Muhammad bin Tughlaq, the Sultan of Delhi from 1325 to 1351 AD, was notorious for taking extreme, dramatic decisions that put his subjects in misery. There were the excessive taxes to support his large army, which led to farmers switching occupation, and creating a food scarcity. Then, there was the declaration of copper currency to be on par with silver currency (to make up for silver shortage), which led to economic chaos and ultimately a big hole in the exchequer’s pocket. And the last straw: his decision to shift his capital from Delhi to Daulatabad, despite resistance from people. There was endless suffering from the journey and many died, and then he changed his mind again and decided to stick with Delhi. If there was Twitter then, #Tughlaq would have trended.

Well, the telecom regime in India resembles the sultan’s rule. With frequent changes in policy, and lack of clarity and good judgment, it has time and again inflicted pain on telcos and caused the death of a few companies. Sixteen companies in the race to provide telecom services in India at one time, are now down to three, excluding BSNL and MTNL.

The Damocles sword that is still hanging over the heads of Vodafone Idea and Bharti Airtel -— two older players — is the last pronouncement by the Supreme Court, on the contentious issue of adjusted gross revenue (AGR). The court slammed the Department of Telecom (DoT) for not enforcing its order on collection of dues, from the licence fee and spectrum-usage charges, and the telcos for not paying up.

With DoT and telcos disagreeing on what constitutes AGR, the dues have multiplied over 14 years, with the matter passed around the offices of Telecom Regulatory Authority of India (TRAI) and Telecom Disputes Settlement and Appellate Tribunal (TDSAT), and the apex court. The DoT wants the government to get a share of overall revenue, even when no money is paid by the customer, such as on discounts. Or for that matter, even on interest income on borrowed money till it is fully deployed as capex.

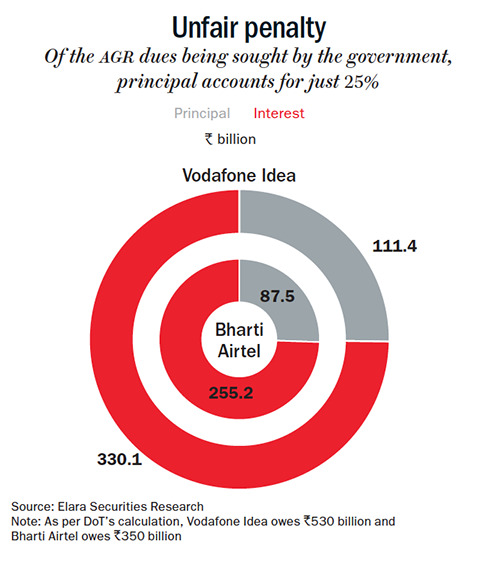

Finally, after nearly two decades of this stand-off, the bill — a staggering Rs.1.47 trillion — has now come to the telcos’ doors. It comprises 75% in penalty and interest on penalty, alone. As per DoT’s calculation, Bharti owes Rs.350 billion and Vodafone Idea Rs.530 billion, against the companies’ self-assessed claim of Rs.130 billion and Rs.215 billion, respectively (See: Unfair penalty). “I don’t know whether to laugh or cry,” says TV Ramachandran, president of Broadband India Forum, and an old hand in the telecom sector, referring to the outrageous AGR bill.

Finally, after nearly two decades of this stand-off, the bill — a staggering Rs.1.47 trillion — has now come to the telcos’ doors. It comprises 75% in penalty and interest on penalty, alone. As per DoT’s calculation, Bharti owes Rs.350 billion and Vodafone Idea Rs.530 billion, against the companies’ self-assessed claim of Rs.130 billion and Rs.215 billion, respectively (See: Unfair penalty). “I don’t know whether to laugh or cry,” says TV Ramachandran, president of Broadband India Forum, and an old hand in the telecom sector, referring to the outrageous AGR bill.

If DoT’s claim, now upheld by the Supreme Court, is to be honoured, it would debilitate or even lead to the death of Vodafone Idea — the biggest telecom operator in the country till only a few months ago. If the telco winds up, the telecom market with 800 million subscribers will become a two-horse race between Reliance Jio and Bharti Airtel. “It’s a nuclear strike,” says a telco veteran.

