For most of his early career Karan Virwani had watched his father, Jitendra Virwani, chairman of Embassy Group, build gleaming office parks for multinational corporations, becoming one of India’s largest commercial landlords. Their tenants ranged from Tata Consultancy Services and Goldman Sachs to Rolls-Royce. In 2016, when Karan was 24, he spotted a new trend in the real estate space.

A new wave of start-ups was rewriting what Indian business looked like. Many of these start-ups had humble beginnings in a co-founder’s apartment. Flipkart was built out of a Bengaluru apartment, Freshworks launched from a cramped warehouse-garage in Chennai and RedBus started from a residential flat.

“For small- and mid-sized businesses, no Grade A landlord was leasing space. You couldn’t go and sign for 2,000 or even 5,000sq ft with developers like DLF or Embassy,” says Karan Virwani, WeWork India’s managing director and chief executive (CEO).

4 July 2026

Get the latest issue of Outlook Business

He had a plan to fill this gap with flexible workspaces, commonly called co-working spaces. These are fully furnished offices where start-ups and freelancers could rent a desk or a room by the month instead of signing a long lease.

He pitched the idea to his father. Around the same time, Jitendra received a call from Tuhin Parikh of Blackstone India, his partner in the business-park segment, flagging the same opportunity.

A month later, the Virwanis were in New York. They visited WeWork and met its co-founder, Adam Neumann, at the time the closest thing the global start-up world had to a rock star. WeWork Inc was barely six years old but already valued at $16bn.

The meeting itself was anything but conventional. “He was having a boxing session... with a punching bag inside a frosted glass cabin. You could just hear him punching,” recalls Virwani. For someone coming from a traditional business environment, it felt “super cool”.

Behind the theatrics, however, was a hard negotiator. The firm was rapidly expanding across London, Tel Aviv and Shanghai. However, “India wasn’t a priority”. It took multiple rounds of discussions to arrive at a model that would work for India.

Eventually, a deal was struck: Embassy Group’s new company would exclusively license the WeWork brand in India for 99 years, invest the capital and build the business from zero to 90,000 seats within five years. After that, WeWork Global was to buy them out, with Embassy remaining “just a real estate partner”.

While the plan and ambition behind the formation of WeWork India in 2017 were clear, what followed was anything but. For its first five to six years, WeWork India would be in permanent crisis management, battling a credit freeze, a collapsing parent and a pandemic that emptied every office it had built.

One Trial After Another

WeWork Galaxy, WeWork India’s first centre, opened in Bengaluru in June 2017. Within 18 months, the lending market froze after an initial default by IL&FS, one of India’s largest infrastructure-financing companies, to the tune of ₹450cr. This led to a cascade of collapses across Reliance Home Finance, Reliance Commercial Finance and Dewan Housing Finance Corporation.

“By November 2018, when we needed a lot of capital, the NBFC [non-banking financial company] crisis hit India and all lending stopped. We weren’t able to raise money or find funding. We were too young for private equity, and no one was willing to back us at that point,” recalls Virwani.

Embassy had no choice but to reach into its own balance sheet. It deployed ₹1,000cr of promoter equity, followed by another ₹200cr from ICICI Bank after pledging part of its stake in WeWork. It was improvised survival. But it paid off in the long run by building a culture of treating capital as scarce and keeping costs in sync with the top line.

The situation worsened when the US-based WeWork Inc’s listing attempt, less than a year later, “turned into a complete meltdown”. What followed was months of bad press not just for the US entity but also for the franchises/subsidiaries globally.

WeWork India, though a pure franchise with no equity held by the American parent, found itself answering questions about problems it had no role in. The financial firewall was real: Embassy held all the equity, the India books were independent, and the 99-year licence deal meant WeWork Inc had no claim on Indian operations.

“We were lucky we were not funded by them. At that time, they didn’t own any equity in the India business. It was just a pure franchise business,” Virwani says. To insulate the brand entirely, WeWork India distanced itself publicly and repeatedly.

He claims the controversy didn’t impact sales. “We were seeing peak sales happen when all the PR was happening,” he says.

Then, barely six months later, Covid threatened to pull the young start-up under for good. “By then, we had already been through two major external shocks [including the NBFC crisis] that had nothing to do with us, but deeply impacted how we ran the business. We had already gone through layoffs and multiple challenges,” Virwani says.

