Just before dawn in the Strait of Hormuz, the Indian-flagged tanker Sanmar Herald was moving cautiously with a cargo of crude when the silence shattered. Iranian patrol boats emerged from the darkness and warning shots ripped across the water.

On the tanker’s bridge, panic spread as the captain’s voice crackled over the radio, “You gave me clearance…you are firing now…Let me turn back.” Nearby, another Indian tanker, Jag Arnav, altered course as gunfire echoed through one of the world’s most strategic shipping lanes.

It was against this backdrop of uncertainty over supplies that Prime Minister Narendra Modi on May 10 urged citizens and officials to adopt austerity measures, including curbs on unnecessary foreign travel and a shift to work from home.

4 July 2026

Get the latest issue of Outlook Business

Just a day later, one of India’s richest industrialists, Gautam Adani, said, “No nation can call itself truly self-reliant if it is dependent on another country for the energy that powers its economy.” He stressed on energy security as the foundation of strategic sovereignty.

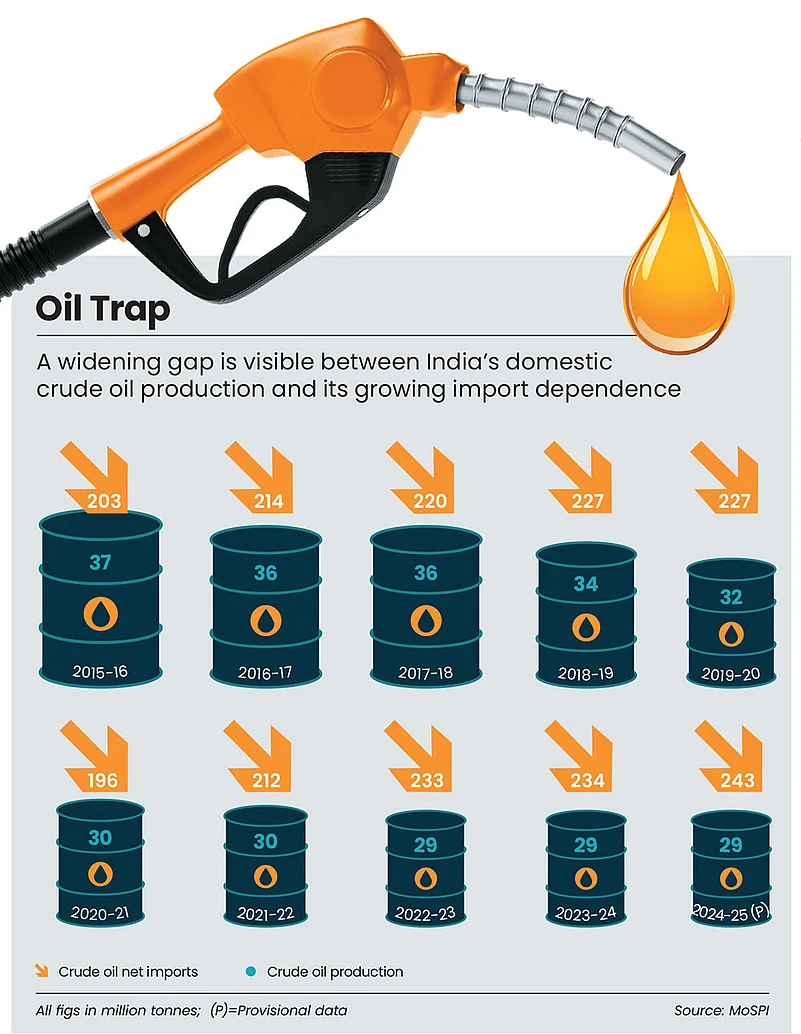

These underpin a stark reality: India has not only failed to produce more crude oil from domestic sources, it has also become more dependent on foreign supplies.

Total crude-oil production in India fell from 36.94mn tonnes (MT) in 2015–16 to 28.7MT in 2024–25, according to government data.

Rajeev Lala, director for upstream strategies and transformation at energy data provider S&P Global Energy, points out that India’s rising import dependence reflects the widening gap between rapidly growing energy demand and stagnating domestic production.

Ageing Oil Fields

The most obvious reason for the increase in import dependence is the lack of new discoveries. It was soon after the Arab oil crisis of 1973–74 that Oil and Gas Corporation (ONGC) discovered India’s biggest oil field, Bombay High, providing a boost to the energy security.

Over the decades, it has produced nearly 527mn barrels of oil and 221bn cubic metres (bcm) of gas, accounting for close to 70% of India’s domestic hydrocarbon production at its peak.

