I believe the key difference between a great company and an average company is its management and leadership. We have many examples of great managements creating huge value for stakeholders and an equal number of examples of mediocre managements losing the plot.

I believe the key difference between a great company and an average company is its management and leadership. We have many examples of great managements creating huge value for stakeholders and an equal number of examples of mediocre managements losing the plot.

RBL Bank is one such success story where a high quality management team has created immense shareholder value over the past five years and is also beautifully positioned to continue building this value for years to come. I would attribute many reasons for the bank’s success, but experienced and high quality management is the single-biggest factor behind its success story.

Since its inception in the 1940s, the bank had managed to grow its balance sheet size to only Rs.2,000 crore by 2010. But since it was taken over by a new management team, led by Vishwavir Ahuja, the Kolhapur-headquartered bank’s balance sheet has grown 20x to over Rs.41,000 crore (FY16) in just six years!

The bank has built a strong operating platform, enhanced its product offerings, increased its customer base multifold, launched a multi-channel distribution network and implemented a robust technology infrastructure. The foundation has already been laid and now a gradual execution of a well-thought through strategy will lead to the emergence of another great banking enterprise.

Credit growth in India has historically been 1.3x of the nominal GDP growth rate. Given that we are still an emerging economy and significant investment is required across almost every sector, I strongly believe that India will be able to maintain this credit to GDP ratio. India’s credit to GDP ratio is still 60% compared with developed markets credit to GDP ratio of 150%. While industry credit growth has been sluggish over the past two years, it will revive in the medium to long term. Credit growth rate has been superior for private sector banks which have been continually losing market share in favour of private sector banks and non-banking finance companies. This trend will continue as public sector banks fail to drastically change the way they operate. RBL Bank is very well positioned to take advantage of this growth given its low loan base. Simply put, as India’s nominal GDP grows at 10-12%, overall bank credit will grow at 14-18%. While private sector banks will grow at 20-25%, RBL will grow at a much-impressive 30-35%.

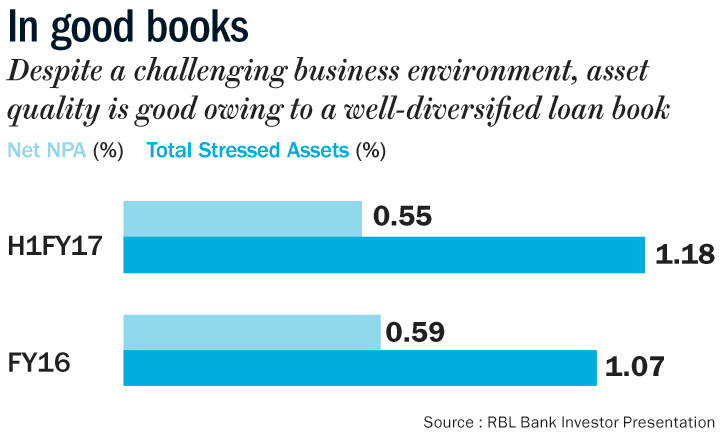

The bank has demonstrated impressive loan book performance with a three-year track record of 49% CAGR. The advances book is granularly built with a higher focus on small and medium enterprises, mid corporate and financial inclusion clients. Asset quality is good as the loan book is very well spread out and has been largely built after the beginning of stress in sectors such as infrastructure and steel. Industry exposure is also very well-diversified, focused more towards services sectors such as retail, construction, healthcare and financial services. Similarly, on the deposit side, the bank has been the beneficiary of declining cost of funds. It has systematically increased its low-cost deposit ratio which will only improve as the bank further strengthens its distribution network through branch expansion and utilisation of its technology platform. Deposits have shown a CAGR of 43% over the past three years.

The bank has made significant investments over past six years in building a strong infrastructure, the benefit of which is yet to be fully reflected in profitability. The branch network has increased from 108 branches in 2012 to 201 branches as of 2016. The management team has been significantly beefed up with top notch experienced banking professionals hired from multinational banks and top-tier Indian banks. As the balance sheet grows, the cost to income ratio will gradually decline, an aspect which has been visible over the past two years.

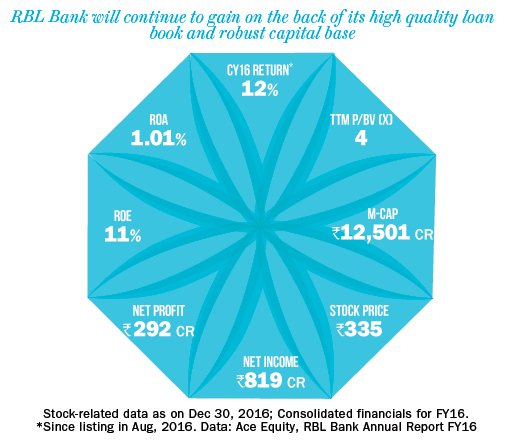

The bank has also built a strong platform to drive higher non-interest fee-based income. This helps private banks to generate significantly higher returns on assets, a key factor which leads to differentiated price-to-book value multiple. A sustained higher share of fee income and lower cost ratios driven by scale will gradually lead to expansion in return on assets which will help sustain the current price to book value multiple. The profitability and return ratios have only been improving over the past three years. Profits clocked a CAGR of 47% since 2013 and return on assets has been constant at 0.9% between FY13 and FY16.

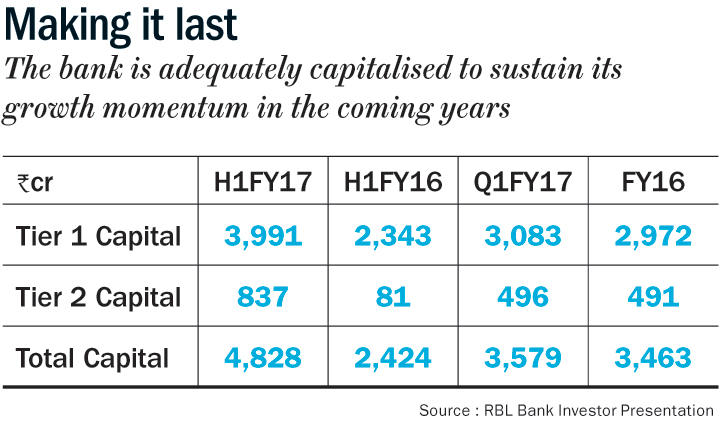

Another critical factor in the success of any bank or a fund-based non-banking financial corporation is its ability to raise capital, which is the raw material for running a business. While public sector banks continue to worry about their recapitalisation, private banks have created enough value for shareholders who have been happy to put more money behind them. RBL Bank is no exception and has demonstrated its ability to raise capital across multiple rounds from both private and public markets. The recent Rs.1,200 crore initial public offer saw a tremendous response with the issue getting oversubscribed 70x. The stock has also delivered 29% return over the past four months since listing. At its current level, the valuation is not cheap, but the bank’s growth story is definitely intact. I believe the stock should touch Rs.1,000 in three years, giving an IRR of close to 40%.

The success of private sector banks with quality management teams is not unheard of in Indian corporate history. Many investors, across multiple investment cycles, have made great returns in private banks. This started with the success of HDFC Bank in the 1990s and continued with the success of Kotak Bank, Yes Bank and IndusInd Bank in the 2000s. RBL is the latest entrant in this list which will derive disproportionate benefit because it is starting from a small base.

The author does not have a position in the stock