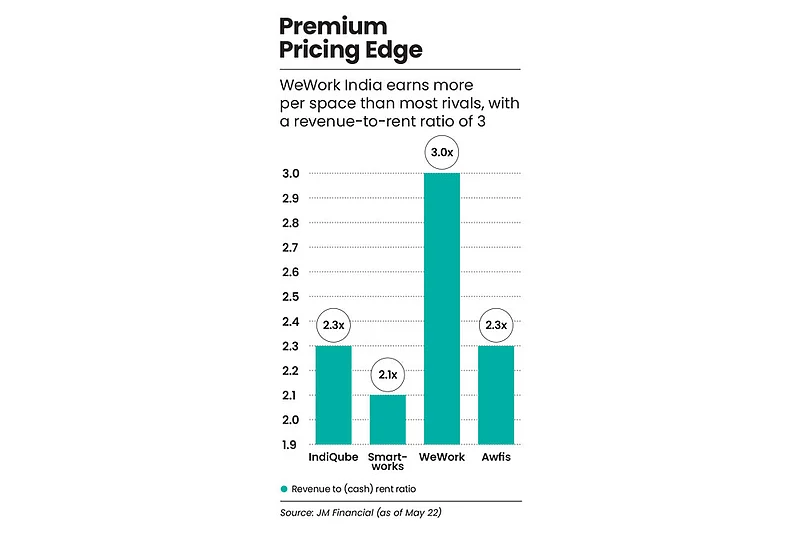

For every rupee WeWork pays a landlord, it earns ₹3 from clients, the highest revenue-to-rent multiple in the sector

As the pandemic emptied offices, he, like many others, initially believed the disruption would be short-lived. Then companies like TCS and others started saying work from home could become permanent. “That was worrying for us because we had so many spaces and long-term leases. Suddenly, buildings that were once full of people became ghost towns,” he says.

As the situation persisted, the company had to renegotiate rents with landlords, seek short-term relief through deferred payments and exit certain locations. “We were investing in capex and members were continuing to sign up, so there was no way to stop. We just had to keep pushing the problem forward until we found a solution,” he says.

Relief came from an unexpected direction. WeWork Inc, now under new management appointed by SoftBank and led by CEO Sandeep Mathrani, invested $100mn in the Indian entity in 2021, acquiring a 27% stake. Embassy retained 73%. The capital came at the right moment, helping WeWork India navigate outstanding vendor liabilities and stabilise operations through the pandemic’s second wave.

At the time, the company had just over 60,000 desks in 34 centres across six cities. In the next three years, it nearly doubled its presence in terms of seats and centres to over 1.1 lakh and 63 locations, expanding into more cities. The crises had forced a discipline that expansion, when it finally came, could build on.

“When Covid hit, we weren’t necessarily calm, but we were more prepared. We had become quite resilient by then,” Virwani says.

However, by 2024, the crises had permanently redrawn the ownership map. Embassy, having deployed over ₹1,000cr into the business, remained the majority owner.

By 2025, the group needed that capital back for other verticals, and tried raising investment from outside, but the valuations they were getting were too low.

A glimmer of hope appeared in 2024 with the successful initial public offering (IPO) of rival Awfis Space Solutions. WeWork India filed IPO documents in early 2025, but it remained under market regulator Securities and Exchange Board of India review for five months.

Even after approval in mid-July, there were complaints that the documents didn’t fully disclose criminal proceedings against the Virwanis. These proceedings were eventually quashed. Ultimately, the IPO was pushed through. But retail investors subscribed to just 61% of their reserved portion while institutional buyers were oversubscribed 1.79 times.

On listing day, October 10, the company’s stock dipped 5% below the issue price of ₹648 intraday, before closing at ₹632.

Beyond Survival

Seven months on, the IPO has given WeWork India a public identity separate from its licenser, its promoter and its past. The survival chapter was formally closed and focus could shift to growth and profitability.

Over the past several months, brokerages that started covering WeWork India shares, such as ICICI Securities, Jefferies and JM Financial, have all issued buy calls. Jefferies even called it a “category-defining leader” in November 2025, projecting 22% revenue compound annual growth rate (CAGR) through 2027–28. JM Financial called it their “top pick in the space”.

The company has both strengths and weaknesses, and is faced with both opportunities and challenges.

Its key strength lies in its high revenue-per-seat. Kulmani Rana, founder and CEO of New Delhi-based venture platform Fibonacci X, who used WeWork for two years around 2022–23, illustrates the pricing premium: in one of Gurgaon’s key commercial hubs, Golf Course Road, a standard seat runs at ₹12,000–14,000. However, at WeWork’s One Horizon, the same desk costs ₹35,000, including GST.

“The experience was flawless–from community engagement to the quality of fittings. That’s why they command a 60–70% premium over a standard seat,” he says.