Numbers don’t lie

Here is how the cookie crumbles. With the current tariffs, analysts estimate Vodafone Idea’s Ebitda to be at Rs.120-140 billion. But, that will be almost entirely consumed by its capex requirements in the coming years.

Vodafone Idea’s average revenue per user (ARPU) stands at Rs.109 on a subscriber base of 304 million customers, as of December 2019. Every Rs.10 rise in ARPU will give the company incremental revenue of Rs.36 billion, and approximately 75-80% of it translates into Ebitda, which is Rs.27 billion-29 billion. Therefore, an ARPU of Rs.200 will mean an additional Ebitda of Rs.240 billion-260 billion roughly.

Now, look at the interest expenses it has to bear. Vodafone’s spectrum-related debt currently stands at Rs.900 billion; other bank borrowings total Rs.300 billion. On top of this will be the AGR liability. After the two-year moratorium on spectrum payments ends, this will cost the company roughly Rs.140 billion per year; now add to that an interest outgo of roughly Rs.30 billion on the remaining debt and another Rs.50 billion-60 billion at the least for AGR, and the total rises to Rs.230 billion. Ebitda, at an ARPU of Rs.200, will be just about sufficient to meet interest expenses, leaving meagre profit.

With some tweaks, survival may be possible, but it would be meaningless. Even if the government provides relief by deferring the AGR payment for long — 15 years as media reports suggest — it’s unlikely to solve Vodafone Idea’s problem. “The deferment could take care of liquidity, but it won’t address the question of viability,” says Rajiv Sharma, head of equity research, SBICaps Securities. “Viability will require striking out the AGR liability or a major recast of its loans, both of which seem highly unlikely,” he adds.

With such towering financial liabilities, it’s unlikely that any new investor will be interested in Vodafone Idea’s equity. “It’s not just a question of financials — the regulatory environment has shocked everyone,” says Nitin Mangal, founder, NM Advisors. “If you are not sure about the ground rules, how the hell do you compete,” he adds.

Financially, the call to invest in Vodafone Idea at this stage would require a leap of faith that the industry will climb beyond an ARPU of Rs.200 sooner than later, and more importantly, competition will be benign hereafter.

Remember that all of this is playing out in the backdrop of the telecom sector’s contracting revenue — it has fallen from Rs.3 trillion to Rs.1.25 trillion over the past three years, thanks to the tariff war after the entry of Reliance Jio. India now ranks the lowest in terms of mobile data tariffs, which clearly is unsustainable. In December 2019, the three telcos agreed to raise tariff in unison, ending the tariff war.

But, the war did not end because Vodafone Idea and Bharti were clamouring for it. It came to an end because, and only after, Reliance Jio hoisted itself as the number one player, above Vodafone Idea.

In less than three years, Reliance has catapulted itself to the leadership position from nothing. Getting to Mukesh Ambani’s stated vision of 500 million subscribers will be the next stop for Jio. But that 150 million gap will be bridged easily, at one shot, if Vodafone Idea collapses with its 304 million subscribers. To ‘Jio Jee Bhar Ke’, the pug must go — now or eventually.

Return of capital

For Mukesh Ambani, this was not a battle he would have lost. It was only a question of how quickly to win it, and at what cost. So far Reliance has deployed approximately $50 billion in the venture, far in excess of what the group had planned for, according to sources. That’s not a small number even from Reliance Industries’ perspective — it’s nearly 4x its annual Ebitda.

So far, Vodafone and Bharti have invested equity of $10.5 billion each in their Indian operations; Idea about $6 billion. Comparatively, Idea has remained fairly undercapitalised all along and deployed lesser equity, a few analysts reckon. The overall investments since 2010 is estimated to be in the range of $30 billion-$35 billion for Vodafone Idea and Bharti.

On the capital Reliance has invested, you want a return of 10%, that’s $5 billion. Assuming two-third debt, the interest alone would cost $3 billion, on a 10% rate. Therefore, the company would need an Ebitda of roughly $8 billion. If the business was operating at a generous 50% margin, that means a topline of $16 billion. If you assume a monthly ARPU of Rs.200, you’ll need a subscriber base of 500 million roughly. That’s the subsistence ARPU for Vodafone Idea, too.

