Action, emotion, drama and romance for ages have been the raison d’être of Indian cinema. But there is one more facet to India’s rich filmi tradition – and that’s trains. Bollywood, in particular, has the longest playing track with Indian Railways, be it songs or even movies such as The Train, The Burning Train and 27 Down. But the most engaging encounter with railways has been one that involves action, and how can one not talk about the cult movie Sholay. A drudgingly moving goods train ends up creating a strong bond between the upright inspector and a pair of crooks Jai and Veeru. Just like Sholay made the ubiquitous goods train more appealing to moviegoers, so has Jagdish Prasad Chowdhary for investors with Titagarh Wagons. A heavy engineering industry veteran, Chowdhary set up Titagarh two decades back in Kolkata and the company has since emerged as one of the leading private sector wagon manufacturers in the country.

While wagons remain its flagship business, Titagarh has also forayed into ship-building and allied businesses to make the most of the growth opportunity. With India embarking on an unprecedented infrastructure spending spree, an investor would naturally look out for a potential multi-bagger and Titagarh is clearly on track to becoming one.

With five facilities across the country, Titagarh today can produce 8,400 wagons, 36 rakes of electric multiple units and diesel electric multiple units, 500 coaches and 30,000 MT of castings. Its defence division builds bailey bridges, nuclear shelters and defence-related railway wagons. It also has a division that manufactures crawler cranes, excavators, besides a ship division which builds naval barges and bulk carriers. Not to mention its recent entrant into the tractors and farm equipment business.

M&A goods

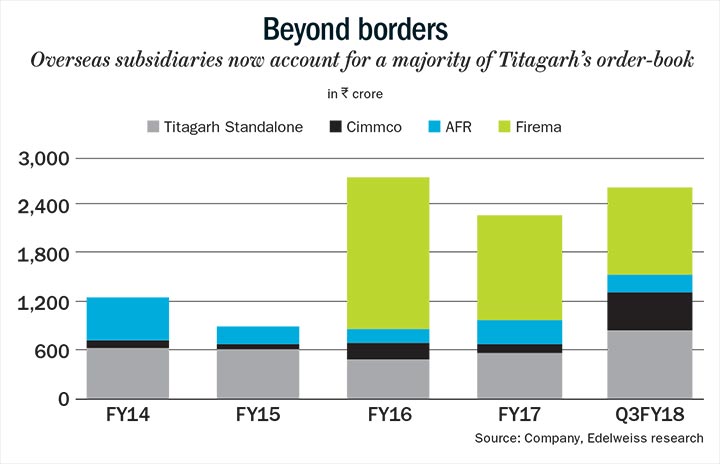

Titagarh has also grown through a string of strategic acquisitions which the company has managed to integrate well, both overseas and back home. In fact, it was a first in the industry when Titagarh acquired the France-based AFR group in 2010, the largest freight wagons manufacturer with a capacity of 5,000 wagons and Firema of Italy, known for metro rolling stock in 2010, followed by Firema Adler of Italy in 2015. The company also bought out Sambre of Italy and entered in to a joint venture with French firm Matèire to acquire know-how for Bailey bridges.

3 February 2026

Get the latest issue of Outlook Business

The AFR buyout improved Titagarh’s design capabilities, thus bolstering its position by building special purpose wagons for the private as well as the defence sectors. Tailor-made solutions were provided to container freight operators and producers of cement, coal, steel, oil, chemicals, fertilisers and food grains for their transportation needs. Today, the company can also design wagons that can carry different types of trucks, catering to the needs of the logistics industry. Firema, a designer and manufacturer of metro coaches and semi and high speed train, has added to Titagarh’s services portfolio by offering overhauling, repairing and maintenance of rolling stock.

These acquisitions have proved to be a boon with the Firema business turning around and contributing 57% to Titagarh’s FY17 revenue. The acquisitions and the company’s efforts to sharpen its skills will help it capture a higher market share when wagon orders gather pace.

Changing track

Given its dependence on railway wagon orders, Titagarh’s financial performance was volatile in the past. But in recent years, the company has de-risked its business by expanding into other verticals. With private wagon orders showing an uptick, the company’s dependence on the Indian Railways’ wagon business is down to about 15-20%. Of the company’s overall order-book of Rs.2,800 crore, EPC accounts for Rs.1,900 crore. However, post Firema’s acquisition, a slowdown in the geography has impacted Titagarh’s overall performance.

Going ahead, railways is going to be one of the biggest beneficiaries with their funding increasing 22% this year to Rs.150,000 crore. The rolling stock order flow, which was slow in the past, would again witness a renewed thrust. Railways are expected to place an order for 13,000 wagons this year. Looking at their past track record, size and capabilities, one can assume a 25% allocation of this order size to Titagarh would keep them busy for the next 30 months. The Dedicated Freight Corridor and its likely benefit for stakeholders will possibly change the way goods are transported in India. This, in turn, could be a gold mine for the company.

The other big opportunity would be in the metro space where Titagarh has proven capabilities. The Kolkata metro refurbishment would be a major project. In addition, tier-I and tier-II cities are also embracing metro rail projects. Similar opportunities overseas in countries such as Indonesia, Malaysia, Bangladesh, West Asia and Africa could be huge. The replacement of existing railway coaches with Linke Hofmann Busch coaches is another area of interest for Titagarh. Indian Railways is also expected to invite private participation in coach manufacturing, where Titagarh stands a good chance given its track record and experience.

The company’s other divisions, too, are gaining traction. It has bagged orders worth Rs.175 crore from the Indian Navy to build four vessels and a Rs.58 crore order for modular bridges in Nepal. Though crawler cranes and excavators have been a low volume business till date, they enjoy much higher margins. However, the jump in infrastructure activity across the nation bodes well for this division.

Interestingly Titagarh is also participating in a prestigious ‘Make in India’ project to manufacture 2,610 future infantry combat vehicles for the Indian Army at an estimated cost of Rs.60,000 crore. It has tied up with Tata Power Strategic Engineering Division for the project among other competitors such as M&M, Tata Motors and L&T. Cimmco, a leading wagon manufacturer based in Rajasthan in which the company had acquired in 2014, has an industrial licence to manufacture armoured vehicles, mine protected vehicles, mine clearing and launching systems. One needs to see how this pans out.

In short, the opportunity for Titagarh is humongous and with a proven track record it would only boil down, not to the quantum of orders flowing to it, but how much the company can take on and execute.

Keep the faith

After hitting a high of Rs.185 in November 2017, a Rs.39 crore loss in the December 2017 quarter, on the back of low-margin legacy orders and challenges in the overseas business, saw the stock correcting to Rs.125 levels. However, Titagarh has shown that it can turn around businesses, like the way it did with AFR, aided by a multifold increase in the topline.

The correction is an opportunity to buy into a sector that will witness exponential growth, transforming this mid-sized company into a large cap in the coming years. With a renewed focus on infrastructure, especially in railways and defence, Titagarh is expected to show 35% CAGR over the next four years. With an expected earnings per share of Rs.7 for FY20, the stock at 17x PE is worth hopping on to.

The author is an independent market expert.