Last year, BVR Subrahmanyam, a career bureaucrat then at the helm of NITI Aayog, a government think tank, excitedly announced at a press conference that India had become the world’s fourth-largest economy. At around $4trn in size, the milestone sounded reasonable enough, coming on the heels of India overtaking its former imperial master, the United Kingdom, and now closing in on Japan.

The claim, made amid an uncertain geopolitical climate, tried to capture a moment of confidence about India’s rise in the global order.

A year later, that confidence has turned out to be a premature celebration, with India slipping back to sixth place in the global GDP rankings, according to the latest estimates by the International Monetary Fund (IMF). The reversal was shaped by revisions to basically how India measures its GDP and the weakening of the Indian rupee against the dollar.

4 July 2026

Get the latest issue of Outlook Business

At a time when India boasts of being the world’s fastest-growing major economy, its currency has abandoned the celebration for the world to see.

Down a Slippery Slope

Over the past two years, the rupee has slipped into a spiral where almost every passing month has brought headlines of fresh record lows. It has depreciated by more than 13%, emerging as Asia’s weakest currency against the dollar. Thresholds that once seemed impossibly distant have now been breached. The rupee has crossed 96 to a dollar on May 15, sinking to the weakest level in its history.

That same history is evidence of how the Indian currency’s loss of value against the dollar has eroded a part of India’s economic progress since opening up to the global economy in the early 1990s. In the three decades till 2023–24, India’s nominal GDP grew at a compound annual growth rate of 12.4%. In dollar terms, however, the pace moderates to 8.9%.

But why should one bother? If India has grown so much and continues to do so, what does it matter if its economy appears smaller in dollar terms?

Today, just like any middle-class Indian, India aspires to become an upper-middle-income economy and, eventually, a high-income one. For a country, those aspirations are measured on a per capita income basis, but more importantly, in dollar terms, because the dollar remains the currency through which most of global trade and finance flows.

Over the past two years, the rupee has depreciated by more than 13%, emerging as Asia’s weakest currency against the dollar

For perspective, India’s current per capita income still lies far below the World Bank’s threshold of $4,496 for entering the upper-middle-income category, and even farther from the $13,935 mark required for high-income status.

A persistently falling rupee will make that climb harder, pushing those milestones further into the distance even when the domestic economy continues to expand.

In other words, no matter how much Indian workers and businesses toil to increase their incomes in rupee terms, a falling currency will reduce their international purchasing power in an economy integrated with the global trading system dominated by the dollar.

The current government understands the implications of a falling rupee very well.

“I believe a strong currency reflects the strength of a nation and will always be good for exports, because India, at the end of the day, is a net importer of goods,” said Union commerce and industry minister Piyush Goyal at an industry event in 2022. “A strong currency supports the Indian economy.”

The question is then, if the government truly understands the costs of a weaker rupee, why has it been unable to protect it?

Reversal of Fortune

As opposed to the situation today, the summer of 2024 had arrived carrying the weight of expectations for a more stable rupee. The IMF at that time, had projected the rupee to weaken, on average, only by 0.5% per annum in the next five years, compared to the 3.3% annual depreciation experienced in the three decades up to 2023–24.

There was a reason behind that optimism. Everything then seemed to be going India’s way.

On one hand, the economy had been moving at unusual speed, while much of the world seemed to have stagnated. On the other, the ruling party had returned for a third term, not with the same sweeping authority, yet with enough strength to promise something India had rarely enjoyed in its policymaking life—continuity.

Now, one may wonder how all of this was supposed to help the rupee.

