Seven years after the century's worst recession, thw world is facing new challenges in the form of a sell-off in commodities, a slowing global economy and an unconventional monetary policy. What are the big risks in 2015 and how will they shape the economy?

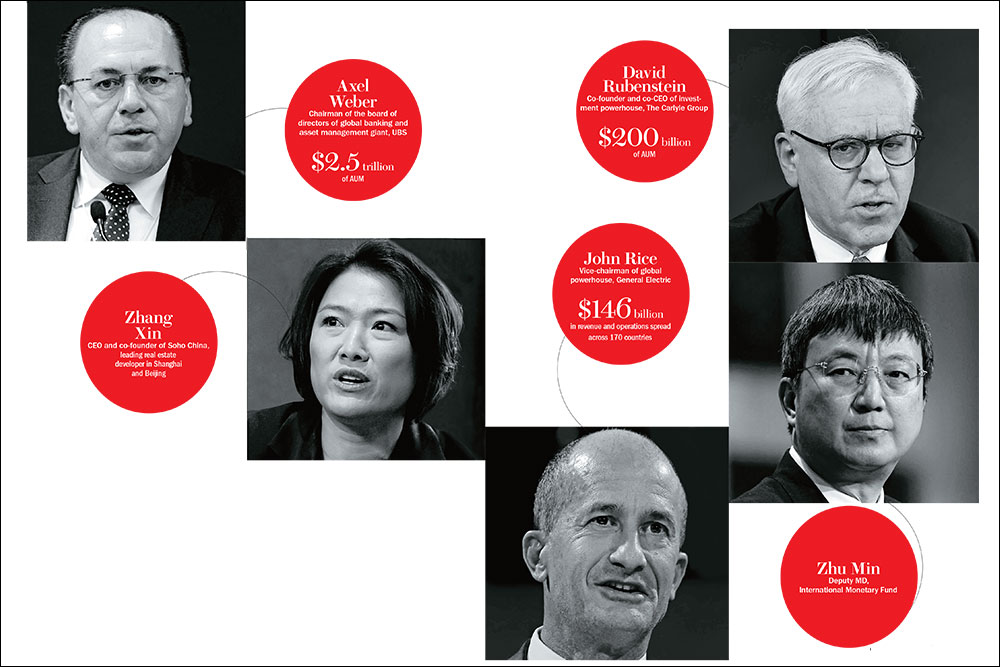

Moderator: Axel Weber, let me kick this off with you. You approach this environment both as a business person and a policymaker, having been the president of the Bundesbank. Can you assess what the Swiss National Bank did last week? What are your expectations from the ECB?

Axel Weber: First, it was always clear to me that the Swiss floor to the Euro was temporary, and temporary has got to end. We have seen a depreciation of the Euro pretty strongly across the board and the Swiss National Bank did the right thing to stop pegging to the Euro or at least having a floor. International flexible exchange rates are the norm and they moved back to normality. There are challenges but they are manageable. There will be a big impact on the Swiss economy. Once the dust settles, we are moving back to a more normal exchange-rate regime for Switzerland.

As for Europe, the issue is that the ECB has continuously bought time for European policymakers to fix the issue. Europe is not back, but the tension has somewhat gone and it should use the fact that they are flying under the radar screen to do the real reforms. But they didn’t. The ECB can only be part of the fix. In my view, they shouldn’t go too far because the more they do, the bigger the incentive for governments to do less, and if you continue to buy time and it is not used for reforms, you have to ask yourself whether more of the same is the best recipe or whether you should change the medication. Europe faces many challenges, of which falling prices is just one. The others are high unemployment, no strong-growth environment and a lack of reforms, and policymakers shouldn’t really kid themselves.

3 February 2026

Get the latest issue of Outlook Business

Moderator: Zhu Min, one of the catalysts for lowering the expectations for global growth this week is the persistent weakness coming out of Europe.

Zhu Min. Yes. Last year, Europe’s economic growth was only 0.8%. So we forecast only 1.1%, very much relative. Why so low? The investment is weak. Compare today with 2007. Europe’s investment and job creation was 5% of the GDP, which reflects the fragility of the region, weak confidence and policy environment. Consumption is strong but not strong enough to overcome weak investments. In Europe, we need a three-pronged policy — an accommodating monetary policy, push to investments, and reforms — to push growth. We need reforms in the labour markets and countries can’t operate in silos.

Moderator: If it is so obvious in terms of what we need, why is it not happening?

Zhu Min: Because we don’t have everyday demand-side policies. That’s because we don’t have a fiscal space — the tax is very high. In advanced economies, the tax would be above 100% by 2020. We don’t have much of a monetary policy because central banks’ balance sheets are big enough and interest rates are zero already. So what do you do? You need a supply-side policy. You need structural reforms and smart investments. You need investment in infrastructure, in innovative enterprises and in the knowledge economies. When you do the structural reforms, you need political leadership. We don’t see that yet.

Moderator: Zhang Xin, can you characterise the growth in China right now?

