There is no such thing as easy money. If there was, he wouldn’t take it. One of India’s longest-serving mutual fund managers and the only one managing the same fund for more than 25 years, Prashant Jain has not won his formidable reputation by merely piggybacking on trends. Quite the contrary. He is inclined to swim against the tide. Exhausting it can be, but the good part is the tide does turn. The bad part, you never know when.

It has been a draining few years for Jain, paddling and kicking against the stock market movement, but not anymore. The current seems to have turned in his favour, finally. His funds are back right on top of the table. His longest-running fund, HDFC Balanced Advantage Fund, has reclaimed its numero uno position across all time periods. It has delivered return of 51.3% over the past year ending June 30, 2021, against the category average of 27.03%. Equity fund HDFC Flexi Cap Fund has delivered return of 66.01% over the past year, ahead of the category average of 55.31%, making up for its shortfall in performance over the past five years. It leads the pack over a 20-year period with an annualised return of 21.89% compared with the category average of 19.19%. HDFC Top 100, with 54.89% return over the past year, has surpassed the category average for the period but still has a gap to fill over the past five years. Over a 20-year period, its return is significantly better at 21.06% compared with the category average of 16.45%.

That heavy-duty performance has come on the back of two things. First, his decision to increase equities exposure to 85% during the market drawdown in March 2020, helped his balanced fund make a supersmart recovery. You can either commend that because asset allocation is key to generating investment return or question that saying 85% equity exposure was ‘too risky’ given the fund’s ‘balanced’ mandate.

The second reason for the comeback, which helped all his equity funds, is the “value trade” that had grossly underperformed in the past few years is now back in favour. Notably, stocks of economy-oriented companies including corporate banks, industrials, commodity companies and public sector undertakings are back in the reckoning after a prolonged lull.

3 February 2026

Get the latest issue of Outlook Business

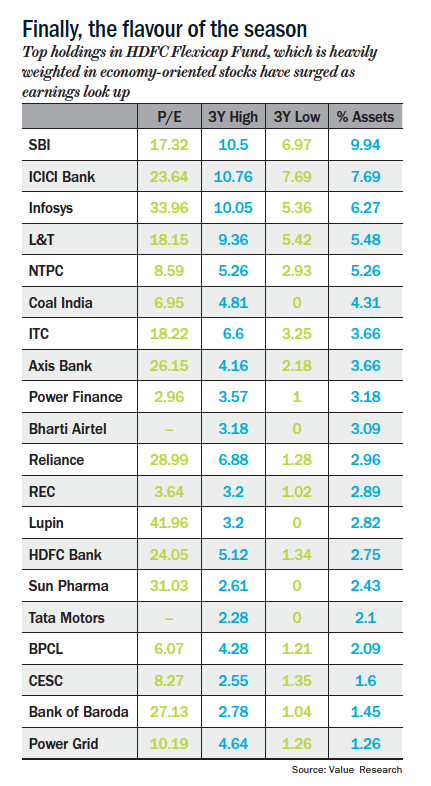

Currently, some of Jain’s biggest bets are in the power sector, including Coal India, NTPC, Power Grid, PFC and REC, besides SBI which is his top holding. Jain also has exposure in a slew of other state-owned companies including BEML, GAIL, Bharat Dynamics, BPCL, HPCL, and notable additions have been made in recent times with HAL, BEL and ONGC. Many of these stocks have generated a remarkable return over the past one year (See: Finally, the flavour of the season). “Stocks that were seen as contrarian bets till some time ago are no longer seen as contrarian, but still offer value. Others that offered value are now fairly-priced or even overpriced in some cases,” says Jain.