But Reliance’s chances won’t look as good if Vodafone Idea survives. You don’t need to be a math whiz to understand that. If Reliance’s subscriber base continues to remain at the current level, the ARPU will have to be closer to Rs.270. Sharma believes it’s not impossible, “but it will take some time to achieve that level, given what customers are used to, and what they may be willing and able to pay.” Mangal lays it out crystal clear: “If Vodafone Idea goes under, competitive pressure will abate. But if it stays in the race, it is inconceivable why Reliance would not compete aggressively. Their debt level may be high, but their cash flows are healthy enough to give them the comfort to compete aggressively if they feel the need.” Sandip Das, former CEO of Hutchison Essar Telecom and Reliance Jio, who has seen the telecom industry from close quarters right from the early days, and also understands Mukesh Ambani having worked with him closely, says, “Things will settle down only when Reliance Jio feels it has got a fair share as the leader of the market.”

Fighting reliance

The siege by Ambani began in 2010. The telecom sector would never be the same again. That year, a non-descript company Infotel Broadband owned by Himachal Futuristic Communications Limited, rumoured to be backed by Ambani, bagged the broadband wireless licence. Soon after, Reliance bought that company for Rs.48 billion and after paying an additional migration fee of Rs.16.58 billion in August 2013 for voice services, Reliance Jio was born.

It was expected that Reliance would upset the status quo in data, not voice services. At the time, voice still constituted 80% of the revenue for most players and the operators were resisting VOIP. “More importantly, Vodafone and Idea grossly underestimated the 4G potential. They thought the long Indian tail would be happy with 2G and 3G, which was not the case,” adds Mangal.

But the Ambani company cocked a snook. It decided to blast the market with cheap-but-fast data experience, hitting the incumbents below the belt in voice by offering voice calls absolutely free. Vodafone, Idea and Bharti were stumped. Data consumption skyrocketed too. Before Jio, the average consumption had been 1 GB a month; after Jio, it surged to 18 GB; and now it has settled at 11 GB. It is unlikely to go back to pre-Jio levels.

“It was not only about cheap data. Reliance had a well-rounded strategy to build scale,” says Das. How do you really get subscribers at scale when a large number of people can’t afford a smartphone? They tied up with the Chinese handset makers, which offered the latest technology at highly subsidised prices, bundled it with a two-year subscription, along with a promise that after two years, you will get an upgraded phone if you renew the subscription for another two years. “So, they lowered the entry barrier for data-starved target segment of users by creating powerful data networks, spreading reach to Tier-II towns, and putting affordable Jio phones in pockets of people stuck with feature phones. This opened up that segment and locked them in with fixed bucket plans,” says Das. Their data plans were also intended to proliferate usage levels so that the customers got addicted to data. Besides, Reliance went only with pre-paid offerings, which were far more cost-effective.

Most people who took Jio phones initially took it only as an additional line, but gradually ended up migrating. Slowly, the other is becoming the spouse. “Reliance knows that these consumers can eventually be leveraged to drive higher ARPUs,” adds Mangal. Incidentally, it is already batting for higher tariffs.

Being a late entrant, it was anyway foolhardy to have expected Reliance to conform to any standard set by incumbents. After all, the subscribers were signed up — at the time the industry had about 800 million total subscribers. What was the chance of adding new subscribers? Zilch or nearly that. So, it had to gain market through churn. Otherwise, customers are highly reluctant to move from one network to another.

Reliance clocked Rs.201 billion in revenue in March 2018, the first full year after it launched its services in September 2016. Given the first six months of free data and voice and thereafter very cheap data prices, at least half of this revenue can be safely assumed as the amount foregone to create churn and snatch away customers from competition. By then, Jio had already signed up 186 million customers. “It was clearly predatory pricing, but the regulators turned a blind eye,” says Mangal.

Instead of sulking, Bharti decided to fight in the market. It was quick to respond to Jio’s undercutting. “Bharti was the only one who was determined not to concede ground easily and plucky enough to put up a good fight. They have always been proud and fierce competitors. They unhesitatingly augmented their data networks on 4G and matched tariffs — essentially, they just decided to match the predator to stay in the frame unlike the other two,” says Das. “Despite all the stress, they managed their balance sheet fairly well compared with Vodafone Idea,” adds Mangal.