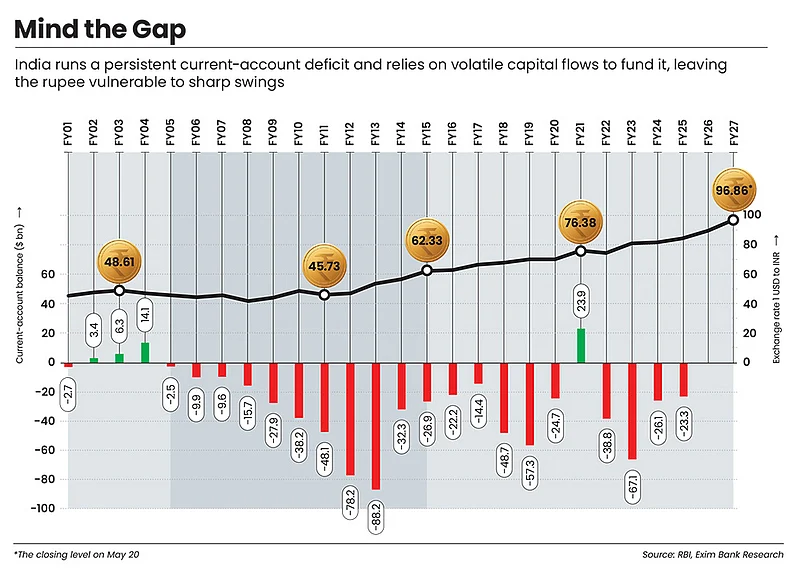

India runs a current-account deficit (CAD), which simply means it spends more foreign exchange on imports and other external payments than it earns through exports of goods and services and remittances from its far-flung diaspora. That gap has to be filled by dollars flowing in from abroad, largely through foreign investment and capital inflows. As long as investors remain confident about India’s prospects, the arrangement works smoothly and helps keep the rupee stable.

In this context, the Economic Survey for 2024–25, in fact, appreciated the IMF’s projection.

“The projected mild rupee depreciation is a recognition of India’s growth potential, its attractiveness as an investment destination and the expectation of convergence of India’s inflation rate with that of the United States,” noted the survey.

But time has a way of unsettling even the most carefully arranged expectations. That optimism was never shaped by domestic factors alone. It also drew strength from a reading of the world beyond India’s borders, and from the belief that the global order would continue to accommodate Indian interests.

Trump and Tariffs

In Washington, DC, Donald Trump was seeking a return to power, often described as a political ally of Prime Minister Narendra Modi. The public warmth between the two leaders had, over the years, acquired a symbolic value of its own, feeding expectations of a partnership that could work to India’s advantage.

At the same time, India, thanks to the encouragement from the US, was positioning itself as a leading beneficiary of the US’ growing unease with China’s dominance in global trade. There was a widespread expectation that global capital would begin to look for alternatives, and that India would be among the primary destinations. Those expectations have not come a long way.

As it turned out, the US was no longer interested in advancing Indian interests. “India should understand that we are not going to make the same mistakes with India that we made with China 20 years ago in terms of saying, we are going to let you develop all these markets, and then, the next thing we know, you are beating us in a lot of commercial things,” said Christopher Landau, US deputy secretary of state, while speaking at the Raisina Dialogue 2026.

India is only seen as a marginal player in technologies that are currently attracting global capital

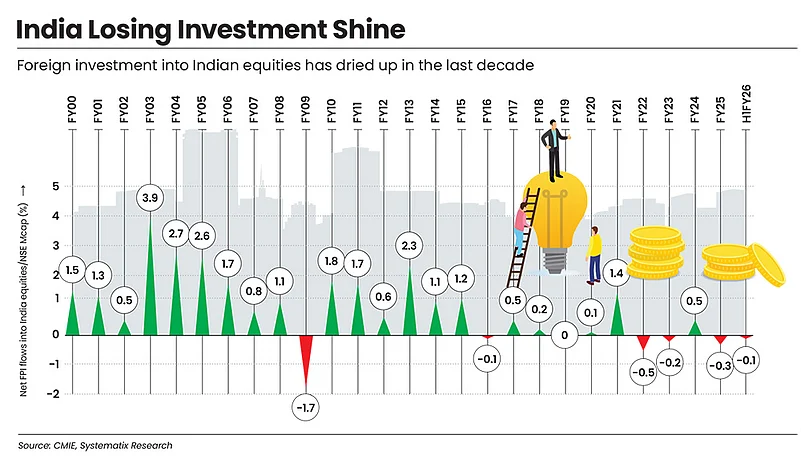

The second Trump presidency, from punishing reciprocal tariffs on Indian exporters to a series of anti-India positions at the diplomatic level, has unfolded in ways that has spooked foreign investors to an extent that instead of backing India’s economic story, they have begun betting against it by pulling out their money.

“Increasingly, exchange rates have become hostage to capital flows, their surges, sudden stops and reversals,” says Michael Patra, former deputy governor of RBI. “Capital flows are highly vulnerable to global spillovers from geopolitical events, trade policy uncertainties and overall economic policy uncertainty caused by systemically important economies.” (see pg 60)

And at a time when technology has become the defining theme of the global economy, India’s artificial intelligence (AI) narrative has done little to reverse their mood. Its focus on cost-efficient innovation and digital public infrastructure has not carried the same appeal for global investors, who remain more drawn to economies committing larger sums to more visible data centres and semiconductor ecosystems.

