In movies, an aircraft landing bumpily on a poorly built runway that ends in single-cabin office suggests a hick town. The protagonist has arrived in the back of the beyond. Over the years, airports have come to convey the poverty or prosperity of a city or a state. They are no longer mere transport hubs, with empty hours of waiting. They are vibrant spaces, where travelers are invited to engage with local history, art and food. One such is Indira Gandhi International Airport in New Delhi, with its famous hand sculptures.

In movies, an aircraft landing bumpily on a poorly built runway that ends in single-cabin office suggests a hick town. The protagonist has arrived in the back of the beyond. Over the years, airports have come to convey the poverty or prosperity of a city or a state. They are no longer mere transport hubs, with empty hours of waiting. They are vibrant spaces, where travelers are invited to engage with local history, art and food. One such is Indira Gandhi International Airport in New Delhi, with its famous hand sculptures.

The airport has earned accolades as one of the world’s best, year after year, with its Terminal 3 built in a record time of 37 months, just before the biggest sporting event that Delhi hosted — Commonwealth Games in 2010. It is operated by Delhi International Airports, which is a subsidiary of GMR Airports, the fourth largest private airport developer in the world.

It is in the thick of things, as the Indian government has recently unveiled plans to develop 100 greenfield airports by 2024. Air passenger traffic has more than doubled in the past decade and has seen a healthy double-digit growth over five years. As per a FICCI report, total air passenger traffic in India should grow 6x by 2040 to 1.1 billion at a CAGR of around 9%. The total number of operational airports may rise to 200. In the same period, global passenger traffic is expected to double by 2040 and reach 19.7 billion.

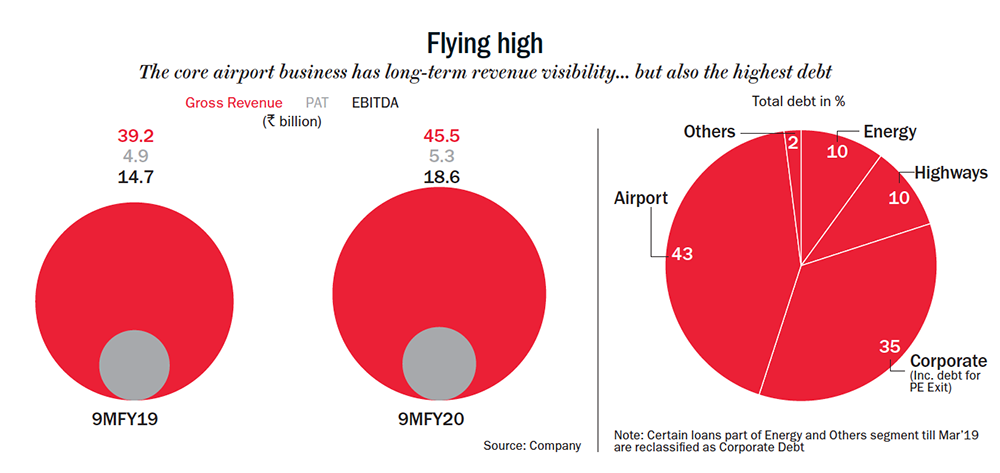

The airport business offers long-term visibility with a stable regulatory environment (after extensive regulatory experimentation). The revenue model is well diversified with non-aero revenue ranging from retail, food and beverages, cargo, rentals, advertisements and ground handling in addition to the regular aero revenue. GMR Airports has consistently performed well with FY20E Ebitda margin higher than 40% (See: Flying high). Globally, airport stocks are valued at around 18x EV/Ebitda. Despite the advantage of India’s higher growth rate, using the same yardstick would value GMR Airports at EV of Rs.500 billion.

However, GMR Airports is not listed, thus one needs to play this theme through the listed holding company GMR Infrastructure. The listed entity has had a tumultuous journey during the past decade, after initially being a much sought after infrastructure stock when it was listed in 2006. In addition to investment in airports, like many others who were riding the infrastructure wave, GMR stretched its balance sheet by committing big to energy and highway projects. The downturn in the economy post the Lehman Brothers crisis, the regulatory overkill and unkept promises such as PPAs as well as gas supply for power projects turned out to be its nemesis. The silver lining, however, were the airport projects that continued to be cash-positive.