While other investors chasing momentum are now joining this bandwagon, Jain feels vindicated, as the bets that had given him and his investors much grief over the past few years are finally paying off. “Over the past few years, his funds barely managed to beat the index and struggled to keep up with peers because of a polarized market,” says Dhirendra Kumar, founder and CEO, Value Research, a firm tracking mutual funds. The extended pain period has also dragged down his long-term return significantly, now averaging 18.08% per annum since inception (February 1994) for Balanced Advantage Fund, 18.43% for HDFC Flexicap Fund (since January 1995) and 19.19% for HDFC Top 100 (since October 1996). In March 2008, HDFC Top 100 Fund was averaging compounded return of 27% per annum since inception, while Flexicap Fund and Balanced Advantage were averaging 23.60% and 22.42% per annum. These are long-running mutual funds, with the first two more than 25 years old.

Despite the knock Jain has taken, his return is among the best any public fund manager in India has generated over such a long period. “The initial periods of outperformance were incredible for Prashant. That has helped him sail through such a tough phase,” says Kumar. There is a contradiction in Jain’s performance: while he remains ahead of the pack with his long-term track record, his performance in recent years have dragged down his own average significantly.

Of course, it is harder to maintain the level of outperformance over long periods, especially with a burgeoning corpus–Jain still manages the biggest funds in the Indian mutual fund industry (See: The cycle of mutual fund performance). Therefore, his task is harder. Jain, however, does not agree that size is a deterrent to performance. “More than size, it is about the market opportunity. Those high returns were possible because, in IT, companies grew at 50-100% for many years. Ditto in the run up to the 2008 crash, when infrastructure and other economy stocks grew phenomenally. Those kind of opportunities do not exist anymore,” says Jain.

Truth be told, Jain is one of the few managers who has not been swayed by market conditions and has exemplified rationality and demonstrated valuation discipline throughout his career, including in the past few years when the market seemed to overshoot in pockets. So, what lessons do this celebrated manager’s prolonged pain period and his eventual comeback have for investors and professional fund managers?

Value divergence

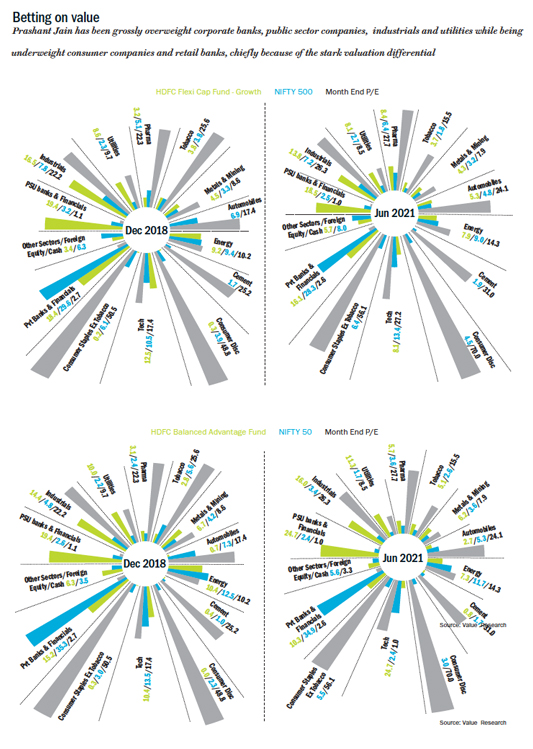

Since 2014, Jain took big bets on corporate banks and the industrial sector and went severely underweight on private banks, betting on a recovery in corporate banks driven by the new bankruptcy code. According to data sourced from Kotak Institutional Equities, in December 2014, while PSU banks and financials had 4.8% weightage in the Nifty, Jain’s portfolios had weightage of 18-22% in the three key funds – Top 100, Flexicap and Balanced Advantage Fund (See: Betting on value). While Nifty had whopping 27% weightage on private banks, his funds had 7.7%.

Similarly, his weightage on industrials, too, diverged vastly from the benchmark index. It was nearly 10.6%-17.7% in the three funds, when the Nifty weight was only 5.2%.

