Imagine, having hurt your leg and needing immediate medical care, your best option is a government hospital a few kilometres away. You begin to dread the hours-long wait for a doctor’s attention, which then may just be for a few minutes. Chances are several others with conditions worse than yours have already been waiting for longer. So, as you thank your stars for giving you private hospitals, you may as well thank Dr Prathap Reddy, founder of India’s first corporate or private hospital.

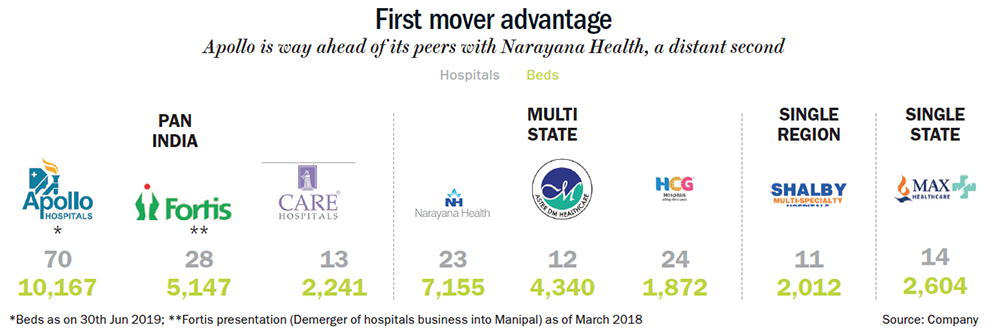

After losing a patient who could not afford to go overseas for a bypass surgery in the ’70s, he realised the need for a multi-specialty hospital. That’s what led Reddy to found Apollo Hospitals in Chennai in 1983. Since then, it has grown to become the largest private healthcare service provider in the country, with nearly 10,167 beds across 70 hospitals (See: First mover advantage). It also operates India’s largest retail pharmacy chain apart from a network of primary clinics and a health insurance company. The nearest competitor, Narayana Health, operates across 23 healthcare facilities and approximately 7,100 beds.

After losing a patient who could not afford to go overseas for a bypass surgery in the ’70s, he realised the need for a multi-specialty hospital. That’s what led Reddy to found Apollo Hospitals in Chennai in 1983. Since then, it has grown to become the largest private healthcare service provider in the country, with nearly 10,167 beds across 70 hospitals (See: First mover advantage). It also operates India’s largest retail pharmacy chain apart from a network of primary clinics and a health insurance company. The nearest competitor, Narayana Health, operates across 23 healthcare facilities and approximately 7,100 beds.

Naturally, Apollo’s stock has been on an upward trend over the past decade. From Rs.470 in March 2011, it has risen to Rs.1,680 in February 2020. After seeing some weakness in 2018, when it fell to Rs.920, the stock has rebounded on the back of improving operational performance. “Apollo Hospitals is coming off an aggressive capex cycle and is now poised for growth and improved profitability. Given their strength in execution and clinical expertise, we expect further improvements at hospitals added in recent years,” says Harith Ahamed, analyst, Spark Capital.

Time to reap

Time to reap

3 February 2026

Get the latest issue of Outlook Business

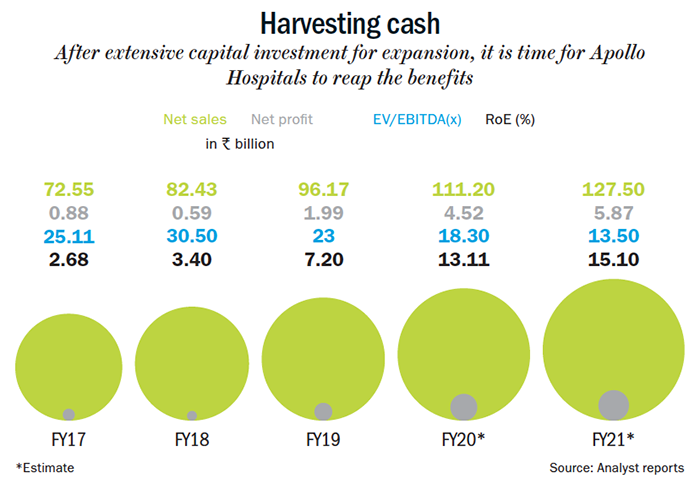

Thanks to a large unmet need and demand-supply gap, despite being a capital-intensive business, Indian hospitals such as Apollo have seen steady and predictable revenue growth (See: Harvesting cash). Over the past five years, its core business grew at 12% CAGR while making an investment of over Rs.20 billion in 13 new hospitals, adding nearly 30% to its existing capacity. Now that the investment phase is over, occupancy levels of the newly added hospitals are expected to improve. “We are expecting gains from operating leverage to play out over the next three to four years,” says Ankit Hatalkar, research analyst-institutional equities, Edelweiss Securities. He adds that once its operating margin and return ratios improve, it will be one of the better performing stocks in the Indian healthcare sector.

