In 2023, Shreshth Mishra and his team at Simple Energy were focused on the next phase of growth. The Bengaluru-based electric two-wheeler start-up wanted to expand production, enter new markets and continue developing new products.

But raising fresh capital was a difficult peak to climb for Mishra. At the time, start-up funding had plummeted, particularly in capital-intensive manufacturing businesses.

Unlike software start-ups that can scale with relatively limited capital, electric-vehicle (EV) manufacturing demands substantial upfront investment and longer timelines before generating returns. For many investors, these were reasons enough to stay away.

1 June 2026

Get the latest issue of Outlook Business

Family offices, however, viewed the opportunity differently. Many of these investors knew what the manufacturing playbook entailed—capital intensity, operational challenges and long gestation periods. So, it wasn’t surprising when family offices led the bridge round, where Simple Energy raised $20mn, one of the largest investments in the EV start-up space.

“The funding came at a critical time for us,” says Mishra, co-founder and chief people officer at Simple Energy.

This was just the beginning as the start-up went on to raise more than $77mn in debt and equity, with a significant portion of the capital coming from family offices, including Haran Family Office, Arokiaswamy Velumani’s Family Office, Vasavi Family Office and the Desai Family Office.

Simple Energy is far from an isolated case. Family offices are increasingly becoming the top choice for founders. There are several start-ups that have been hand-held between two funding rounds or have survived because domestic investors and family offices were willing to write cheques.

Aakash Educational Services, India’s leading test-prep player, is one such case in point. In 2023, when edtech company Byju’s was embroiled in a debt crisis, Aakash being a subsidiary got caught in that storm too with foreign lenders tightening their grip over the company.

Venture investors were cautious, markets were jittery, but Manipal Group chairman Ranjan Pai, through his family office Claypond Capital, stepped in and infused nearly ₹1,400cr by taking over US-based investment fund Davidson Kempner’s debt exposure in Aakash.

These two episodes underscore a broader shift underway in India’s start-up ecosystem. For nearly two decades, the sector was built on the back of foreign capital, with global venture funds, sovereign-wealth funds and institutional investors underwriting much of the country’s entrepreneurial boom. But as overseas capital has turned more selective, domestic pools of capital have begun stepping into the breach.

Among the biggest architects of this shift are family offices that are often backing founders at critical stages when foreign investors are pulling back. The numbers reflect this growing influence.

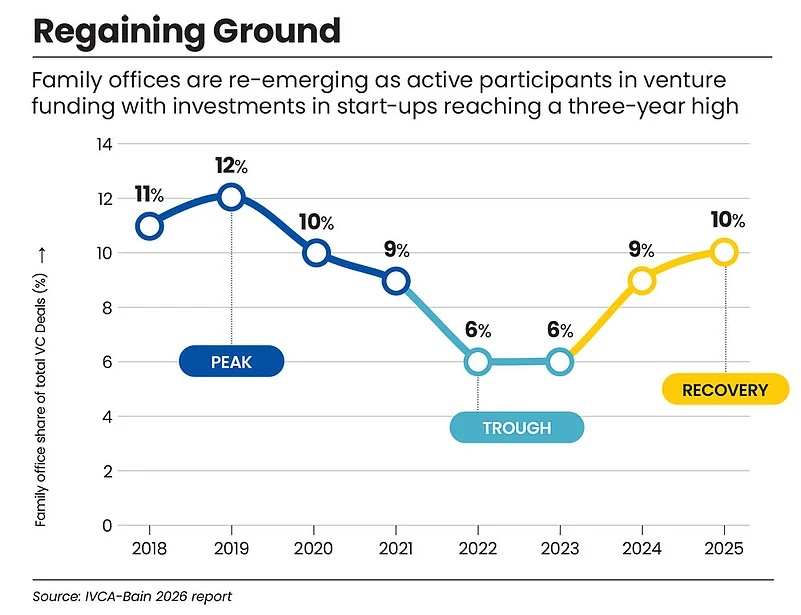

India’s family offices, which collectively manage an estimated $30bn in assets, have participated in over 1,300 start-up funding deals since 2014, according to media reports.

Why Family Office?

As family offices become more active participants, start-up founders are discovering that the value they bring extends beyond capital. “Family offices brought an understanding of what it takes to build something from scratch, the ups and downs, the setbacks and the need to stay focused on sustainable growth,” says Mishra.

Here, the founder-investor dynamic often differs significantly from traditional venture-capital (VC) relationships. Instead of being viewed solely as financial backers, family-office principals frequently become long-term sounding boards for founders.