Hindsight, though, is always 20/20. And it is easy to bracket decisions as right or wrong based on outcomes and new realities. But Jain had made his contrarian call and his defence was that the valuation differential would get bridged when the performance of public sector banks improves with the Insolvency and Bankruptcy Code, accelerating bad loan resolution. Private sector banks were trading at nearly 3x book while SBI was trading at less than book value, despite the value embedded in its subsidiaries like SBI Life, SBI Cards and SBI Asset Management.

That reasoning was not totally out-of-whack. In 2014, when the country voted into power a majority, BJP government, the market gave a big thumbs up since big reforms and better governance were expected, and India’s potential to clock growth closer to 10% was to be unleashed. In such an environment of optimism, few could have foreseen the biggest corporate banks, watching from the sidelines, trying to clean their mess for the next six years.

Jain admits that not factoring in potential delays in the IBC process was a mistake. While poor governance of the IBC and the consequent delays ensured that the struggles of the corporate banks with bad loans continued, the mayhem caused by demonetisation and ill-designed GST battered economic growth and further compounded the problems for banks for years. Private capex came to a halt, the economy went into a downward spiral and, not only did corporate banks continue to bleed, industrials and commodities companies languished.

Profit growth for all sectors disappointed – corporate banks, metals, power, capital goods, automobiles and pharma included. Only consumer and tech companies, and retail banks continued to post steady growth.

Unsurprisingly, with that pall of gloom, the popular vote in the stock market went to those with pretty-looking balance sheets, stable cash flows and respectable growth. “Because of the absence of growth in the economy, the valuation differential between these two buckets – consumer and economy-related – became even more accentuated,” says Ashish Gumashta, managing director and CEO, Julius Baer India. Consumer stocks went through the roof and those that were unable to show a healthy bottomline were shunned.

The index weights reflected the new reality. Private banks’ weight in Nifty went from 27% in December 2014 to 40% in December 2019, where Jain was grossly underweight. More specifically, much of the gain came from retail banks where Jain had no exposure. Ditto for consumer businesses, where index weights nearly doubled since 2015 but where Jain had cut his exposure to zero.

While near-term earnings visibility does feed into market sentiment, the operating environment got stronger year-after-year for consumer companies. Be it the GST rate cut or the corporate tax cut, policies kept fortifying these companies’ bottomline, which kept raising their valuation. “When the market overshoots, it is never because of just one event. It is a progression,” Jain admits.

Another key factor that played in favour of consumer companies was the reducing cost of capital, which made it easy to justify high valuation for stocks with reliable long-term growth rates.

India’s risk-free rate is down from 8.8% in 2014 to 6.1% currently. So for a company like HUL, cost of equity is down from about 12% to 9%. Interestingly, while cost of capital theoretically should alter valuation of all businesses equally, it does not quite work that way. It is far more favourable to secular businesses with high entry barriers (read brands, tech and such) than businesses whose return is intrinsically linked to interest rates, such as utilities where return can dip with a fall in interest rates over a period of time, or businesses that are price-takers such as commodities, where new suppliers can come and depress overall return and growth.

Prolonged pain

In any case, it was easier for investors to place greater faith in India’s consumption story than in India’s investment story. The near-term reality and long-term visibility in earnings, the free-cash-flows and the intuitive appeal of the sector perpetuated the positive narrative for consumer stocks. “By the way, several of those consumer stocks were what Prashant bought far ahead of the market when these stocks were going at less than 20x earnings back in 2007, when the market was smitten by infrastructure and real estate. But he started selling them when they hit the valuation ceiling of 40x-something,” points out Kumar.

As investors were besotted with the ‘quality’ basket, PSU stocks and industrials went the other way. The narrative was getting weaker on the side Jain was bullish. Apart from the extended pain in corporate banks, the performance of public sector companies suffered a severe blow because the government decided to disinvest through exchange-traded-funds (ETF). Strategic sales would have ensured that the companies were valued at their true worth, but the government taking the ETF route to offload stocks and offer discounts on already depressed prices of PSUs only dragged stocks down even further by increasing the free float. “The sentiment towards public sector companies was negative despite their businesses doing fairly well,” laments Jain.