What works in Apollo Hospitals’ favour is that almost 69% of its Ebitda comes from mature hospitals that are more than 10 years old. They also contribute to nearly 62% of its operational capacity. For these hospitals, the cost of investment has been fully recovered and it enjoys operating margin of 22.1% compared with 8.4% for hospitals that are below five years old. “The case mix in mature hospitals is improving and the volume growth in mature hospitals is also strong,” adds Hatalkar. Even when it comes to the new hospitals, almost all have turned profitable. They rake in annual revenue of Rs.11.50 billion and they have the capacity to generate revenue of 1-1.25x the capital employed over the next five to seven years. The group’s largest hospital in Vashi, opened in November 2016, with an operational bed facility of 230 is already Ebitda-positive with 50% occupancy. The company’s Nashik hospital is the only one making losses at the Ebitda level, according to the management.

Spark Capital’s Ahamed is confident about Apollo’s prospects: “They are so good at tweaking the specialty and doctor mix that you will never see an asset that is loss-making for a long period. While some may take time ramping up, they figure out how to make it work in three to four years.” Param Desai, vice president, Elara Capital, adds: “Over the next three to four years, we expect the overall Ebitda margin to improve from around 8% to around 14-15% and that will bring in an additional Rs.2 billion in Ebitda.”

According to the company, the focus will be on improving asset utilisation by increasing overall occupancy levels, which is currently at 68% of operating beds. Over the next three years, it is expected to go up to 71%. That may not be too difficult to achieve since more than one-third of its revenue comes from daycare and very low average length of stay (ALOS). In fact, over the past 10 years, ALOS has steadily declined from 5.15 days to 3.99 days while the average revenue per occupied bed increased from Rs.15,134 to Rs.36,946. This essentially means the company is utilising its assets well.

Another advantage for the chain is that while patients typically choose hospitals for treatment based on a specific doctor or specialist, Apollo Hospitals’ revenue is not doctor-driven. “Patients come here for the brand, and not for a doctor. That’s why Apollo has the lowest doctor dependency,” says Hatalkar. According to the Edelweiss Securities report, Apollo has 70% of its doctors on payroll and 30% of visiting specialists, whereas other players have 40-50% of the latter.

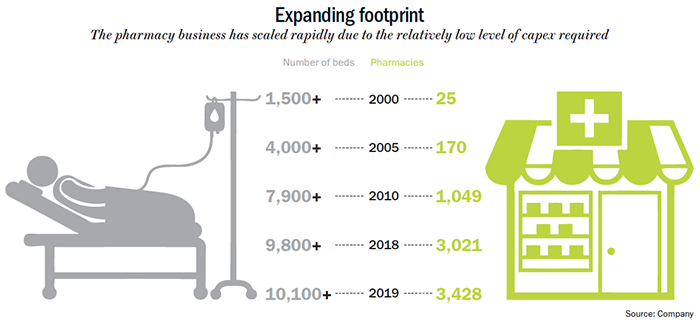

Apart from its core hospitals business, which brings in nearly 54% of consolidated revenue, the company has invested significantly in non-tertiary care businesses — retail pharmacy, which contributes 40%, and Apollo Healthcare and Lifestyle, which includes primary clinics, diagnostic centres and diabetic clinics, and contributes 6% to the overall revenue. Its pharmacy business is the largest in the country with over 3,700 outlets (currently) across 20 states and has seen revenue growth of 17% over the past five years (See: Expanding footprint). Analysts believe that increasing contribution of its private label, which is currently at 8% of pharmacy sales will help in improving the overall margin of the business.