To be fair, Vodafone had already sunk huge sums of capital into buying the company from its earlier owners. Till the merger with Idea, the telco had invested a total of $26 billion into the company — $15.5 billion into buying the stake from Hutchison (67%) and later from Essar (33%). It was also bogged down by the capital gains tax demand from the IT department of $2.5 billion, which tempered its enthusiasm for the Indian market.

Vodafone’s total investment in India has been to the tune of $9 billion, excluding the acquisition cost which went to the sellers, not to capitalise the company. “Before Reliance Jio came into the market, Vodafone could have augmented their data network like other incumbents — they were in the driver’s seat. The 900 megahertz spectrum that Vodafone owned was considerably depreciated, yet they did not make any significant investments on upgrading the network,” says Das.

The poor network affected Vodafone’s USP, of being a branded service, against Reliance’s commoditised one. “You have a poor network, you cannot retain high-end customers — it’s as simple as that,” says Das. He recalls a conversation with a senior guy in Vodafone Idea, a few months after the merger. “He went on and on about how they were focusing on brand building. He sounded to me like Marie Antoinette!” It’s only when all things are equal that brand counts, not when your services are not even in the ballpark,” says Das. The market was looking for bread, and Vodafone Idea was offering bad cake.

After Jio, it was a desperate scramble. Thus, came the merger of Vodafone and Idea in April 2017. As separate companies, Vodafone and Idea were among India’s finest — in terms of business ethics with respect to vendors, employees and corporate governance. “Even today, Vodafone and Idea can beat the shit out of competition, if they were given a level playing field,” says an angry telco veteran.

That’s true. But, it is also equally true that both did not rise to the Jio occasion, like Airtel did. “Vodafone and Idea kept up fiduciary discipline generally associated with ‘peace times’ and stable markets, but the need of the hour was to make strategic shifts to protect market share,” says Das. “I personally think they made strategic blunders, including the merger itself. Agility is more important in minefield markets rather than size,” he adds.

Sharma says the merger had bad timing. “It should have been done at least two years earlier, so the integration could have been taken care of and the company was fitter for the battle,” he explains.

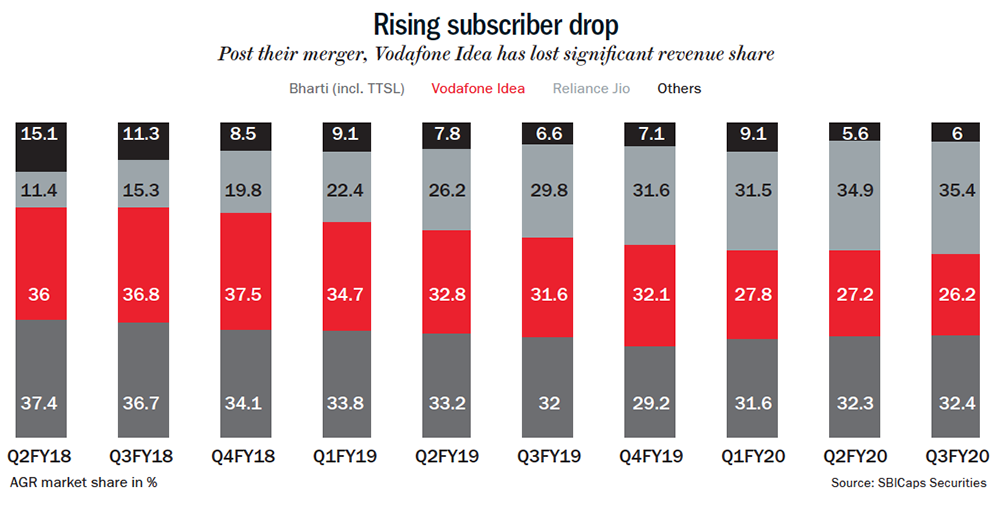

Today, Vodafone Idea looks like a hippopotamus in the middle of a muddy swamp surrounded by alligators (See: Rising subscriber drop). “They are stuck,” Das says. While Vodafone Idea prided itself in being the biggest operator, their size only resulted in bigger problems.

Today, Vodafone Idea looks like a hippopotamus in the middle of a muddy swamp surrounded by alligators (See: Rising subscriber drop). “They are stuck,” Das says. While Vodafone Idea prided itself in being the biggest operator, their size only resulted in bigger problems.

