A diamond is forever. This marketing slogan from 1948, from the biggest diamond house in the world De Beers has come to be accepted as gospel. Earlier the stone was considered a luxury, but the ad campaign made it a must-have for anyone promising eternal love. It did wonders for the industry, which is today worth more than $80 billion, and Surat is an integral part of it. It cuts and polishes nearly 90% of the diamonds globally. The city’s Rs.1-trillion industry runs on 5,000 odd units, which employs upwards of 600,000 people.

“Fresh piece aaya hai,” says an excited Chandrakant Tejani, director, JR Exports and his father immediately gets to studying the small piece of stone placed on his table. The traffic din in Surat’s Mini Bazar is merciless and conversing over it is trying. It is difficult to reconcile the cacophony with the commercial centre’s formidable reputation in the international, luxe market. Tejani shuts the window before turning the air conditioner on.

1 May 2026

Get the latest issue of Outlook Business

Tejani represents the quintessential Gujarati businessman. The 47-year-old is a third-generation entrepreneur with a sharp understanding of the business. He travels extensively and is tight-lipped about his revenue. “Business was not very good till last September. Post Diwali, it has really taken off,” is all he says. The fresh stone on his table is a 1.3 carat piece and will sell for Rs.700,000-800,000 in the market. Tejani believes growth will continue for a while before taking a turn for the worse. According to industry reports, festive season in the US and Europe coupled with units slowing production in Surat boded well for the industry in the last two months of 2019. But although Bain & Company expects India’s long-term growth in this space to remain intact, it stated in its latest report that, “Ongoing currency fluctuations and short-term policy changes in India could disrupt that country’s potential, as they have in the past.” Tejani is not perturbed. “Phases will come and go,” he says philosophically.

He is referring to the time prices fell due to supply glut after 2010. Production had increased by 15% as new players entered the fray, but as many as 500 units had to shut shop since demand didn’t match supply. When capacity levels were cut drastically a year ago, demand still didn’t take off due to several geopolitical reasons. Larger players like Tejani have mostly been unaffected by this, like they have always been through every headwind, but smaller enterprises are despairing.

In the rough

Each year, the Hong Kong Jewellery & Gem Fair in September is a grand affair, where buyers and traders from across the world discuss the latest trends and showcase their innovations. It’s an ideal platform for Surat traders to connect with prospective clients. “Hong Kong sets the tone for our future business, but the event last year was a huge disappointment,” says Chirag Virani, Director, B Virani & Co, who is a regular here.

The civil unrest caused a 15-20% drop in turnout, worsening the already pessimistic mood. Trade war between the biggest nations hasn’t helped either. China is Surat’s second largest market at 35% of total diamond exports, which then uses the polished diamond to export jewellery to the US. But with higher tariffs, China’s exports to the US have taken a hit. In turn, it has affected demand from China itself. The whole saga meant orders for Christmas, which would normally trickle in by August, fell by more than 15%. “Obviously, we were extremely worried. What was unusual this time was the duration of the slowdown and we have never seen one last for more than a year,” says Virani. The aforementioned Bain & Company report explains that aside from the current slowdown, the diamond market has faced only four recessions in the past 50 years, but the market typically returns to normalcy within a year.

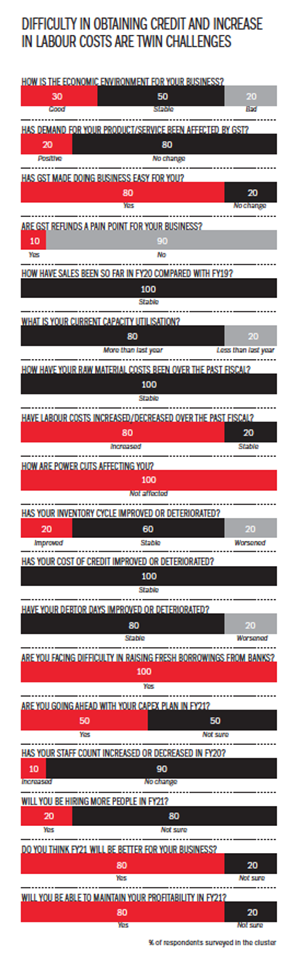

Back home, the liquidity picture has not been pretty, especially since the Nirav Modi fiasco. Banks are too scared to lend to jewellers, and credit to the sector has fallen from Rs.650 billion in 2018 to just over Rs.500 billion in 2019. “Neither credit nor demand only complicated things further,” he adds.