The field reached its highest production peak in 1989, when it produced around 476,000 barrels per day of oil and 28bcm of gas. However, output has steadily declined since then as the field matured.

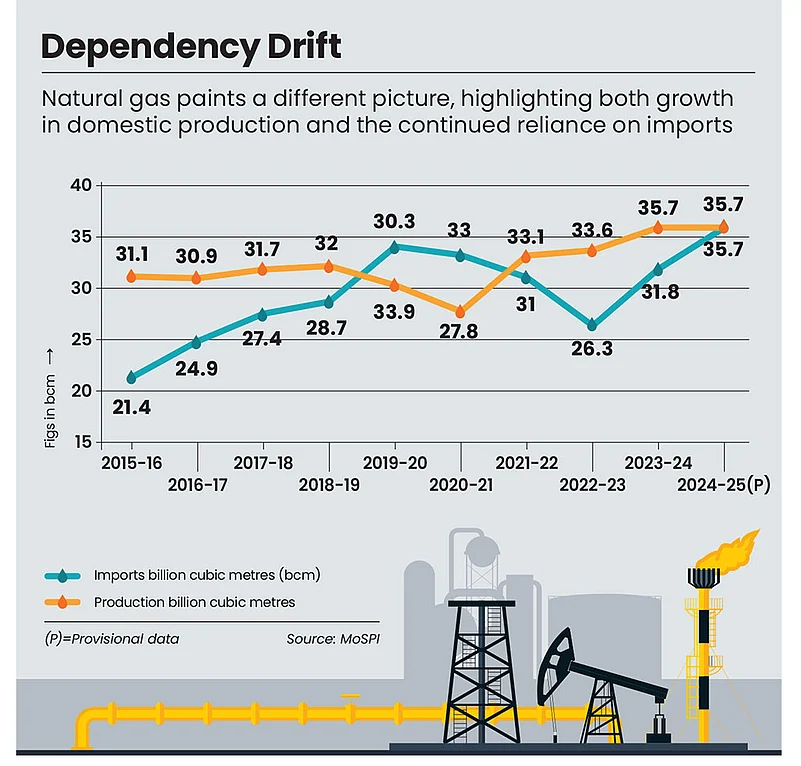

Expanding the role of natural gas can help moderate overall import vulnerability by diversifying both fuel sources and supplier bases

“Hydrocarbon assets typically follow a lifecycle of around 20–30 years, after which reservoir pressure weakens and output falls unless supported by new discoveries or major technological interventions like enhanced oil recovery,” says Manas Majumdar, oil and gas leader at global consultancy firm PwC.

Experts say that nearly 70% of India’s oil wells have reached maturity, as most of the country’s major hydrocarbon discoveries were made between 1950s and 1970s.

Besides Bombay High, fields like Krishna Godavari D6 and Rudrasagar have all passed their peak output. Onshore, key mature fields include Ankleshwar, Kalol and Mehsana in Gujarat, as well as Digboi and Moran in Assam. Even relatively newer fields like the Vedanta-run Barmer Basin are now entering a mature phase.

Today, a major share of India’s oil output comes from declining reservoirs, making enhanced recovery techniques essential and contributing to the stagnation in production.

Investment Priorities

Ideally, the upstream oil and gas sector functions through a continuous cycle: as older fields decline, companies aggressively invest in exploration so that new discoveries can sustain future production. Exploration, in that sense, is essentially long-term planning for future energy security.

However, that has not happened here. “India has not explored and developed enough new hydrocarbon resources to meaningfully offset rising consumption and the natural decline of ageing fields,” says Majumdar.

Experts say the priorities have been different. Expenditure on exploration and production by ONGC, which accounts for nearly 70% of India’s domestic crude oil and gas production, has grown much more slowly than its contribution to the government in the form of taxes, royalties and dividends.

Between 2019–20 and 2023–24, ONGC’s contribution to the exchequer grew at a compound annual growth rate of about 12.2%, while its capital expenditure rose at a comparatively modest 6.1%.

Hence, a substantial share of ONGC’s cash generation continues to flow to the government, instead of being reinvested more aggressively into upstream exploration and development needed to secure future domestic production.

Furthermore, ONGC Videsh—ONGC’s foreign arm—had overseas assets producing close to 15mn metric tonnes of oil equivalent. But several setbacks have affected that trajectory.

“It lost assets in some regions due to conflict and political instability, while investments in countries such as Venezuela became increasingly difficult to operate,” says Subhash Kumar, former chairman and managing director at ONGC.