Zhang Xin: China is on the other side of the spectrum right now. So much of the growth was driven by investment for the last two decades that now we are seeing the other problem — the return on investment has become lower because of excess investment and not enough consumption. So China needs reforms — tax reforms that support the growth of consumption.

Moderator: Where are we with respect to real estate in China?

Zhang Xin: Real estate in China has moved from red hot to deep cold. Right now, it is the coldest sector of the economy and we can comfortably say that China’s urbanisation-led growth is almost coming to an end. There is very little money going into buying new land and buildings because so many buildings have been built. A developer like me, who used to spend so much time buying land and developing buildings, is now also moving to the consumption side, trying to get more people to come in to use my office buildings.

Moderator: David Rubenstein, is it true that the US is seeing the most vibrancy, relatively speaking? How do you invest around the world right now?

David Rubenstein: Right now, the US seems to be the greatest place to invest because we have growth at over 3%. The IMF is predicting 3.4%, and our own numbers are predicting something similar for this year. Inflation is very low. If the Fed increases interest rates, it is going to be very modest. A 3.5% growth is still very good when you have a $19 trillion economy. The biggest problem in the US is that as interest rates go up a bit, more money will come in, the dollar will get stronger and that could hurt exports. In terms of investing, there is nothing better now than the US because of the rule of law, transparency and good economic factors. But emerging markets are still a large part of the global economy. Eighty-five percent of the world’s population is in emerging economies and 55% of the GDP is in emerging markets, although this has slowed down. This is probably a buying — not selling — opportunity. So I am still very bullish on many emerging markets, particularly China, Sub-Saharan Africa and India.

Moderator: Particularly as valuations in the US have been rising…

David Rubenstein: They have been. It is a trade-off. In the emerging markets, you can probably get things at lower prices for a somewhat greater risk. In the US, prices are not cheap. Ebitda multiples for buyouts are roughly the same as they were in 2007. One of the things that is of concern, and should be to everybody, is that typically in the West and the US, we have a recession every seven years. We are about seven years from the last recession. We are not able to predict but something is going to happen in the US and the global economy that we are not projecting, something similar to the oil price, which means a gigantic price cut in the US and in Europe. In the US, we are a family of four with an average income of $55,000 which is a median income, and it is a tax cut of about $900-$1,000 per family. That is going to spur consumer spending in the US and Europe.

Zhu Min: David is right, falling oil price is terrific news for the consumers and consumer-driven economies. But it is not good news for producers, and investments will slow down. Also, about $1 trillion of the energy industry abounds in the market. So how do you reprocess bonds and how do the spreads change? This may impact the financial sector. Particularly for oil-exporting countries, the physical production costs are still very low, as low as under $20 per barrel for some. But the budgetary cost is very high — it is around $100 per barrel for many. So obviously, those countries will suffer lower current account surplus and deficit, low growth, exchange rate appreciation and sharp market drops which may have a spillover impact for other countries as well. So while on a net basis, falling oil prices are a positive, we should not overestimate the positive impact of oil price.

David Rubenstein: I didn’t mean to say that falling oil prices are an overwhelming positive. There will be layoffs in oil companies and oil-producing countries which have budgets that are $89 a barrel and now they are not going to get that. So they will go into deficit spending. But here is a good example of something that you wouldn’t have anticipated. Russian companies have borrowed roughly $650 million from the West. Because their economy is weak, if the Russian companies can’t service that debt, it is going to be a problem. Who owns most of that debt? Mostly European banks, which have been struggling, and can struggle again if the Russians can’t pay off their debt. I would say the single greatest new opportunity to invest in is distressed debt in energy. For companies that expanded a lot, assuming that oil would be at $100 a barrel, their debt isn’t going to be worth a hundred cents a dollar. A lot of people are going to buy that debt at discount, and take control of some of these companies.

Moderator: What do you make of it, Axel?

Axel Weber: I think oil is normalising. Going forward, global liquidity is coming down. So if you look back over the last seven years, there was a lot of money that went into the oil market and was driving commodities as part of an asset class. Now, commodities are back to being commodities. The other thing is, the biggest marginal supplier of energy is now the US. It is changing its energy balance and that has an impact. Opec as a cartel will produce less than one third of the world’s supply of oil in the next couple of years. That means there is very little ability to reduce capacity utilisation quickly, and therefore you see the strong correction in the oil market. Oil will trade back to something between $50 and $70 because that is where the largest part of global marginal supply is, but it will not go up to where it was. I think that should be welcomed as the normalisation of what used to be a pure commodity and which, over a couple of years after the crisis, became driven by other things.

Moderator: I want to get back to something David said, and that is the European Banks and their vulnerability. We are trying to identify what could be the catalyst in terms of sending us back into recession. How vulnerable is Europe right now?

David Rubenstein: American banks went through lots of heartache and angst, and today they are in reasonably strong shape. The European banks honestly didn’t do all that the American banks did. Maybe the government regulators didn’t force them. Today, they are not in as strong shape. So if there were defaults from Russia it would hurt the European banks. I suspect there will be a lot more currency turbulence in Europe and that is going to hurt some of the banks as well. I think the banks are much more vulnerable to turbulence in

the US and the global economy than the American banks are.