Small is not beautiful

Dinesh Navadiya, who runs Tiku Gems and is regional chairman (Gujarat), The Gem & Jewellery Export Promotion Council (GJEPC), points out to one more factor — unpreparedness for a slowdown. “It was just assumed that the party would go on forever,” he says. That includes not investing in skill development or technology as much as they should have. And it has hit the smaller players hardest, who form 90% of the industry but only have 40% share in the revenue generated.

The smaller enterprises cannot afford to employ skilled labour, and with a turnover of less than Rs.50 million, most have as few as two people and rarely more than 40. While smaller traders pay around Rs.15,000-20,000 to their workers, a skilled person can easily make over Rs.30,000 at a larger diamond house. “There are some who earn Rs.150,000 per month in Surat,” says Navadiya.

For years, these craftsmen have polished diamond manually. To get ahead in the race, many big companies have adopted auto-polishing. In his swanky office, the 30-year-old Nikunj Shankar, director, Shivam Jewels, elaborates on how this is transforming the story. “Earlier, it would take five days to get a diamond polished. With an auto polishing machine, it can be done in two days,” he says. Of course, the scale of his operation (875 employees) gives him the leeway to invest that additional Rs.2 million in the machine. “If you can manage the business smartly, the money can be recovered in nine months,” he adds confidently.

Shankar believes every player must offer a clear differentiation because, honestly, the margins have dropped from double digits to 1.5-2% and this may not change. Diamonds are no longer exclusive. “The differentiation has to be technology or the ability to procure the rough diamond at a lower price,” he says.

On the other side, in a dimly lit room, Rutul Moradia’s smile is the only sparkle. He employs 30 workers in his unit and they quietly go about polishing the diamonds. For two years, their wages have not increased and Moradia smiles wryly when he speaks about it. “There has been no business to speak of in the past three years. I have never been so worried,” he says.

Loud Bollywood music plays throughout our conversation and that appears to be the only reason for cheer among the workers. Moradia’s unit is called Rutul Enterprises, a part of the fraternity of small units, with his making a turnover of less than Rs.50 million. The limited scale is a bane for the business and he candidly admits it. “Our consumption is completely in and around Surat. Maybe we need to invest in technology, but where is the money to do it?” he asks.

A rock and a hard place

The other monster in the room is the rise of synthetic diamond or more often called CVD (chemical vapour deposition) that started two-three years ago. For true diamond enthusiasts, they are ‘fake’. Made through a controlled process in the lab, these are not extracted from a rock and cost 70% lesser than natural stones. Jayesh Patel, director, MV Enterprise and an old industry hand, sneers at them saying a consumer looking for quality will not buy a synthetic deposit.

While several units have started making lab-grown diamonds in Surat, Navadiya says that it is not being done in an organised manner. Since large players don’t target price conscious consumers, it’s mostly the smaller players who are trading in it. He adds that they deal in 0.01 to 0.10 carat segment, with only a handful selling one-carat diamonds. While the average ticket size is Rs.15,000, the artificial variety can come as cheap as Rs.6,000 a piece. Makers of CVDs are asking for the right to trade on the diamond bourse, but are facing resistance from the larger players who are fearful of losing their dominance.

They are rightfully afraid. As the economy hits mid-income consumers’ spending power, many are gravitating towards the cheaper option. Jhanvi Enterprises’ Arvind Vaghani is just about the size of Moradia’s worriedly explains that of every 100 buyers who approach him, at least 30 show a marked preference for the artificial version today. But he remains reluctant to make that change. “I know nothing about it and have to learn from scratch. It is a challenge after spending over twenty years in the real diamond business,” he admits.

For now, the mid-sized and large players are thrilled about the demand post Diwali. Traders say it has been a spike of 10-15% and pray for what will be at least a “stable” business scenario. Virani, who does business worth Rs.350 million annually, sounds a word of caution. “Oversupply is now correcting to equilibrium. We are getting a lot of enquiries but we will need to see how long it can hold out,” he says.

Moradia meanwhile is unable to relate to the recovery and says his business is now only a ‘zabardast tension’. Of his ten ghantis (the table where the workers polish diamonds), three have remained unused for over two years. “That investment is useless now and I don’t know how the staff will be employed in the future,” he laments. Neither Moradia nor Virani know how the story will play out, though they hear that diamonds are forever.