In turn, money has moved out into what investors now see as “innovation economies” such as the US, Taiwan and even China despite its broader economic slowdown, former RBI governor D Subbarao pointed out in a column for BasisPoint Insight, an online financial journal. Meanwhile, India may still be among the world’s fastest-growing major economies, but it is only seen as a marginal player in technologies that are currently attracting global capital.

As a result, in 2025, foreign portfolio investors pulled out nearly $19bn from Indian equities on a net basis; the largest outflow on record. What has also weighed on sentiment among portfolio investors is the gap between India’s China-plus-one narrative and actual capital inflows. Adjusted for foreign investor exits and rising overseas investments by Indian firms, economists estimate that net foreign direct investment (FDI) into India effectively hovered near zero for almost two years.

Fading Appeal

In fact, there is an uneasy familiarity to this moment, one that calls to mind Mark Twain’s observation that “history does not repeat itself, but often rhymes”.

During the global financial crisis (2008–09), the rupee came under similar pressure as foreign investors pulled money out of India and moved towards safer markets. The shift rattled an economy that had, until then, been growing rapidly and carried a similar sense of optimism about its future. A few years later, the rupee was hit again when the US signalled higher interest rates. Investors quickly began moving money back to America, where they could earn safer and better returns.

The memory of how little control India historically has had over its currency has begun to return and haunt the government of today. In response, officials have claimed innocence, trying to separate the rupee’s fall from the policies of the government.

Responding to concerns in Parliament over the currency’s decline, Nirmala Sitharaman, Union finance minister, said, “India’s economy is strong, our fiscal situation is strong, and the entire world is praising our fiscal-deficit management. Our forex [foreign exchange] reserves are solid.”

Before her, V Anantha Nageswaran, chief economic adviser argued in his longest Economic Survey this year that the rupee is “punching below its weight” and “does not accurately reflect India’s stellar economic fundamentals”. This is where experts argue that India’s pitch to global investors is beginning to look outdated.

“Foreign investors are no longer interested in your headline growth rate or fiscal deficit. They want productivity and innovation, besides external stability,” says Dhananjay Sinha, chief executive and co-head, institutional equities, Systematix Group, an investment advisory. “In that sense, the rupee’s sharp depreciation reflects India’s fading appeal as an investment destination.”

So far, India has relied on the promise of high long-term growth and domestic political stability to win the trust of foreign investors and attract the dollars needed to keep the rupee stable. That formula no longer seems sufficient in a world shaped by rapid technological shifts and geopolitical risks. In short, countries are changing their priorities, and so are investors, leaving India in a state of panic.

Lessons From History

In a recent speech, Prime Minister Modi urged people to avoid importing gold, cut down on foreign travel and reduce oil consumption, essentially asking Indians to curb anything that increases the country’s demand for dollars.

His plea highlights the uncertain times testing the Indian economy, where foreign investors are no longer willing to readily finance its CAD. On top of this, the US has triggered a conflict in West Asia.

These do not bode well for India, where rising oil prices are expected to widen the import bill and put further pressure on the rupee.

“The CAD has been very benign, averaging less than 1% of GDP over the past three years,” says Sajjid Chinoy, managing director and chief India economist at JP Morgan, an investment bank.

“Against this background [of slowing of capital flows], expectations of a much wider CAD, in the wake of the West Asia war, are acting as a force multiplier, rather than the original cause.” (see pg 79)

History rhymes here, once again.

India’s per capita income is far below the World Bank’s threshold of $4,496 for the upper-middle-income category

More than three decades ago, just like today, a war broke out in West Asia, pushing oil prices higher. But the consequences then were far more severe than they are today.

At that time, India was nowhere a serious export nation and was already teetering on the edge of a balance of payments (BoP) crisis. The country’s forex reserves had fallen so low that they could barely cover two weeks of imports.

India was, quite literally, running out of dollars.

As the import bill ballooned and remittances from Indians working in the Gulf came under stress, the crisis would become a turning point.

The situation forced then Prime Minister PV Narasimha Rao to introduce sweeping economic reforms, dismantling large parts of the licence-permit regime and opening the economy to global trade and investment.

Since then, India has tried to unlock its long-delayed export potential and strengthen the trade balance, a key component of the current account. In many ways, this is the path several East Asian economies have followed to have a stable currency.