Family offices are often backing founders at critical stages when foreign investors are pulling back

“We are not trying to squeeze founders or become adversarial. We try to become long-term partners, big brother and a positive team,” says Vivek Oberoi, actor-investor and chairman, The Oberoi Family Office.

So, family offices are becoming the connective tissue between early-stage companies and larger institutional money, adds Oberoi.

This relationship-driven nature of family office investing has become a recurring theme among founders.

In fact, family office principals remain closely involved through major business milestones and, in some cases, important personal events.

“We are not only looking for capital but also for the value, perspective and long-term thinking they bring to the table,” says Sanjay Nekkanti, co-founder and chief executive, Dhruva Space, a space-tech company.

The Start-Up Lure

India’s start-up ecosystem is the third largest in the world after the US and China. This rise, from a few hundred in 2016 to more than 1.5 lakh today, underscores the critical role private capital has played in building the ecosystem.

And family offices want to be active participants in this growth. They are drawn to the possibility of generating returns that outpace traditional investments.

Venture investors typically target net internal rate of return of 20–30%, compared with annual returns of roughly 12–14% from leading stock indices like Nifty 50 and Nasdaq, and 8–12% from real estate, making start-ups attractive avenues despite their higher risk.

Family offices are betting on this attractive return potential. They are either investing indirectly as limited partners (LPs) in VC funds or directly through their family offices.

For many families, the first point of entry was the LP route. It provided exposure to venture investing without requiring them to build in-house start-up investing capabilities. As start-up investing gained traction, the number of family offices in India grew from 45 in 2018 to around 300 in 2024, according to PwC, a consultancy.

Over time, however, many family offices began shifting towards direct start-up investments as these offer a favourable cost structure.

VC funds typically operate on the “2 and 20” model, charging a 2% annual management fee and taking 20% of profits as carried interest on realised gains. With direct investments, family offices avoid these fees, exercise greater control over investment decisions and build direct relationships with founders.

But it’s more than economics. Generational change inside family businesses has a big role in this shift towards start-ups. As younger scions returned from global universities and professional stints abroad, many found themselves more drawn to technology start-ups over traditional asset classes.

Besides, founders who once struggled to raise seed capital are now celebrated on television, social media and industry stages.

Shows such as Shark Tank only amplified this trend, turning start-up investing into an aspirational pursuit.

For the younger generation of wealthy families, backing start-ups became a way to participate in India’s innovation story rather than merely managing inherited wealth.

Generational change inside family businesses has a big role in this shift towards start-up investments