However, GMR Airports is not listed, thus one needs to play this theme through the listed holding company GMR Infrastructure. The listed entity has had a tumultuous journey during the past decade, after initially being a much sought after infrastructure stock when it was listed in 2006. In addition to investment in airports, like many others who were riding the infrastructure wave, GMR stretched its balance sheet by committing big to energy and highway projects. The downturn in the economy post the Lehman Brothers crisis, the regulatory overkill and unkept promises such as PPAs as well as gas supply for power projects turned out to be its nemesis. The silver lining, however, were the airport projects that continued to be cash-positive.

The past 10 years were spent fire-fighting, after which the management seems to have clarity on the way forward. They have decided to focus on the fledging airport business and divest the rest of the businesses at an opportune time. However, to immediately reduce the debt burden and clean the balance sheet, they have divested 49% of the airports business to Aeroports de Paris (Groupe ADP) at a post-money valuation of Rs.220 billion, which is about Rs.40 billion higher than their earlier agreement with the Tatas. Earn-out achievements may add another Rs.45 billion in due course.

GMR Infra would utilise part of the Rs.100 billion it receives from Groupe ADP, to reduce debt from Rs.95 billion currently to about Rs.25 billion at the listed entity level. It has also been able to divest the 1,050 MW Kamalanga Thermal Power Plant to JSW Energy with an equity payout of Rs.12 billion and made a similar divestment of Chhattisgarh Power project in 2019 to Adani Power at zero equity value. The road project vertical is self-sustaining. The other thermal projects, too, are self-sustaining with some of them providing a positive cash flow. The Rajahmundry Power Plant, which was an albatross around its neck, where it has 45% equity, has been able to go through a resolution plan and the debt has been brought down to sustainable levels. GMR is in a position to clean the balance sheet across verticals.

A closer look reveals some hidden wealth in the backyard. GMR has 10,400 acres of port-based land at Kakinada in Andhra Pradesh with eight kilometres of coastline, which will be developed into a port by a third party utilising 2,000 acres. Another 2,500 acres may be developed as a mega petrochemical park by HPCL, GAIL and Haldia Petrochemicals. They also have 2,500 acres of land at Krishnagiri in Tamil Nadu. A special investment region is being set up on 600 acres in collaboration with TIDCO. The land should be in demand when global majors look for alternate regions for their manufacturing facilities post the Covid-19 scare and the US-China trade spat. Even assuming a paltry Rs.5 million per acre, the land value works out to Rs.65 billion. Additionally, there are claims of Rs.39 billion pertaining to the road assets against government authorities which, when realised, will be added to the bottomline. There is also a 30% interest in PT Gems Coal Mines, which was acquired for around $500 million in 2011.

Over the next two years, we should see the clean-up being completed. The airports business will drive the group valuation with a possibility of GMR Airports being listed independently and GMR Infrastructure shareholders directly holding the 51% currently (could go up to 59% with earn-outs) held by the holding company. This could unlock huge value. Though Covid-19 is a risk factor for the airports business due to travel curtailment and lower footfalls, I would prefer to be an optimist looking at life beyond the next three to four months.

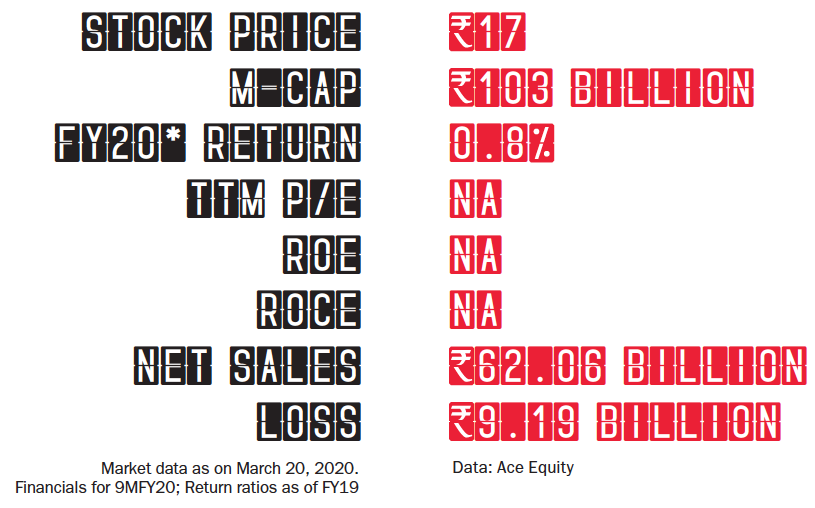

The stock has corrected sharply by 33% due to the Covid-19 scare, making it an opportunity to buy for long-term growth.