As this year’s Economic Survey observed, “Across several successful industrialising economies, especially in East Asia, a common pattern is visible: strong growth in manufacturing exports preceded improvements in current-account positions, reserve accumulation and the gradual strengthening of currency credibility.”

This strategy offers two advantages. First, growth in manufacturing exports helps contain CAD and keeps it at sustainable levels. Second, the same export-led growth generates productivity gains that attract foreign investment, creating a win-win situation for the domestic currency.

Since the BoP crisis, India’s merchandise exports have come a long way, from $18.4bn in 1990–91 to $437.1bn in 2023–2024. This seems to suggest that India is doing pretty well in that direction.

In reality however, the idea of “manufacturing exports” that the Economic Survey pointed to has not truly been realised.

Why? Because India exports more, but also imports far more to produce those exports.

Oil-y Stranglehold

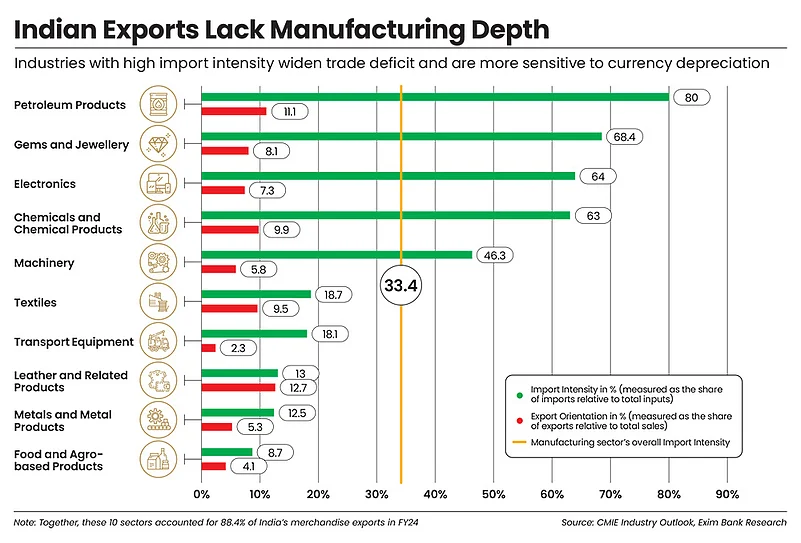

A study by the Export-Import (Exim) Bank of India, a public-sector bank to promote India’s international trade, helps lay bare how deeply imports are now woven into India’s export story. Nearly 56.2% of the country’s merchandise exports, it finds, come from sectors where dependence on imported inputs far exceeds the manufacturing average of 33.4%.

Despite years of policy pushes under programmes like Make in India and production-linked incentives, India’s merchandise exports, even when supplemented by its long-standing surplus in services trade and remittances, have failed to keep pace with the country’s import bill, leaving CAD persistently difficult to contain.

This conundrum is most visible in electronics, one of India’s most celebrated export success stories in recent years. Electronics exports have risen sharply, from $28bn in 2023–24 to $48bn in 2025–26. At first glance, it looks like the very outcome policymakers had hoped for. But the other side of the story gives the full picture.

Over the same period, electronics imports rose even faster, from $84bn to $116bn. India was exporting more phones, components and devices, but it was also importing enormous quantities of chips, parts and machinery to assemble them. The trade deficit widened instead of narrowing. That, experts argue, changes the entire equation of India’s “manufacturing exports” story.

“Many high-value sectors, such as, electronics, chemicals and machinery, today, depend heavily on imported components, technology and energy,” says Ajay Srivastava, a former Indian Trade Service officer and founder of the research outfit Global Trade Research Initiative, pointing to the low domestic value addition of Indian exports.

“And with India importing nearly 90% of its oil needs, higher crude prices widen the import bill and put further pressure on the rupee, creating a feedback loop of rising costs and currency weakness,” he adds.

After all these years, energy continues to remain India’s biggest chokepoint, with oil alone making up a significant portion of the country’s import bill. The more India spends on importing oil, the wider its trade gap becomes, a gap that is becoming harder to cover through services exports and low-value manufacturing exports.

A Different World

For years, this problem was manageable because foreign investors kept bringing money into India. Those inflows helped finance the trade gap and kept the rupee relatively stable. But now, as foreign money dries up, the same trade deficit is beginning to look far more dangerous for the currency.