Although he says that these companies maintained their lead position, there was no denying that the government was destroying value by dumping stock instead of realising the best value for its assets.

As the market got more and more polarised, Jain’s confidence in the trade grew stronger and he decided to go headlong in the other direction, shows data from Value Research.

The strategy has worked unfailingly for him in the past. In 1999 and 2007, Jain had exited the flavour-of-the-season stocks and hopped on to undervalued stocks ahead of the market peak. These moves caused a period of underperformance, but they proved to be correct, saving lots of money for his investors and keeping his performance leaps ahead of others. He had learnt a lesson: betting against a polarised market will pay off but you have to be prepared to live through a period of pain.

This time, when a similar situation presented itself, Jain responded as he had earlier. However, he was betting blind on one thing: how long the polarity could continue and, therefore, when the pain endured will pay off. To be fair, ‘when’ is not an easy question to answer. Interestingly, legendary investor Howard Marks says he steers clear of forecasting ‘when’!

Jain’s strategy of digging his heels deeper by favouring the out-of-favour and shunning the favoured landed him a double whammy. Some key stocks he sold out continued to soar and those he piled up went the other way, dragging down performance. Until last year.

Reverse tide

“As the earnings story has turned around in other sectors such as commodities and there is greater optimism around the investment-led story driven by higher public spending and government incentives, the focus has shifted once again, after a rather long spell,” says Gumashta. The government recognising the damage done to asset value, from sale through the ETF route, and the market anticipating aggressive strategic sales have infused a fresh lease of life into PSUs.

None of Jain’s bets though were or are on companies with a lousy business or crazy valuation, the usual deathbed for investments. “Jain’s research is significantly superior to any other fund house’s,” says Gumashta. “His understanding of businesses has always been superior and every time he explained his calls it was based on solid data and research. Their research is deep, very deep. It convinced us that the strategy will pay off eventually.”

Even Jain’s critics argue that, fundamentally, the calls by and large were not misplaced. But, they say, he doubled down on his exposure when there was no reliable signal of reversal and prolonged his pain period. Unsurprising for believers in the strategy and bewildering for others, that is what saved the day for Jain and is the chief reason for his remarkable comeback.

“Most investors prefer to take comfort in the direction of the price movement. It comes down to your temperament. The market went against us but we believed in the businesses that we had bought into, so the logical thing to do was to stick to our research and stand by our principles,” says Jain defending his call. “As for consumer businesses, they were overvalued then, they are overvalued now,” adds Jain. Agrees Manish Chokhani, director, Enam Holdings and a highly respected voice in the stock market. “You have to differentiate between good companies and good stocks. We all agree those quality companies are great, but if you buy them at 90 P/E, you cannot expect to make a return,” he cautions.

When you stray from your philosophy or capitulate, you run the risk of a market reversal after you have exited your position. When you change track based on market sentiment, not validated by business fundamentals, the risk is especially pronounced. “I dread to think what may have happened if I had given into sentiment last year,” says Jain.

A relatively young but astute fund manager, who has been occupying the top slot for the past decade consistently, concurs with the view. “Their research and investment process are top-grade. In fact, we aspire to do the same in terms of process and rigour. It has been developed and fine-tuned over many years. The fundamentals of the stocks they picked therefore are unquestionable.” Not just that, he compliments Jain for remarkable individual stock discoveries, such as Info Edge and Motherson Sumi, which were multi-baggers well ahead of the market. That list is long, except that selling at the “right” price has cost him dearly. Info Edge for instance has zoomed past Rs. 5,000 after he sold it around Rs. 1,500 in 2018.

Jain could hold on to his conviction because he had a strong history of outperformance behind him. That played hugely in his favour with both his trustees and investors placing great degree of faith in his persistence. That trust also stems from the manager dining on his own cooking. Jain’s own money is invested in his fund schemes. “That kind of integrity and commitment is not something too many fund managers can claim. You can’t ask for greater assurance than that,” says Gumastha.

