Shivam Gupta did his schooling from a Hindi-medium school situated in a remote district of Uttar Pradesh. Growing up, one of his favourite subjects was English and he used to score fairly well in the written examinations. However, spoken English is where he stumbled.

This problem persisted throughout college. “Everyone used to communicate in fluent English. I struggled a lot in asking questions in class,” he says.

And this struggle laid the foundation of his entrepreneurial journey. Gupta co-founded MySivi, a spoken-English practice platform powered by artificial intelligence (AI).

1 June 2026

Get the latest issue of Outlook Business

Millions in India, including 13-year-old Arush, hesitate to speak up in class. He says even teachers did not have time to help him.

However, things have changed for the better for the 9th grader in the past few months. Arush credits learning-assistant app YolearnAI for the change as he can now learn without any fear of judgement.

Shivam and Arush represent a transition that is happening in India’s education industry. This shift is about how AI is successfully seeping into all levels of education—from kindergarten to 12th grade (K–12), competitive exams to skill-based learning.

In fact, learning use cases of AI are maximum in India, revealed Pragya Misra, head of strategy and global affairs at OpenAI, at the India Innovation Day event in Gurgaon this year.

And this growing demand is currently being catered by two edtech setups: traditional and AI native.

Traditional edtech houses platforms that existed before AI burst onto the scene at the end of 2022.

The other category is a new pool of AI-native start-ups that are learning from the mistakes made by the old wave and upgrading themselves.

The Learning Curve

Industry insiders say that traditional edtech companies never had a strong core product. They only enhanced the accessibility of an offline class from an average of 50–100 students to millions via digital mode.

But the content quality remains more or less the same, they add.

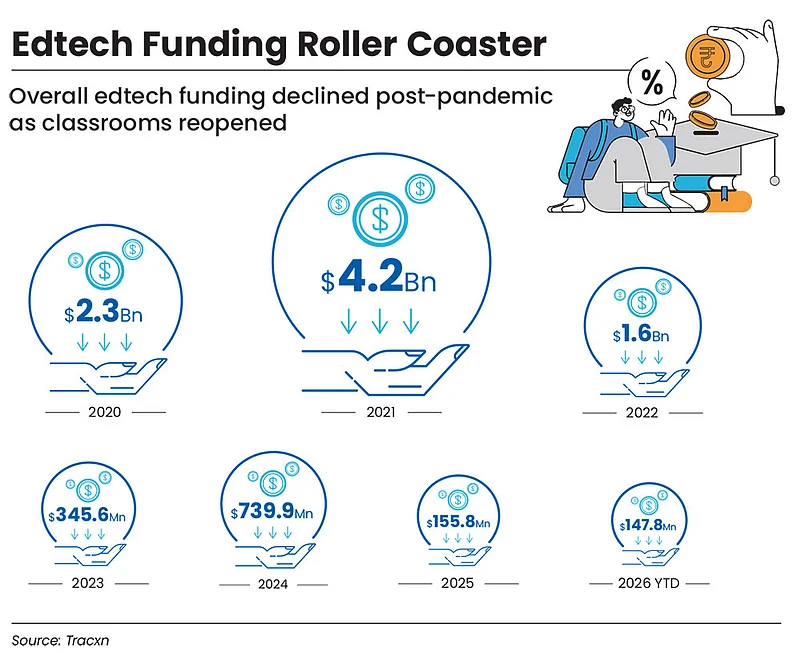

This explains why the edtech boom happened during the Covid pandemic and fizzled out as soon as the classrooms reopened.

Numbers encapsulate the decline in India with the total funding in the edtech sector dropping from $4.2bn in 2021 to around $155mn in 2025, according to data platform Tracxn. Globally, investments have plummeted from $16.7bn to less than $3bn.

This highlights that traditional edtech never attempted to solve the actual pain points of the offline framework, say experts. It was just a digital replica of the offline version, where one teacher addressed many students, irrespective of the latter’s individual requirements, they add.

On the other hand, the new edtech start-ups, currently around 61 in India, according to Tracxn, are attempting to fill these gaps using AI.

The product of traditional edtech has been unempathetic towards the learning of the student, which AI is changing inherently, says Vimal Singh Rathore, chief executive of AI mentor platform Superkalam.

AI edtech start-ups claim to provide one-on-one tutoring while having the same quality offered by their traditional and offline peers, if not better. “In the past decade and a half, we have abused the word personalisation in education to the level of criminality. But with the help of AI, one-to-one tutor that has always been costly across the world is now very much possible,” says Rathore.

Today, AI tutors can modify their teaching modules to address a student’s weak points. They can be trained on the best-of-the-best human teachers. They can then be made available to everyone, anytime, anywhere, in multiple personas, says Kirti Prakash Mishra, chief exectutive, YolearnAI.

“You can have a good AI tutor speaking Marathi and Bangla, but you cannot have a human faculty teaching fluently in Bangla the way he teaches in Hindi,” he says.

At a basic level, the core product/offering of most traditional edtech companies usually include recorded courses, live classes, test prep, mentorship, assignments, certifications, doubt-solving and career support.

However, with generative AI, the value or exclusivity of these offerings has reduced significantly. Most are almost free or a fraction of the cost at AI edtech platforms, making it far more attractive to users.

Experts say that it’s clear that AI edtech start-ups have built their product on top of this “access” with offerings designed as per the user’s profile and are far cheaper.