Geographical Challenges

A related challenge is geological and geographical. At the most fundamental level, hydrocarbon availability depends on whether oil and gas were originally formed in commercially viable quantities and whether those resources remained trapped underground over geological timescales.

India’s geological profile presents certain limitations. Large parts of the country, particularly the Himalayan region, are geologically young and tectonically active, increasing the possibility that hydrocarbons may not have remained securely trapped over long periods. “The challenge is not necessarily the absolute absence of hydrocarbons, but rather the fragmented and difficult nature of India’s reserves,” says Kumar.

In the Northeast, exploration is complicated by challenging terrain, dense forests, heavy rainfall and hilly geography, all of which make drilling and logistics significantly more difficult and expensive.

“In contrast, West Asian countries possess vast and mature hydrocarbon basins with highly favourable geology with vast stretches of flat desert terrain, allowing easier drilling, transportation and infrastructure deployment,” says Kumar.

“Their reserves are not only abundant but also relatively easier and cheaper to extract, enabling decades of large-scale production and development.”

Money Pangs

The third reason behind increasing imports is that government support still leaves something to be desired.

Several initiatives like Samudra Manthan and the Open Acreage Licensing Policy (OALP) have been introduced to improve the investment climate in the upstream sector. India has opened up more sedimentary basins for exploration and sought to attract greater private and foreign investment into upstream oil and gas drilling.

However, PwC’s Majumdar says the industry response has been moderate. “Some reforms have improved things—HELP [Hydrocarbon Exploration and Licensing Policy], OALP, better data access through NDR [national data repository], revenue-sharing models, opening frontier acreage, deepwater focus through initiatives like Samudra Manthan,” he notes.

Recent crises like Iran war expose a deeper vulnerability. It’s not just volatile prices, but the risk of actual supply disruptions

Despite opening the oil and gas sector to 100% foreign direct investment (FDI), India’s track record in attracting capital remains underwhelming. It has received only about $8.19bn in FDI between April 2000 and September 2024, according to data compiled by the Department for Promotion of Industry and Internal Trade.

A key reason, Majumdar explains, is that global oil companies have multiple investment options. In 2026 alone, over 40 countries may launch or extend bid rounds, raising competition for investor attention.

If a company can deploy capital in Brazil, Guyana, the US shale basin, or West Asia, where geological certainty is higher and extraction easier, India becomes a tougher proposition. The limited response to reforms is also the result of the global energy narrative, with attention shifting toward low-carbon investments.

The regulatory environment has also been marred by clashes with investors, who look for long-term policy stability and predictability, so that profits can be repatriated smoothly over the life of the investment.

For instance, the dispute between Capricorn Energy, formerly known as Cairn Energy, and India became one of the country’s most high-profile retrospective taxation cases. The seven-year legal battle began after India imposed a retrospective tax demand of ₹10,247cr in 2014. The case eventually went to international arbitration, where a tribunal ruled in favour of Cairn in 2020, stating that India had violated investment treaty obligations. It ended with the Indian government refunding around ₹7,900cr to the company in 2022.

The Strategic Gap

Earlier, global energy disruptions were largely viewed through the lens of price volatility, with concerns centred on rising crude prices and inflationary pressures.

However, recent crises exposed a deeper vulnerability. It’s not just volatile prices, but the risk of actual supply disruptions. For the first time, commercial buyers and industrial consumers faced concerns over securing physical energy supplies, or “molecules”, themselves.

This has fundamentally altered the nature of the debate.

“Reducing import dependence is no longer merely an economic aspiration; it has become a strategic necessity linked to energy security and supply resilience,” says Sanjay Sah, leader, energy and chemicals (South Asia) at global consultancy firm Deloitte.

One important strategy in this direction is fuel diversification.

India’s dependence on imported crude oil remains extremely high, whereas natural gas imports are comparatively lower because domestic production still contributes a meaningful share of supply. Expanding the role of natural gas in the energy mix can help moderate overall import vulnerability by diversifying both fuel sources and supplier bases. India should also start shifting its focus toward deepwater exploration, particularly in frontier regions such as the Andaman basin.

“Many of India’s conventional onshore and shallow-water basins have not yielded discoveries on the scale seen in major hydrocarbon-producing nations, prompting a strategic push toward offshore deepwater areas where untapped potential may still exist,” says Sah.

Given India’s limited hydrocarbon reserves, maximising the use of alternatives like renewables, ethanol and compressed biogas is also essential for its long-term energy security.