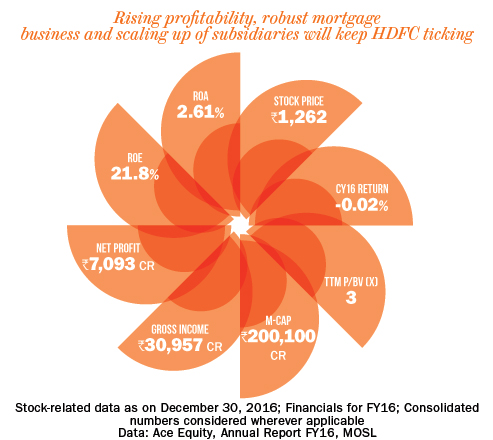

HDFC has been an overwhelming favourite with investors over the past two decades. And why not, the stock has created enormous wealth for them with a compound annual growth rate of 22% as against 11% for the Sensex during that period. So, what makes it as one of the top stocks to own in the New Year and beyond?

HDFC has been an overwhelming favourite with investors over the past two decades. And why not, the stock has created enormous wealth for them with a compound annual growth rate of 22% as against 11% for the Sensex during that period. So, what makes it as one of the top stocks to own in the New Year and beyond?

Our positive view on HDFC is driven by the growth outlook for its core business of mortgages and the continued value creation by its various associates and subsidiaries. Founded in 1977, HDFC is a pioneer and the market leader in mortgages and developer finance. It has been the largest housing finance company for the past three decades and has grown its total assets under management (AUM) by 20x from Rs.132 billion in 2001 to Rs.2.6 trillion in 2016. HDFC has a wide distribution network across the country and is also aided by its associates, primarily HDFC Bank with its over 4,500 branches across the country.

It’s a no-brainer. Demand for housing in India will continue to remain strong in the coming decade. While mortgage penetration has improved from 2% of GDP in FY02 to 9% of GDP in FY15; it is still very low levels versus other developed and emerging markets 60%-100% for developed economies and over 15% for emerging economies like China, Malaysia, etc.

India has various drivers to raise the penetration level of mortgages over the next decade — favourable demographics (a young population; median age of 26 years), large unmet housing demand, low levels of urbanisation, and improving affordability. The government’s particular focus on housing-for-all should provide growth opportunities — its thrust on affordable housing, enhanced tax incentives on home loans and lower risk weights for affordable housing loans bode well for the housing finance industry.

HDFC’s mortgage book comprises of individual loans (74%) and non-individual loans (26%, spread across lease rentals, construction finance and corporate loans). The individual loan portfolio, with average ticket size of Rs.2.5 million, has been growing at a CAGR of 20% over the past five years. This momentum will continue led by several macro positives, as discussed earlier. Over 80% of borrowers are salaried, with an average age of 37 years. Asset quality has remained largely stable over the past several years and is expected to remain so. The non-individual book, where growth was moderate for the past three years, will see some uptick in the coming years, as economic activity picks-up in FY18. Moreover, as the real estate market gets rationalised (led by the recent measures of the government), risk pricing of this segment will be favourable for players such as HDFC.

The lending institution has a diversified liability franchise with borrowings from banks, public deposits, NCDs and external commercial borrowings. Non-bank borrowings account for 80% of total borrowings, resulting in lower weighted average cost of funds. The company was also the first Indian company to raise money from Masala Bonds, raising Rs.30 billion in June, 2016. We believe its strong liability franchise enables it to price its loans competitively, while maintaining spreads as the same time.

Given its large size of operations, HDFC is able to leverage significantly on costs. It is one of the most cost efficient franchises in the industry with cost to income ratio of 10% as of FY16 — the lowest in the industry. While there have been concerns of correction in real estate prices, this has been limited to a few markets.

Creating value

Over the past two decades, HDFC has incubated several subsidiaries and associates across businesses and most of them were early entrants in their respective industries.

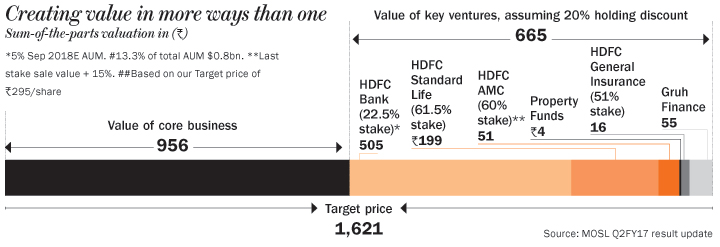

Of these, HDFC Bank and Gruh Finance are listed subsidiaries. HDFC Bank has grown to become the largest private sector bank in the country in terms of loan book size (Rs.4.9 trillion) and profits (Rs.123 billion in FY16). The bank’s market capitalisation (Rs.3.1 trillion) has now exceeded that of HDFC (Rs.2.0 trillion). We expect the bank to continue to grow profitably and gain market share for the next 10 years.

HDFC Standard Life recently acquired Max Life and the merger is expected to be completed in FY18. The combined entity will be the largest private sector life insurer in India, with a private sector market share of over 20%. Moreover, the combined entity will have strong product offerings across all segments (Max Life is strong in ‘par’ business, while HDFC Life is strong in ULIPs).

HDFC AMC has been one of the top AMC with an AUM exceeding Rs.2 trillion. It is also among the most profitable AMCs in the industry. These three associates/subsidiaries contribute over 40% of the total SOTP of the company. We see the value creation from them to grow at a faster pace, which is best captured by being an investor in HDFC.

Quality demands premium valuations

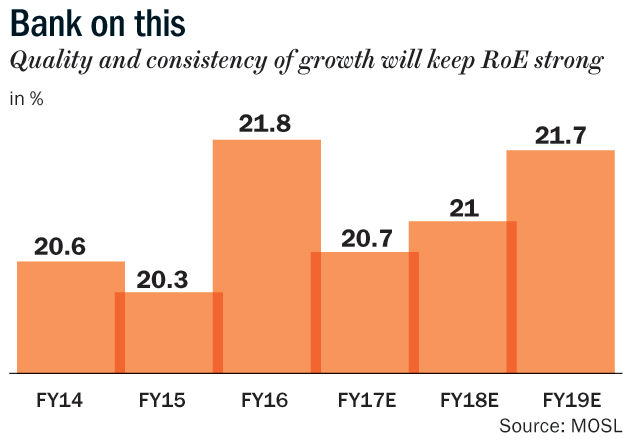

Led by strong growth in its core business, HDFC’s return ratios have remained consistent for the past two decades. We expect RoEs to remain well above 20%; quality and consistency of growth will remain strong. Valuations for this strong franchisee remain attractive and are at long period averages. As interest rates in India are headed south, this will have a further positive impact on earnings and valuations on across businesses for HDFC group.

In corporate India, very few groups have created such enormous wealth for investors across their group companies for a long period of time. We see this process to not only continue, but also accelerate as more group subsidiaries and associates gain size. HDFC and its listed group companies have foreign ownerships of well above 70%, marking it as one of the best owned stocks by FIIs. We would suggest that domestic investors should also consider raising their investment to benefit from the long-term value creating machine.

The writer, in his personal capacity, does not own the stock but the brokerage has a buy call on the stock