The fund manager quoted earlier, who does not want to be named, says the one thing he would do differently from Jain is position sizing: “As mutual fund managers, our primary mandate is to beat the benchmark. If that objective is clear, the portfolio has to be managed accordingly and so I would be wary of moving completely away from the benchmark.”

Till the last decade, Indian fund managers hardly paid heed to benchmark return. The size of mutual funds was small and beating the benchmark was a cakewalk. The real objective for managers was to stay in the top quartile and produce absolute return. The game has since changed.

As the fund industry grew in size, the level of outperformance came down. It was a wake-up call for fund managers. After all, the mandate of an active mutual fund is primarily to beat the benchmark, beat peers and seek absolute return, in that order.

The fund manager quoted above says their fund house has set a maximum variation of 30% from the benchmark, be it in sector or in stocks. “In extreme situations, we could go up to 50%, but never more.” That sounds prudent from a mutual fund manager’s perspective.

But Value Research’s Kumar adds a different dimension. As the fund grows larger in size, smaller wins do not add tangibly to return. “Thus, the only way to create alpha is to take sharply contrarian calls on key bets and get them right too,” says Kumar.

Resisting style drift

Jain denies he is a contrarian investor, defending that he thinks and invests in a consistent way, but it is the market that deviates from fundamentals. While that explanation is both true and fair, he has clearly shown he is not loath to rejecting popular opinion and holding his own even under adverse circumstances. He is happy not to participate in a Keynesian beauty contest.

This is the fundamental lesson a whole generation of value investors have learnt and lived by. Benjamin Graham used the metaphor of Mr. Market, the fickle-minded character who comes and tempts you to buy and sell every day. It is for you, the investor, to take the deal or leave it. Your ability to not give in to those temptations and hold your own based on your data and research ultimately determine your investment success. It is a tenet that has been drilled into value investors – buy stocks that are available cheap and sell those that are expensive.

But few investors have been able to hold their own against market sentiment. In a recent media interview, Jain said he cared more for investment principles than for investment performance.

“When you run an open-ended fund where the NAV is published every day, you do not have an option. The investors’ pressure won’t allow you to hold on to your principles,” says Raamdeo Agrawal, co-founder, Motilal Oswal Financial Services, and an ardent follower of Warren Buffett. While most professional managers call themselves value investors, style drift is quite the norm.

Another astute fund manager raises a more pertinent question, about maintaining consistency in performance in the medium term. While investors in mutual funds are usually told to hold a three- to five-year horizon, even that may prove too short sometimes. “Sticking to principles then might be fraught with risk because you might end up with years of underperformance and then compensating with blockbuster performance. That lumpiness may not be a good idea for mutual funds as the time horizon for investors may not be in sync with that of the fund manager’s style,” he says.

That is the tyranny of managing public money. Contrarian calls can take a long time to pay off. That markets can remain irrational longer than a fund manager can hold on to his job is not a funny quote but reality.

To be fair, it is not about the irrationality of the markets alone. Jain’s investments in Canara Bank, Oriental Bank and PNB, which he sold off eventually in 2019, are debatable as these banks though they offered value may face a slow death because of their inability to survive competition. Some value investors argue that these are value traps.

Besides, Jain may have erred in judging the depth of the bad loan issue and delays in the resolution process or even the government’s mishandling of the divestment process. It could well be an outcome of inattention blindness – a concept beautifully explained by Christopher Chabris and Daniel Simons in their book The Invisible Gorilla. In their experiment, six people – three in white shirts and three in black shirts – simultaneously pass a basketball around and you are supposed to keep a count of the number of passes made by the people in white shirts. At some point, a gorilla strolls into the middle of the action, thumps its chest, and then leaves. How could you miss a gorilla on the screen? But yes, half the people miss the gorilla, the experiment revealed.