He points out that building owners in markets like Gurgaon typically earn a modest 4% rental yield, leasing bare-shell space at ₹100–140 per sq ft. WeWork, sitting between landlord and client, could charge around ₹250 per sq ft in the same markets, with annual escalations built in.

While rivals like Smartworks and IndiQube focus primarily on cost efficiency and enterprise solutions, WeWork stands apart through a brand-led portfolio. It offers on-demand desks, virtual offices, conference rooms, parking, information technology (IT), food and beverages, and now design services. It has built a broader platform with workplace-as-a-service, business solutions and community offerings—events, start-up programmes and more.

As a result, for every rupee WeWork India pays a landlord, it earns ₹3.0 from clients, the highest revenue-to-rent multiple in the sector. Rivals IndiQube and Smartworks manage 2.3x and 2.1x, respectively, against a sector average of 1.9x.

The company has a much larger client base, at over 2,000, compared to IndiQube’s 830 and Smartworks’ 777. Moreover, 45–50% of desks sold, excluding renewals, are from clients upgrading within the system, according to JM Financial.

The Structural Shift

However, the company’s business model is also coming under increasing pressure from an evolving market.

Flex workspaces, which began as a fringe option for start-ups and freelancers, have now become a mainstream way for companies to operate as the demand driving it has changed fundamentally.

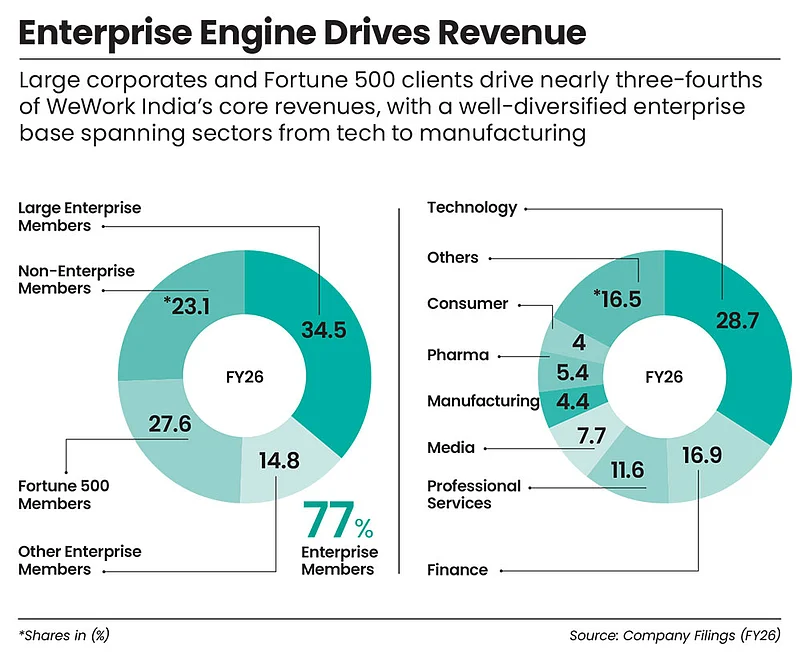

Large enterprises—multinationals, global capability centres (GCCs) and Fortune 500 companies—want customised, long-term office setups, not pre-designed shared spaces.

As of 2025, managed and enterprise solutions account for 70–80% of total flex demand, as per property consultant Anarock.

This is where WeWork India faces its sharpest structural challenge. Smartworks and IndiQube have 100% of their portfolios in managed office space, giving them client lock-in periods of 47 and 33 months, respectively, and roughly 65% of clients renting more than 300 seats.