And if India is unable to reverse the flow of foreign capital back in its favour, it may do well to prepare for a prolonged phase of sharp rupee depreciation. The deficit that is currently becoming difficult to finance could widen even beyond the disruptions of the present time. The problem is that India no longer enjoys the kind of global environment that once helped China build its export-led growth story, a path many believe India is trying to follow.

“The global trading environment is very different now, with geo economic fragmentation, muscular national trade and industrial policies, reshoring of supply chains and tariff and non-tariff barriers having weakened global demand and depressed global economic prospects,” says Patra.

Even if India does get past geopolitics, the global economy itself is no longer the same. Its growth, according to the UN Conference on Trade and Development, is slipping towards levels often associated with recessionary periods, raising the possibility of weaker global demand in the years ahead.

Energy remains India’s biggest chokepoint, with oil alone making up a significant portion of the import bill

Meanwhile, the rise of AI, apart from discouraging foreign inflows into India, has also triggered fears that demand for large segments of routine IT and back-office services, sectors where India built a major export advantage over decades, may weaken over time.

Yet regardless of where the world might be heading, India, unless it cuts down its dependence, is expected to import more oil.

India, according to the World Oil Outlook 2025, is projected to remain the single-largest contributor to global oil demand growth until 2050, with its demand rising by another 8.2mn barrels per day.

With all of this, pressure on the rupee could, very easily, persist as a structural feature of the economy rather than a temporary phase of market volatility. Most importantly, this structural weakness will take its own toll in such a way that eventually feeds back into itself.

Cost of a Cheap Currency

Mahavir Sharma, founder of Oscar Expo Design, a Jaipur-based producer and exporter of wooden furniture, carpets and silver jewellery, had never imagined that the rupee would fall so sharply against the dollar that he would be forced to rethink his production costs altogether. All his imports such as dyes, chemicals and wool are getting expensive, with energy inputs used in operational activities adding further to the cost.

“A sharp depreciation in the currency is not good for any economy and can make producers uncompetitive compared to businesses of other countries whose currency maybe doing relatively better,” he says. “We hope that this situation does not go on for long and gets resolved soon.”

Sharma’s worries are shared by thousands of producers across the country who depend heavily on imported raw materials to keep their factories running, yet do not always have the luxury of passing these higher costs from a weaker currency on to consumers in India’s low-income and intensely competitive market.

More importantly, as they absorb these pressures instead of expanding production or investing further, productivity growth across the economy begins to slow.

In March, for instance, the same month the rupee breached 95 for the first time, growth in India’s manufacturing sector, as captured by HSBC’s Purchasing Managers’ Index, fell to almost a four-year low.

“Firms also faced an intensification of cost pressures, the steepest since August 2022,” HSBC noted in its report. Its chief economist Pranjul Bhandari observed that “firms appear to be absorbing much of the increase, keeping output prices relatively contained”.

No wonder the prime minister and ministers of the ruling government who speak of turning India into a manufacturing hub have long argued in favour of a stronger and stable rupee, even from the time before they came to power.

A falling rupee, often hailed by many trade economists as a messiah for Indian exporters, can in reality act as a Trojan horse, weakening the economy from within through rising input costs that slow output growth and investment cycles.

And among all the inputs, the most significant channel of pressure is, once again, of energy, points Jahanwi Singh, senior economist with the Exim Bank of India. “Sectors such as aluminium, iron and steel, cement and chemicals are highly energy intensive. These sectors also have significant linkages with other manufacturing sector activities, leading to a transmission of the cost pressures across the value chain,” she says.

“Therefore, the drag on manufacturing operates more strongly through energy prices, with the exchange rate acting as an amplifier,” she adds.