The challenges were on several fronts. “Merging networks is one of the biggest nightmares in telecom,” says R Ravichandran, a telecom engineer who has done rounds with several operators. A bigger nightmare is to manage people. “Mergers are more about chemistry rather than plain mathematics,” says Das.

The merger seemed to have achieved exactly the opposite of what was needed — a demoralised workforce and an overloaded network. The approvals took more than a year to come through, slowing everything down including capex. Even today, Vodafone Idea is at least $4 billion-$5 billion behind in terms of network investments, analysts estimate. Since the merger was effected, the company has lost nearly 100 million subscribers and its market cap has shrunk from Rs.446 billion in September 2018 to Rs.128 billion as of March 11. On cost savings, it has not done too badly though — the merger was meant to bring in Rs.84 billion, in opex synergy benefits, of which, it has already managed 85%. It is but a weak consolation.

Considering the need of the hour, the telco should have been firing on all cylinders. The new behemoth needed a CEO who had to wear three hats or three COO-level executives looking at three key aspects — manage the board expectations, convince them to raise capital and build the network; fight in the market and defend market share, especially the share of high value customers; and steer the integration process effectively, keeping morale up. It would have given Hercules a headache.

Vodafone Idea had no experienced hand. While Kumar Mangalam Birla took over as chairman of the merged entity, he was not a hands-on manager at Idea, even earlier. At the helm was Balesh Sharma, who was elevated as CEO of the merged entity in August 2018, having served as COO at Vodafone since April 2017. Earlier, he had spent five years with Vodafone Czech Republic and Vodafone Malta, rising from the ranks at Hutchison Telecom in India for many years prior to that. In a regulation-led business with high stakes, not having experienced hands at “managing the environment” has cost them dearly, say industry veterans. “The AGR issue should have been taken up at the highest level – it’s a question of survival,” says Ramachandran.

In November 2019, a day after CEO Nick Read said that “financially, there’s been a heavy burden through unsupportive regulation, excessive taxes, and on top of that, we got the negative supreme court decision” and that the company faces a “very critical situation”, he had to retract his statement as the government allegedly expressed displeasure over his comments. Neither Vodafone nor Kumar Birla seems to have strong links in the corridors of power, going by the fact that both have been busy making public statements.

There is a bit of history to Birla’s limited access. In November 2016, Delhi chief minister Arvind Kejriwal alleged on the floor of the Delhi Assembly that an Aditya Birla Group company had paid a Rs.250-million bribe to Narendra Modi when he was the Gujarat chief minister, based on a CBI search report. PM Modi refuted the claim. When NGO Common Cause filed a plea with the Supreme Court, a two-member bench rejected the plea and refused to order an investigation, on grounds that the material was “non-genuine”. Incidentally, one of the two members of the bench was Arun Mishra, who has ruled on the AGR case.

Three’s company

Vodafone Idea’s immediate collapse will be a problem for all connected to it — even competitors. Apart from having a third of the country using its services and 15,000 employees, the company owes banks some Rs.300 billion, as mentioned earlier. It has thousands of vendors of all size and scale, many of who could go deep in the red, if their dues aren’t paid. Its stock has also been decimated — languishing at Rs.4. Kumar Birla has said it will not make sense for him to put good money after bad. That’s after both Vodafone and AV Birla group ploughed in Rs.110 billion and Rs.72 billion, respectively, for a rights issue in May 2019. Vodafone currently holds 45% stake, and AV Birla Group 26%.

Vodafone Idea folding would give the other players access to 304 million customers (many of them with an additional Jio or Airtel connection), but moving those with a single connection to another network won’t be a walk in the park. First, two-thirds of the telco’s subscribers are still on 2G/3G, which means these customers will have to be upgraded to 4G, and that will entail upgrading their handsets.

So far, Bharti has never subsidised handsets, but this has been a prime customer acquisition strategy for Jio. Considering about 200 million subscribers to be migrated, and handset subsidy of just $10, that cost alone will amount to $5 billion-$6 billion. That apart, both Airtel and Jio will require additional spectrum to accommodate Vodafone Idea customers. The adjusted net present value of the spectrum, with Vodafone Idea for the residual period (roughly 10 years), is $14 billion.