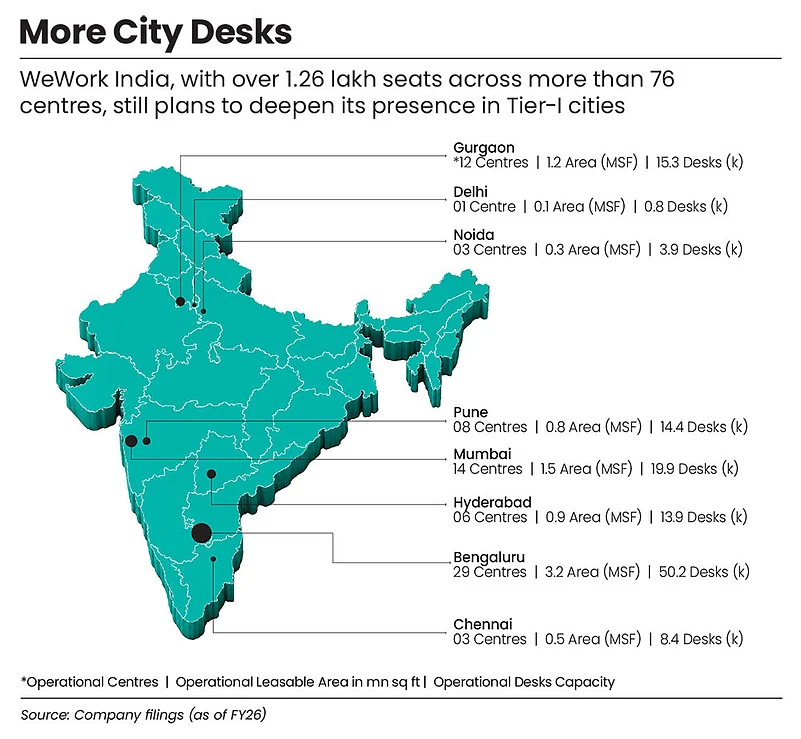

WeWork India has only recently entered this segment. Managed offices currently account for just 21% of its portfolio, translating into a 26-month average lock-in. Demand is being driven by large enterprises, with global capability centres, or captive back offices of global enterprises, accounting for over 50% of all flex seats, followed by IT-services firms at 25%. This is also reflected in the scale of each of these companies. WeWork offers only 1.26 lakh desks across 76 centres, while Smartworks has 2.31 lakh desks across 66 centres and IndiQube has 2.15 lakh across 130.

Rivals, with their large, longer-term clients, spend less on client acquisition and also enjoy better visibility on revenue and profit. WeWork’s earnings before interest, tax, depreciation and amortisation (Ebitda) margin is expected to rise to 26% this year, according to JM Financial, but still trails Smartworks’ 30% and IndiQube’s 28%.

Hence, the company that commands the highest revenue-to-rent multiple in the sector is not yet the most profitable. “Since managed and enterprise solutions account for 70–80% of total flex demand, scaling this segment is critical to the future relevance of any operator,” says Peush Jain, managing director of commercial leasing and advisory at Anarock.

WeWork India has a larger client base, at over 2,000, compared to IndiQube’s 830 and Smartworks’ 777

Secondly, there is uncertainty about IT, which accounts for 40% of the total flex office demand in India, stemming from geopolitics and artificial intelligence (AI).

However, Virwani is not unduly worried and points out that most of his clients are technology firms, rather than IT-services majors. “They are largely end-tech, global tech and cyber security [firms],” he says, noting that IT services does not even figure in WeWork India’s client mix, with 34% of revenue from the broader tech sector, comparable to Smartworks but structurally different from pure IT and IT-services exposure.

Brokerage Kotak Securities’ Shrikant Chouhan projects a 25% Ebitda CAGR between 2025–26 and 2027–28, citing premium positioning and relatively low IT client exposure as the key differentiators.

On the question of broader demand, he points to India’s commercial real estate gap. “India has 800mn sq ft of Grade A real estate; Manhattan has 750mn. That’s how small our commercial market is compared to that of the world,” he says.

Moreover, the rupee’s continued depreciation, he adds, makes India increasingly attractive for global companies to operate from.

The Next Growth Lever

On the margin question, Virwani’s strategy is to build the full spectrum of workspace-as-a-service offerings, capturing clients at every stage of their growth.

To that end, the company launched Rivet, an end-to-end design-and-build platform for large enterprises and GCCs looking to set up offices in India. Unlike traditional managed office models, Rivet offers a single contract covering design, engineering, construction and commissioning of the client’s own workspace, with WeWork India holding full accountability for delivery.

Rivet has already completed projects exceeding 1 lakh sq ft, including the Embassy Group headquarters, with a cumulative project value of nearly ₹50cr.

“It allows us to continue serving members who have grown with us and may now seek their own independent spaces,” Virwani says.

He points out that only 35% of Fortune 500 companies currently have global capability cenres (GCCs) in India.

As mid-sized global firms follow the early movers, he wants WeWork to be the default landing pad. “As this number rises, it will drive commercial real estate demand for years to come,” he says.

WeWork India’s targets reflect that ambition: to add 20,000–25,000 new seats every year, achieve 20% revenue growth and take the share of the managed office business from 21% to 30%.

JM Financial is more bullish, projecting a 24% revenue CAGR through 2027–28 and calls 2025–26 a potential industry-wide turnaround year, the point at which all three listed flex operators move into sustained net profit.

As its rivals move into structurally stronger territory on profitability, Virwani’s job may only get harder. In many ways, WeWork India has already achieved the improbable part of surviving through crises. And that’s what makes it interesting.

But as they say, the best companies are the boring ones that spit out bigger mounds of cash every quarter. The challenge ahead is less cinematic, but remains the ultimate test of a durable business.