When your attention is devoted to something, you tend to ignore things that may be obvious. In Jain’s case, it may be his extreme focus on not overpaying for an asset and seeking value that may have caused him to ignore some of the other factors influencing prices.

That still does not justify the extent to which market prices were divorced from the asset value in those stocks. Similarly, the excesses in the quality basket are just about getting recognised and some of these stocks have been underperformers for the past year or so.

The narrative has begun to change slowing for the consumer pack. Over the past few years, growth in profit has come not as much from topline growth as much from pricing and efficiency gains. “Profit growth can diverge from topline growth for a few years but not forever,” says Jain. It is thus highly possible that consumer stocks go through a long period of correction that will bring their valuation down to a more justifiable level.

Then again, in the absence of any sudden and big change in performance variables, stocks may not come crashing down, which may then allow time for other managers to adjust their portfolios, without paying a huge price for clinging on to highly priced stocks. In other words, no negative marks for holding on to stocks at inflated prices.

Peering into the future

The question therefore is whether maintaining valuation discipline is a rewarding strategy. Of course, it is hard to answer because we could debate on what is the fair value of a company. But assuming that, for well established businesses with a linear growth trajectory we can agree on a fair value range, the periods of irrational behaviour, in which the market price deviates from fair value range, may far exceed periods in which the stock is priced within an acceptable range of fair value. That’s the reason why Buffett has professed holding stocks for a longer period if you bought into the right business at the right price.

“These questions are highly relevant, but no one in the world has answers,” says Chokhani. An even bigger question for all asset managers and especially Jain who has demonstrated a contrarian streak is how they will deal with this asset class in the times to come. Jain’s aggressive equity call last year has rewarded him with a remarkable comeback. Only four months ago, Balanced Advantage Fund had equities exposure of 85%. With that opportunistic move having paid off, Jain has already cut his equities exposure to 71% in the fund.

Right now, the narrative has turned positive for economy-oriented stocks driven by the expectation of earnings momentum keeping pace. The surge in stocks prices in these sectors is also supported by a market desperate for new narratives as valuation is already steep across different pockets. It is not hard to see why SBI is now being pitched as a ‘better bet’ than richly valued private banks, which may be prone to defaults in retail or SME portfolios. But then, the remaining tiny boats of undervaluation have also been lifted by the tide of liquidity. “Public sector companies are getting valued like they are going to get sold tomorrow,” says Chokhani.

Largely, equity prices are trading beyond fair value. The prices are justifiable because of low interest rates, but the risk of rising rates very much exists. “We all grew up thinking of valuation as the reciprocal of the risk-free rate. Interest rates were the force of gravity in the market but over the last 12 years, there has been total manipulation with quantitative easing,” says Chokhani.

With the Federal Reserve having rigged the market with excess liquidity, the investing landscape today has changed beyond recognition. Chokhani says that everyone is operating like Alice in Wonderland, getting a shot at showing return, turn-by-turn. “Anyone can put up a track record and show how well they are doing, because there is rotation in the market from mid-cap to large-cap, quality to value, those chasing momentum and so on.” He recalls former Citigroup CEO Chuck Prince’s now infamous July 2007 quote, “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you have got to get up and dance. We are still dancing.”

“It will end poorly though,” warns Chokhani. Either there has to be a crash or a long and painful period of correction with no return, like in the case of Japan, because equity market return has gotten front-ended. “Today cash is the most hated, but cash will be invaluable when the cycle breaks,” reminds Chokhani. As Buffett says, we do not have to participate in the market at all times but the hubris of market newbies is astounding, which explains why despite his 55-year legendary track record, many still question Buffett’s strategy.

John Maynard Keynes eloquently said years ago, “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.” The next big contrarian call that can make tonnes of money for investors may well be reducing exposure to equities at the right time or going aggressively underweight. It would be interesting to see how Jain navigates that market turn.