For instance, as of May this year, the cheapest Union Public Service Commission Civil Services Examination-General Studies course available on edtech platform Unacademy is for ₹14,736 annually (₹1,228/month), excluding optional subjects and offerings like one-on-one live mentorship, mains practice, among others.

In contrast, the cheapest plan at Superkalam is for ₹1,499 a month. Even its most expensive course is cheaper than the cheapest at Unacademy. At ₹12,999 one-time payment, the user can access all premium offerings.

“It’s almost like the capability of having a one-on-one tutor by paying a tenth or one hundredth the cost,” says Aditya Singh, co-founder of venture capital (VC) firm All in Capital.

The old wave built content libraries and tried to put a teacher on every screen. The new one is building tutors, not libraries, explains Ashish Bhatia, co-founder of multi-stage VC fund Finvolve. “The core difference is that AI platforms can offer genuine one-on-one experiences at a fraction of the cost, with feedback loops that adapt to each student,” he adds.

Evolved Business Model

The AI edtech model has several structural advantages over the traditional setup. These include limited human involvement in operations, controlled customer-acquisition costs (CACs) and scalability at close to zero marginal cost. From shooting, recording and editing content to selling, managing and running the platform, it requires minimal human workforce.

Superkalam is a great example here with just 11 employees. “Previously, we used to hear that edtech companies have 3,000–4,000 employees. But today I know many Series A, Series B, AI edtech start-ups who have 25–50 people maximum,” says Rathore.

Limited human involvement also allows to scale easily. This is in stark contrast to the traditional model, where operational costs scale linearly along with the growing student base due to the heavy reliance on hiring human teachers and support staff.

The AI-native space automates both content generation and grading, allowing it to serve millions of students globally without proportionally increasing human capital or infrastructure costs.

Some of the traditional edtech start-ups took some strategic missteps that resulted in inflated CACs. However, “the flaws were structural. CACs ballooned as every player chased the same parents on the same channels. Sales teams were optimised for closing, not for student fit, which led to high refund rates and reputational damage”, points out Finvolve’s Bhatia.

He argues that the traditional model worked for a while but when the funding environment tightened, it could not sustain itself because it was never efficient, just well-funded.

Similarly, All in Capital’s Singh notes that instead of depending heavily on large sales teams and expensive marketing, many AI-native platforms rely more on product-led growth.

The idea is that if the product is genuinely useful, the growth is going to be oraganic. This lowers AI platforms’ CACs compared to aggressive spending by traditional peers on advertisements, says Singh.

AI start-ups, adds Singh, also avoid some of the pricing issues because software scales cheaply. Once the AI system is built, serving an additional student costs far less than hiring more teachers. This allows them room to offer lower prices or freemium access without destroying margins.

Several traditional edtech start-ups have started to gradually integrate AI into their offerings. For example, Vedantu that was once purely an online live-tutoring platform, now uses AI features like ‘Ved’ to scale mentorship and personalise learning.

But the reality is that AI is still being treated as an experiment by them, say industry insiders. Even if their AI pilots are showing some success, most of their revenue still comes from live classes and recorded courses.

Hence, the focus stays on protecting and growing the existing revenue stream, says Superkalam’s Rathore. If the old wave wants to grow its AI business, that growth may come at the cost of its human-led teaching model, because the two systems work very differently, he explains.

For now, they are trying to find a balance between traditional teaching and AI instead of completely replacing one with the other.

Traditional edtech is also waking up to the reality that star faculty isn’t the biggest moat anymore. AI tutors have to a great extent reduced its value proposition. Today, there are AI tutors for almost every use case.

There are two main reasons why star faculty is a fragile moat. First is scale. “A good AI tutor can be replicated multiple times and is infinitely scalable. A human star faculty is not scalable at all,” says Yolearn’s Mishra.

Secondly, it’s costlier. Traditional edtech pays crores in packages to teachers to switch to their platform. And since these teachings cannot be scaled, there is a ceiling to the amount of return that can be generated on it.

“Skilled teachers do drive enrolment, but it’s a fragile moat. The moment they leave, a chunk of your students follow. It is closer to the film industry than to a tech business,” says Finvolve’s Bhatia.

The New Moat

Distribution remains the biggest moat for edtech as acquiring and retaining students at scale is extremely difficult and expensive. Companies that build strong distribution channels through brand recall, creator-led audiences, school partnerships, referral loops, communities or organic reach, gain a major advantage over competitors.

Even if multiple platforms offer similar courses or AI tools, the company that already has student trust and direct access to learners can scale faster and at lower CACs.

Over time, this creates a self-reinforcing advantage. “Today, building a good product is not difficult, but getting people to use the product is. So, whoever cracks distribution is going to win,” says MySivi’s Gupta.

As for AI edtech, experts believe the real moat is a start-up’s insight into its specific learning vertical and an understanding of its user behaviour.

“Whatever we have built in the past three years can easily be replicated. But our alpha is our next 10 insights and how our next three months of product road map would look like,” says Superkalam’s Rathore.

This means that successful AI edtech companies need to continuously identify and solve the next set of problems. These insights are built over time. The defensibility comes from user insight, workflow integration and speed of iteration rather than from the technology layer alone.

The moat, therefore, lies in a start-up’s ability to stay closer to the learner, anticipate evolving pain points and keep building solutions faster than competitors can imitate them.