Apart from its core hospitals business, which brings in nearly 54% of consolidated revenue, the company has invested significantly in non-tertiary care businesses — retail pharmacy, which contributes 40%, and Apollo Healthcare and Lifestyle, which includes primary clinics, diagnostic centres and diabetic clinics, and contributes 6% to the overall revenue. Its pharmacy business is the largest in the country with over 3,700 outlets (currently) across 20 states and has seen revenue growth of 17% over the past five years (See: Expanding footprint). Analysts believe that increasing contribution of its private label, which is currently at 8% of pharmacy sales will help in improving the overall margin of the business.

The company has also invested about Rs.6 billion in building retail healthcare business through Apollo Healthcare and Lifestyle. This segment includes Apollo Spectra Hospitals for minimally invasive surgeries and multispecialty clinics, diagnostic centres and Apollo Cradle, a centre for women and children. This vertical just broke even at the operating level in September 2019. “In FY19, it clocked a loss of Rs.1 billion at the operating level. It has the potential to generate nearly Rs.1 billion in Ebitda over the next three to four years leading to better overall margins for the company,” says Desai of Elara Capital.

Debt set right

While the group has scale and skill on its side, there have been concerns on pledging of promoter shares and rising debt on the company’s books. Over the past five years, the company’s net debt increased from Rs.8.55 billion in FY14 to Rs.31.80 billion as on January 2020. The company expects this to reduce to Rs.25 billion after the pharmacy restructuring and the Apollo Munich stake sale by the end of FY20. This rejig will ensure its net debt to equity ratio stays at about 0.84x. While this figure is slightly higher than its peer Narayana Health’s debt ratio of 0.68x, it is considerably less than Healthcare Global’s 1.5x.

Apollo Hospitals will rake in about Rs.3.9 billion from the restructuring of its pharmacy business. In November, Apollo had announced restructuring and stake sale of its pharmacy operations under Apollo Pharmacies to Enam Securities, Jhelum Investment Fund and Hemendra Kothari for Rs.5.28 billion. Under the new structure, Apollo Pharmacies will be carved out into a separate company, which will be a wholly owned subsidiary of Apollo Medicals. Apollo Hospitals will own 25.5% of Apollo Medicals and the balance will be held by the new investors. According to Hatalkar, around 85% of the economic value of the business will continue to remain with Apollo Hospitals. Another infusion of cash will come from its stake sale in Apollo Munich Health Insurance, which HDFC agreed to acquire in June 2019. While the Reddy family holds 40%, Apollo Hospitals holds about 9.96%. HDFC will be buying out 51.2% stake in this arm for around Rs.3 billion.

The other big concern will also be addressed by the stake sale as the promoters will redeem some of their pledged shares. At one point, the company spooked investors when promoter pledging rose as high as 78% for Rs.17.5 billion including accrued interest. The management assured that this was done to invest in Apollo Hospitals, Apollo Munich and medical education between 2008 and 2012. Later, promoters took an additional pledge on their shares to meet their repayment commitment to KKR since the PE major had invested Rs.5.5 billion through non-convertible debentures in Apollo’s parent company, PCR Investments, in October 2013. To allay investor concerns, the promoters sold 3.6% stake raking in Rs.7.5 billion, bringing the promoter holding to 30.8% at the end of the September 2019 quarter. After the stake sale, Apollo has been able to use the funds to reduce promoter pledging to 29.64%. While the promoters have ruled out any further dilution in the company, they expect the level of shares pledged to come down to 25% by April 2020.

In good health

Analysts are optimistic about the concerns being addressed and the brand sustaining its competitive edge. As operating parameters for key hospital clusters start to look better, many deem Apollo as the best bet on the Indian healthcare sector. Analysts at Citigroup expect the Ebitda margin to improve by 230 basis points to 13.4% over FY19-22 leading to a significant improvement on return on capital employed from 9.1% to 18%. Any further growth in the operating metrics in Apollo Health and Lifestyle and their cancer treatment facility, Proton, will only further improve RoCE.

Since it is a capital-intensive business, stock market valuation tends to mirror the company’s return on capital rather than earnings growth. Apollo currently trades at 13.5x its FY21 EV/Ebitda whereas Narayana and Healthcare Global trade at 12.5x and 10.5x, respectively. Given its improving fundamentals and the fact that the stake sales will reduce the debt burn and promoter pledging — two of the major concerns with investors last year — almost every analyst covering the healthcare space is bullish on Apollo Hospitals. Some believe it has enough head room with Citigroup analysts forecasting a price target of Rs.1,970.