%) and DS Group (4.84%) in a fierce fight with each other to increase market share through their brands Mango Bite, Poppins, Candyman, Alpenliebe and Pulse among others. Hard-boiled candies make up for more than half the market with toffees and chewing gum coming in next, accounting for nearly 20% of the overall segment. So why did Eveready choose to ignore the two largest segments in the confectionery market and choose to foray into a segment that barely accounts for 5% of the market? “We wanted to diversify in a space that is less competitive and offers scope for differentiation. Our fruit chews are healthier, as it has extracts of orange and strawberry in it,” informs Khaitan. Having outsourced manufacturing, Khaitan is launching Jollies in April-May 2018, at Rs.1 per candy, initially in Kolkata and Jharkhand with plans to go pan-India by July-August 2018.

Even in the so-called less competitive segment, Eveready will have to battle with established brands such as Perfetti’s Fruit-tella, Mentos, Mapro’s Falero, Parle’s Mazelo and ITC’s Jellicious with similar offerings. Over the next five years, the fruit chews segment is estimated to grow to Rs.1,000 crore but even then, it will only constitute about 7% of the confectionery market. Khaitan is aware of that and says once they iron out the initial chinks in the business, Eveready will foray into the much larger, hard-boiled candy segment as well.

As a new entrant in the confectionery space, Khaitan draws inspiration from one of the biggest success stories — Pulse. A candy launched in 2015, by Noida-based DS Group, the brand has managed to rake in Rs.300 crore, since then. “From product development to marketing and distribution, Pulse managed to get it all right. Although, every new player might not be as successful, we are confident we will grab a good share of the fruit chew segment first, and then hard boiled candies with our differentiated offering,” says Khaitan. Like Eveready, the DS Group enjoys a wide reach through pan and small retail shops across the country through its products like Rajnigandha pan masala and Pass Pass. It also retails the ‘Catch’ brand of spice sprinklers and premium mineral water through kirana shops. “For a Rs.1 product, the cost of distribution is quite high. It works out to nearly 15 to 16 paise per piece, which we have already incurred. So it gives us a competitive advantage,” says Khaitan.

Prateek Srivastava of Chapter Five Brand Solutions feels getting the distribution right is only one part of the equation and that alone will not guarantee success. According to him, finding success in the food business can be quite a challenge. He cites ITC as an example, “ITC had to make significant investments in the food business. But, it took several years before they achieved scale and became profitable,” says Srivastava.

Shashank Surana, VP, DS Group who has been instrumental in scaling up the candy business shares his experience. “One of the critical success factors was distribution, which was already established. Since, we have been working with pan masalas for decades now, we wanted to focus on flavours and fragrances — to create a differentiated taste. So, we devoted three years to product development,” he says.

Every time a new player failed in the market, the team learnt a lot and focused on researching the product and taste profile of customers. “It was very clear that among flavours, kaccha aam ruled the roost followed by mango in a sweet form. So we knew we had to go with mango, but we had to differentiate as well. If you think about it, kaccha aam is always eaten with rock salt. So we figured out a way to centrifuge the candy with rock salt and other spices,” explains Surana. It took about three to four years for the company to get the product right, since they kept going back to customers for the right taste and flavour.

Surana feels while there are no entry barriers in the candy market; it will be a difficult game, especially for new players. “There is a lot of impulsive buying and no loyalty to any single product. So you not only need to have a good distribution network, but also have a differentiated offering in terms of flavour and taste,” he says.

But industry consultants feel, even on the distribution front, Eveready will need to widen its reach. “For candies, you have to reach the smallest retail points — from panwalas to pharmacies. Typically, batteries are not sold at these places,” points out Arvind Singhal, chairman, Technopak Advisors. “Diversification could work for Eveready if they also get the taste, flavour, packaging, and marketing right. But they will need to acquire some of those skills,” Singhal adds.

And that’s what Eveready plans to do! “Whenever we diversify, we hire people from that domain. When we moved to LED and electronics, we hired leaders from that industry. Similarly we will put together a team for the confectionery business as well,” Khaitan says. Wanting to keep the business asset-light, Eveready has already outsourced the product development to Mala’s, which is a well-known company in fruit concentrates. Mala’s has been making jams, squashes, syrups and crushes for over 50 years.

Wings to fly

Completing Eveready’s foray into FMCG is its joint venture with the Wings Group. It will hold a 30% stake in the venture while Universal Wellbeing will hold the balance 70%. The 70-year-old Group started off as a detergent company and today sells a range of products including, personal care, fabric care and food products. The joint venture will decide on what products to introduce in India and whether to manufacture, import, or outsource them in the next couple of months. Srivastava believes, “Wings has found a good distribution partner in Eveready. Since they have been in the FMCG business for longer, it is likely they will take the lead in the venture for now, since they understand the consumer needs in this space better.”

Khaitan wants to bring down the contribution of the battery and flashlight business to about 40% of turnover in the next two-three years (see: Discharging). Apart from its limited market size, the battery business continues to battle its Chinese counterparts on price. So he is betting on the lighting and appliances business to scale up and bring in one-third of the revenue and the FMCG business — which he hopes will contribute Rs.400-500 crore — to make up the balance. Riding on the growth from its new businesses, analysts expect the company’s revenue to increase from Rs.1,354 crore in FY17 to Rs.1,946 crore in FY20 and net profit to increase from Rs.94 crore to Rs.151 crore during the same period.

However, Eveready will have to build brands afresh in businesses they have little experience in and that is not going to be easy. Plus they are battling worthy competitors in each of these segments. But these are risks that Khaitan is willing to take. For him, this is the only way he can take Eveready to the next level.