Moderator: Zhang Xin, your views?

Zhang Xin: In China, we have recently been encouraged by the government to go outside of the country to invest. I had an opportunity to look at an asset in Europe. We bid but backed off in the end. We saw that because of the monetary policy in Europe making borrowing so cheap, if you buy a building through long-term borrowing, it will probably cost you 3%. But there is no future of the building since that would be led by the growth in the economy. So while you have this cheap borrowing rate that makes everybody rush in to borrow and buy, on the demand side you really don’t know. Due to a lack of investment, Europe is becoming another place that is deflationary like Japan.

Moderator: Axel, would you disagree?

Axel Weber: Look at it this way. In China, the real estate market boomed for a long time and is now correcting. There is inventory overhang. We have seen a price correction last year. We are probably going to see another 10% decline in housing starts this year. But there was this big rotation — investors that were in real estate and property-related investments rotated these investments into the equity markets. There was also a big influx of overseas money into China, so there was a major rally that will continue under these conditions.

The same is happening in Europe. It happens always when QE starts. Look at the Fed. You have a very low interest rate, and a balance sheet that is expanding. You don’t get a return on fixed income assets, in particular in sovereign debt, so you move to equities. In the US, the equity boom happened with a relatively stable path. In Japan, the equity boom happened with a depreciation of the yen and what you have seen in Europe is currency depreciation. We are now overweight on European equities because there will be a pick up in the equity markets. It is not like European equity is dependent on European demand. Many of the European corporates are global companies. Their main export markets now are the US and China. Not every European company is the same. But I think we see things improving.

Moderator: But from your standpoint Xin, you are a long-term real-estate investor. You are not ready to even look at valuations that have come down so much in Europe.

Zhang Xin: In fixed assets in real estate, the price has not only not come down but has actually gone up because of the monetary policy, because it is so cheap to borrow. So for these buildings, you cannot always use equity, you have to borrow. If half of your money is borrowed at a very low interest rate, you will borrow. So that makes the buying price of these buildings very expensive. You are willing to buy expensively if you know that there is growth and the rent will go up. But if you are not confident about the economy’s growth, you will not do it.

David Rubenstein: Now deflation is a much more serious problem in Europe, but economists and central bankers are much better at solving inflation. It will take a long time to get out of deflationary cycles. Governments traditionally built infrastructure, but now they will be dependent on the private sector through private-public partnerships. If you are happy with rates of return in infrastructure projects, you can be pretty happy with what you are going to get out of good infrastructure projects. I think a mid to upper teen rate of return on infrastructure projects in equity is a reasonable rate of return and you are going to see more projects this way in the US and Europe. I think, if there is more private equity, the world would be in a much better place.

Moderator: What country have you been investing in the most over the last few years?

Zhang Xin: The US.

Moderator: David, where are you investing right now?

David Rubenstein: We are investing in Japan, which we find very attractive. It has demographic issues but we can talk about those later. We think the US is attractive. We still have very bullish views on China. People are obsessed with the Chinese growth rate. Since it grew 10% a year for 30 years, they think it should grow at 10% every year. This is not a realistic assumption. It is a $10 trillion a year economy, growing at 6.5% a year which is still spectacular at that size. The US cannot grow at 6.5% a year, we are happy at 3.5%. So I think China doesn’t get the credit it deserves although it does have some issues in disequilibrium. But generally, we do think that PE or private investments are probably going to outperform public investments over the next couple of years.

Zhu Min: I think the Chinese government is doing a lot of reforms. China is a transitioning emerging market. Their last year’s growth number is impressive. It’s getting slower but doing better. For the first time, the consumption contribution is more than that of investment to growth. For the first time, you see the service sector is bigger than the industry. When you change the structure, the growth will go down. Also, to add to what David said, the whole knowledge economy has taken off now — you see so many new industries in Germany and the US. We have technology-driven innovative start-ups. Their productivity is very high and the returns are very good. The financial sector should take more risks moving into new areas.

Axel Weber: You have got to invest in growth. At 3.5% growth today, we are overweight on US equities. We just moved to an overweight of equities in Europe because we think that the same thing will play out in many other countries. We are overweight on emerging markets and China. If you want to capture the growth dividend in no-growth areas such as in some European economies, you can get it only through equity exposure because fixed income is very low everywhere and you have to get it from the growth regions. The US is less than twice the size of GDP of China but with China growing at roughly 7%, it is still contributing the most to global growth. So China exposure is still very important to have for non-Chinese investors.

Moderator: John Rice, where are your investments right now?

John Rice: We are looking at a few developing markets. If you look at market size, the growth of the middle class, the demand for infrastructure, there is no country that is off limits, except some where you can’t participate legally. So we invest in Southeast Asia, Latin America and Africa.

Moderator: Esteemed members of the panel, we thank your for your thoughts. Thank you everybody.

This WEF session was developed in partnership with Fox Business