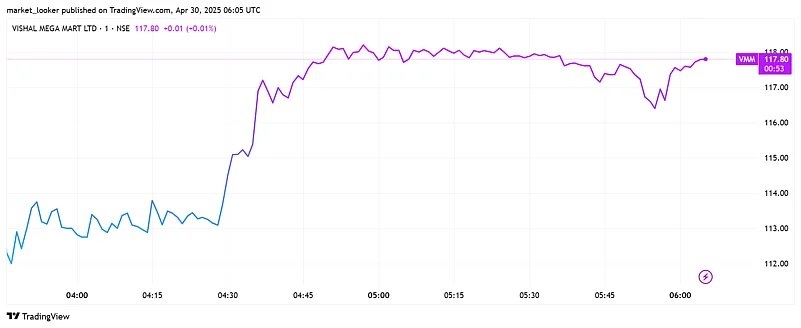

Vishal Mega Mart shares surged by nearly 10% on the bourses after the company announced robust Q4 results. The hypermarket chain recorded a net profit of Rs 115 crore for the quarter ending March, marking a surge of 88% from Rs 61.2 crore recorded in the corresponding quarter of the previous year.

At 11:10 am, the shares of Vishal Mega Mart were trading at Rs 117.68 price level, up by around 9.26% on the National Stock Exchange.

1 August 2026

Get the latest issue of Outlook Business

Revenue from operations soared to Rs 2,547.9 crore during the quarter under review, an uptick from Rs 2,068 crore recorded in Q4FY24. The company also witnessed a surge in overall margins. While EBITDA increased to Rs 357 crore from Rs 250.5 crore, experiencing a 42.6% surge, EBITDA margins improved to 14% in Q4FY25 as against 12.1% reported in the same previous fiscal period.

For the full financial year 2024-2025, the company's net profit levels increased by 36.8% to Rs 631.97 crore. As for revenue from operations for the full fiscal year, the figure surged to Rs 10,716 crore, experiencing an uptick of 20.2%.

_(1)_570_850_1642198580.jpg?auto=format%2Ccompress&fit=max&format=webp&w=768&dpr=1.0)

Vishal Mega Mart Shares

In the last 6 months, the shares of the hypermarket chain surged over 5%. On a year-to-date basis, the shares have surged by around 11% on the bourses. However, the stock is still down by over 7% from its 52-week-high of Rs 126.87.

Advertisement

Expansion in the quick commerce segment remained robust, with 656 stores operational across 429 cities. The registered user base saw a strong 65% year-on-year growth, reaching 8.7 million. As per a report by ICICI Securities, the loyalty program continues to perform well, contributing to around 95% of total sales from registered users. Regionally, revenue remains well-distributed across north (43%), east (29%), south (19%) and west (8%).

"We maintain our earnings estimates for FY26E/FY27E, modelling revenue/ EBITDA/PAT CAGR of 18%/19%/26% over FY25-27E," the brokerage firm said in its report and maintained a 'Buy' call on the stock with a prospective upside of 30% from the current market price (CMP) of Rs 108.