The Indian art market is still at a very nascent stage of development, despite the vast strides made and record prices achieved in the last few years. The secondary art market, which is a significant pillar in the evolution of the market, comprises auction houses and private dealers, with the former being the more visible part.

Indian auction houses came into play only around 2000, although Indian art was selectively auctioned by international auction houses for a decade before that. In contrast, the international art market is more than 250 years old, if one were to take the formation of notable auction houses like Sotheby’s (1744) and Christie’s (1766) as relevant starting points.

Notably, the global art market has endured the test of time, making this one of the few sectors where the market leaders have flourished for nearly three centuries, besides maintaining a close to duopolistic position.

Likewise, global wealth has participated in the art market for many centuries now, with encouraging results. For instance, the Rothschild family, which has mastered the art of managing wealth, is widely considered the greatest non-royal collecting dynasty in history, amassing an unparalleled art collection since the late 18th century.

1 June 2026

Get the latest issue of Outlook Business

While it is a popular historical rumour that the Rothschild family allocates one-third of their wealth to art, it just goes to show the level of focus and rigour with which they view their art allocation. Likewise, Deutsche Bank holds approximately 55,000-60,000 artworks, making it the largest and most significant corporate art collection in the world.

The bank actively engages with its collection, which is displayed across its global offices, besides also supporting various art programmes.

A recent study by Deloitte Private, which provides tailored services to private companies and high-net-worth individuals, examined trends and developments at the intersection of art and wealth management. A survey of family offices showed 13.4% of the wealth being allocated to art and collectibles. This trend has already percolated to India over the last few decades, with new wealth finding its way into art, in addition to the old promoter family collections and individual art patrons.

Family offices may be broadly categorised into 3 buckets, based on their evolution in art collection (which will in turn determine their requirements).

The first bucket is new wealth that is participating now in the art collection acquisition. The second category is old wealth and new infusion that is consolidating art collection.

Old wealth with historic collection forms the third bucket, which is rebalancing art collection or planning legacy.

We see some of the factors playing out in the coming years, which will drive participation in Indian art.

The increasing purchase of luxury real estate is one such factor that has resulted in a leap of buying art for consumption, also triggered by increasing collaboration between art and interior designers/architects. Many of these buyers, if well guided into the journey, will now emerge as collectors.

Another factor could be family offices come of age in India. There will be a structured approach towards creating an allocation to art, as a diversification tool.

International family offices and institutions, which already have allocation for art across various geographies, will add Indian art under their coverage.

An important factor that could play out is the Indian diaspora, which has been watching keenly on the sidelines will soon join the fray, with the increasing socio-political-economic importance of India on the global scene, resulting in increased pride and acceptance of Indian art and culture.

Collectors from China and beyond who have made significant gains on Chinese art may book profits and look for moving their capital into the next big story.

As the outlook of Indian family offices becomes increasingly global, it is important to understand the global shifts in the art market, which eventually reinforce the significant underpricing of Indian art.

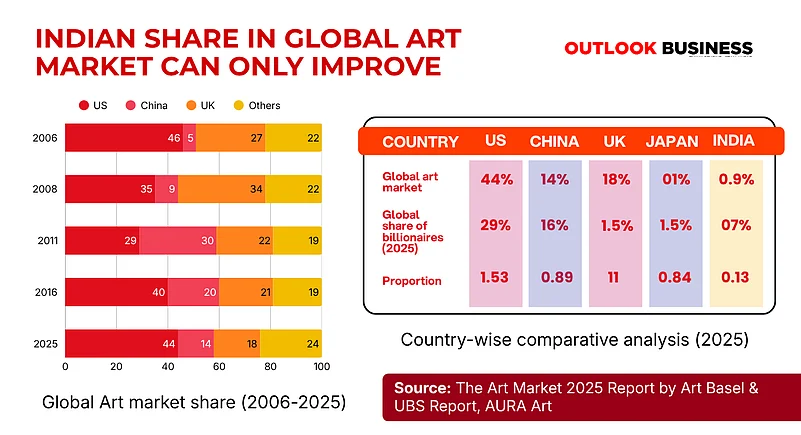

Chinese art market has had an enviable bull run from the beginning of this century, starting probably at par with the Indian art market—in the sense that both markets were insignificant in the global art scene way back in 2000. From then on, China moved swiftly to reach 9% of the global art market in 2008—while there was a market upswing in Indian art as well.

However, it is the period after the financial collapse in 2008 which is very interesting to observe. Whereas Indian art market took a breather and the US and UK art markets corrected, Chinese art market grew sharply to reach a high of 30% global market share in 2011.

The US art market has gradually recovered over the last decade, with the Chinese art market giving up some of its gains.

International collectors have been on the lookout for a while for the next big art market and given recent interest by the leading international houses to hold auctions in India as well as the record highs achieved by Indian artists in the last few years suggests that India has a fair chance to be that new market. This coupled with the increasing socio-politico-economic importance of India as well as the relatively lower prices for Indian art augurs well for the market in the long run.

After the significant milestone of development of secondary market in India in 2000, the next such milestone is development of much-needed art infrastructure, to address the needs of collectors and other stakeholders.

To sum up, Indian family offices are increasingly aware of the opportunity that Indian art presents to meaningfully diversify their portfolio. Many of them already have legacy collections, which need to be managed better. Simply revaluing these collections will reinforce the enormous wealth creation potential of art.

Besides, the soft power of art can be leveraged in many ways. The interest amongst family offices to set up art museums, already kindled by the sense of pride generated by Nita Mukesh Ambani Cultural Centre in Mumbai and Museum of Art & Photography in Bengaluru will hit a feverish high after the launch of the expanded Kiran Nadar Museum of Art in Delhi.

The writer is CA, CFA, and director, Aura Art Development