Reinforcing the Loop

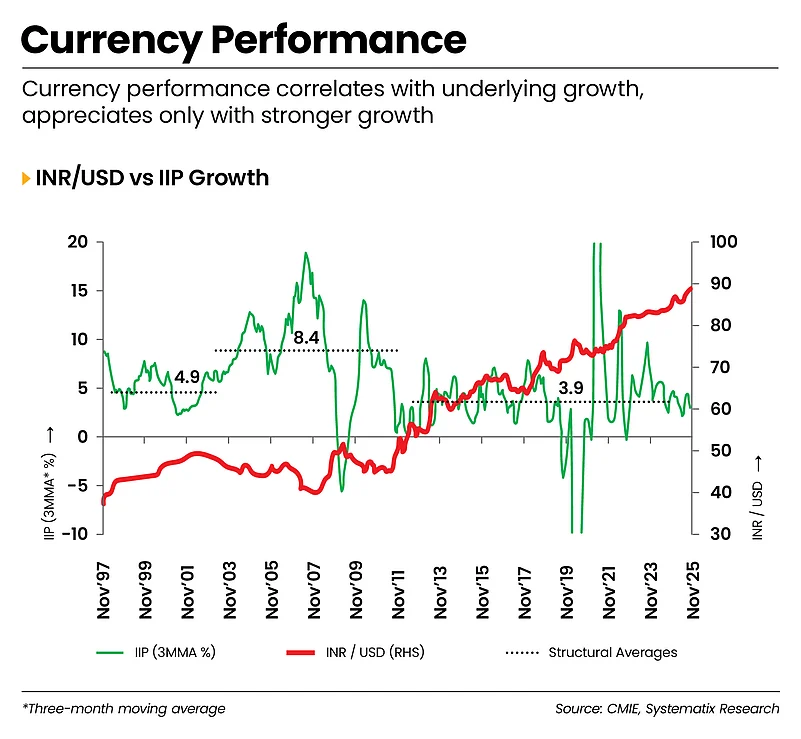

The concern is borne out by data that points to the adverse impact of a volatile and falling rupee on growth in India’s Index of Industrial Production (IIP), an indicator used to track changes in output across manufacturing, mining and electricity. Between early 2000s and around 2010, a period when the rupee remained relatively stable, growth in the IIP, where manufacturing carried the highest weight of 77%, averaged 8.4%, according to research by Systematix based on data from the Centre for Monitoring Indian Economy.

India today is caught in a vicious loop of weakening capital flows and a falling currency

In contrast, over roughly the past decade-and-a-half, the average growth rate has slowed to 3.9%, suggesting a negative correlation between the rupee’s more volatile fall and manufacturing growth, as per the research.

India has seen significant growth in merchandise exports, but this has not eased the trade deficit or strengthened the current account, as imports have grown even faster, leaving currency stability at the mercy of volatile foreign inflows.

This instability, in turn, feeds into the country’s productivity and industrial growth. But the cycle does not end there. There is a third and final phase, one that circles back to where it began.

Such slowdown in growth, experts point out, can further dampen foreign-capital inflows, reinforcing the loop. “If you have sharp currency depreciation, it ultimately slows productivity growth in an economy with high import intensity and feeds into itself,” says Systematix’s Sinha.

“As growth slows, foreign capital inflows, which are pro-cyclical rather than counter-cyclical, tend to fall, creating a self-fulfilling loop.”

In simple terms, if businesses face tighter margins and cut back on investment and expansion because of currency pressures, foreign investors also begin losing confidence and pull money out instead of bringing more in to help ease that pressure. That, in turn, puts even more pressure on the rupee, creating a cycle that keeps feeding itself.

To understand this link better, it is worth noting that while India today is caught in a vicious loop of weakening capital flows and a falling currency, it experienced the exact opposite between 2004 and 2008, where a stable rupee and strong industrial growth during that period attracted equity inflows averaging a little over 2% of GDP, helping the rupee appreciate by around 2.5-3% a year.

A key facilitator of this loop or cycle is obviously, India’s high import dependency.

So today, while the rupee is being described by the government as a “victim of geopolitics”, that may appear true on the surface.

A deeper look into the problem suggests India’s inability to reduce its import dependency that fuels its consumption-led growth. This has left the country trapped in a cycle over which policymakers may ultimately have little to no control.

If the nation truly wants to prosper, this cannot go on forever.

The Currency Curse

At independence, India carried an ambition that stretched far beyond the immediacy of nation-building, the belief that one day it would reclaim its place as a prosperous and self-assured economy.

And yet, even before that moment of freedom arrived, the rules of the global economic order that would challenge that belief had already been written elsewhere.

In 1944, at the Bretton Woods Agreement, the dollar was placed at the centre of the world’s financial system, initially anchored to gold and, even after that link was broken in 1971, retaining its dominance as the principal reserve currency.

What has emerged is not just a medium of exchange, but a god among currencies, one that continues to shape the fortunes of economies like India.

For countries whose industrial policies fall out of sync with the force of the dollar, the consequences have often been severe, eroding hard-earned gains at home and trapping the economy in a cycle of recurring currency pressure.

The only durable way out is to build stronger domestic industrial capacity that not only expands the economy but also allows the country to retain the gains of that growth.

The choice now confronting Indian policymakers is whether they want to finally break India free from this currency curse that has shadowed the country for decades, or simply live with it.