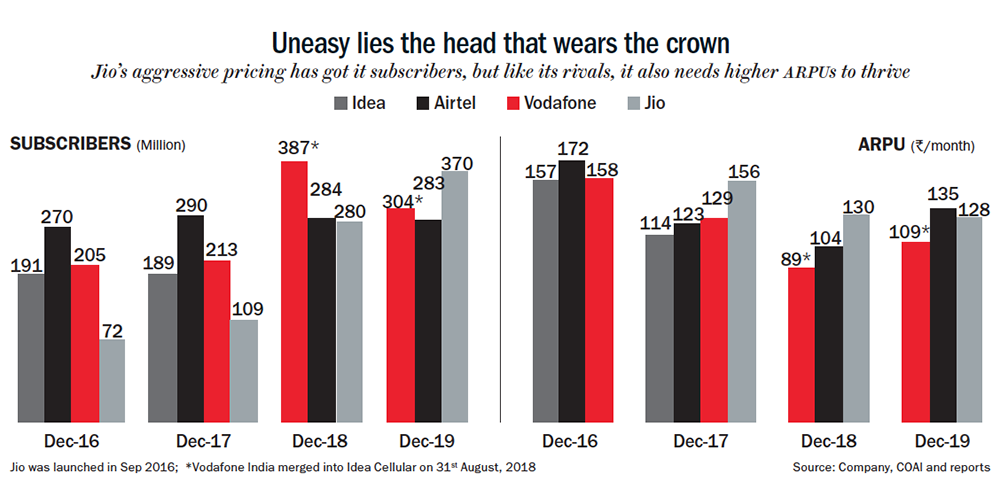

It’s not the kind of money Jio would want to burn right now (See: Uneasy lies the head that wears the crown), given the financial challenges it faces in its core business and an already stretched balance sheet. Reliance’s mainstay business of petrochemicals is not too rosy, while its group debt stands at a whopping $41.6 billion (FY19). Bharti is in no better shape to make huge spends to accommodate a big set of new customers. “But, buying spectrum is all about negotiation,” says Sharma.

It’s not the kind of money Jio would want to burn right now (See: Uneasy lies the head that wears the crown), given the financial challenges it faces in its core business and an already stretched balance sheet. Reliance’s mainstay business of petrochemicals is not too rosy, while its group debt stands at a whopping $41.6 billion (FY19). Bharti is in no better shape to make huge spends to accommodate a big set of new customers. “But, buying spectrum is all about negotiation,” says Sharma.

As for Bharti, CEO Gopal Vittal has said that the company would want Vodafone Idea to survive, and that’s not for any altruistic reason. All along, although Vodafone, Idea (before the merger) and Airtel battled each other in the market, the real war was between Reliance and the rest of the players, whether it was regulatory or in the market place. “Bharti will miss a partner to echo its voice on regulatory issues,” says Sharma.

There are tangible, financial factors too. The whole idea of shared infrastructure has helped Bharti and Vodafone Idea to keep their overall networks costs low, thus the leeway to offer lower tariffs. According to Sharma, incumbent telcos have not only shared towers but also fiber, which will be a huge cost saving factor going forward. They will also have the opportunity to share spectrum in the future. Again, Sharma says, 5G will be a lot more about densification, which will warrant high network costs, with no promise of commensurate increase in revenue.

Every which way, a distant third player with struggling economics will be helpful when it comes to negotiating with the government; the most inefficient player, after all, usually sets the minimum profitability in any sector. A two-player market may make it tricky. So far, given that Bharti Airtel and Reliance have been at loggerheads, they are more likely to settle for peaceful co-existence splitting the spoils, although Sunil Mittal will have to reconcile to being No. 2 after all these years.

That may be hard, but being No. 2 could certainly be a better deal. The Airtel brand could help in accessing and retaining high-paying customers, leading to better profitability. “This is a place where Reliance could be vulnerable, so Airtel could actually end up having a disproportionate share of high-paying customers,” says Das. In the end, both will bear the burden of having pumped in too much capital. Either won’t have a high return on equity. “This business is hardly about capital efficiency,” says Sharma. The game for the survivors will be to reduce their equity at the appropriate time and monetise when the going is good. A change in the holding pattern of these companies is imminent in the next 18 to 24 months, people quoted in this story concur.

As of now – with no money, no management, no unique idea, the die is cast for what was once India’s biggest telecom operator. It seems like a slow, painful decline for Vodafone Idea.