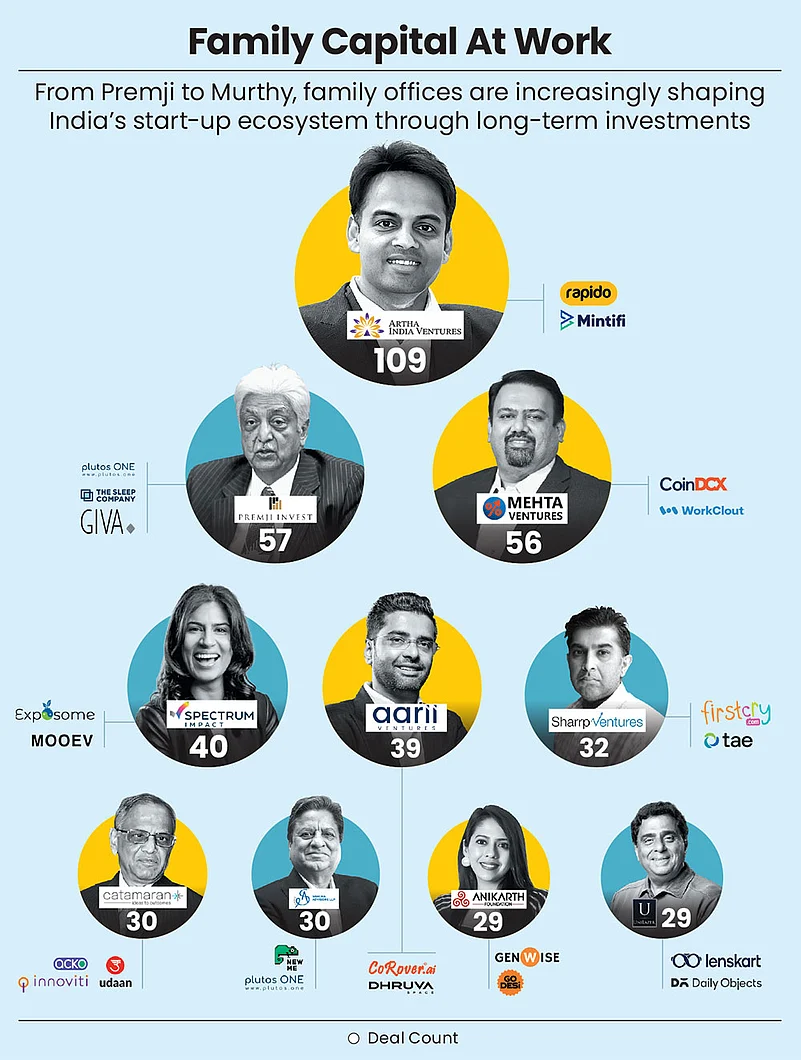

Several high-profile start-up successes further strengthened the conviction among wealthy families and high-net-worth individuals (HNIs). Anirudh A Damani’s family office Artha India Ventures’ early bet on hospitality chain Oyo in 2011 is one such prominent example. This bet yielded a whopping 350x returns on exit in 2016–17, claims Damani.

“At that time, if you told someone you were investing in unlisted companies, the immediate question was, ‘Where is the exit?’ Oyo changed that,” says Damani.

This also helped validate the VC power-law thesis, prompting more family offices to seek co-investment opportunities alongside Artha India Ventures, adds Damani.

Investment Playbook

Initially, many family offices tried to copy the VC investment playbook. However, that approach often failed because VC funds and family offices have fundamentally different objectives.

“A VC fund invests with the intention of exiting within five to seven years. Family offices don’t operate under that same timeline,” says Munish Randev, founder and chief executive of Cervin Family Office.

As they deploy their own capital, family offices are generally less constrained by exit timelines and can remain invested through multiple market cycles.

Rishabh Mariwala, managing partner at Sharrp Ventures, looks at a VC investment as a marriage with a divorce date. “With a family office, it is a marriage without a divorce date. That’s the beauty,” he says.

But due diligence isn’t the same for everyone. While larger family offices may follow VC-like diligence processes, smaller ones typically invest through funds, co-investments and club deals.

“Most family offices cannot independently conduct legal diligence, financial forensic reviews or complex compliance checks. Instead, they often piggyback on the lead institutional investor in the round,” notes Randev.

Mature family offices with clear investment processes represent only about 10% of the market, says Randev. “The rest are often driven by referrals, personal networks, founder relationships and FOMO [fear of missing out].”

Ticket-size limitations also shape family-office investments in start-ups. Smaller family offices are more active in early-stage opportunities, while larger VC funds are often better positioned to lead sizeable growth-stage rounds and take on deeper governance roles.

Money Metrics

For years, overseas investors, from sovereign-wealth funds and private-equity firms to crossover funds and global VCs, have accounted for a significant share of start-up funding.

But global uncertainty makes foreign capital more selective and unpredictable. This has renewed focus on domestic capital as a more stable funding source.

However, start-up investments still represent only a small share of most family-office portfolios. “For instance, a family office managing ₹1,000cr in assets may allocate around ₹100cr to private markets, of which ₹30–40cr could go into funds, leaving only ₹40–50cr for direct start-up investments,” notes Randev.

What’s noteworthy is that family offices are making bets on start-ups. So, the investment share in portfolios has a massive potential to grow.

At the same time, a growing number of start-ups, including quick-commerce and food-delivery companies Zomato, Swiggy and Zepto, are seeking to increase domestic ownership. This allows them to operate inventory-led models in India and, more importantly, makes it easier for family offices to offer patient capital.

Last year, brokerage Motilal Oswal Financial Services facilitated Zepto’s pre-listing round, helping reduce its foreign shareholding. Many family offices wrote cheques for the quick-commerce firm, but what’s noteworthy here is the push from scions.

“The older generation didn’t want to put money, but the new generation wanted to experiment,” says Jayesh Faria, director and regional head at wealth-management company Motilal Oswal Private Wealth.

Smaller start-ups with unique ideas will also increasingly turn to family offices as they bring knowledge, operating experience and industry networks.

Ultimately, while foreign capital built the foundation of India’s start-up ecosystem, the next frontier belongs to domestic wealth, with family offices holding the key to this evolution. Domestic capital provides the patient funding that the landscape needs.

With family offices embracing an institutional mindset, they will do more than just finance the future. They will own and shape the next generation of businesses.