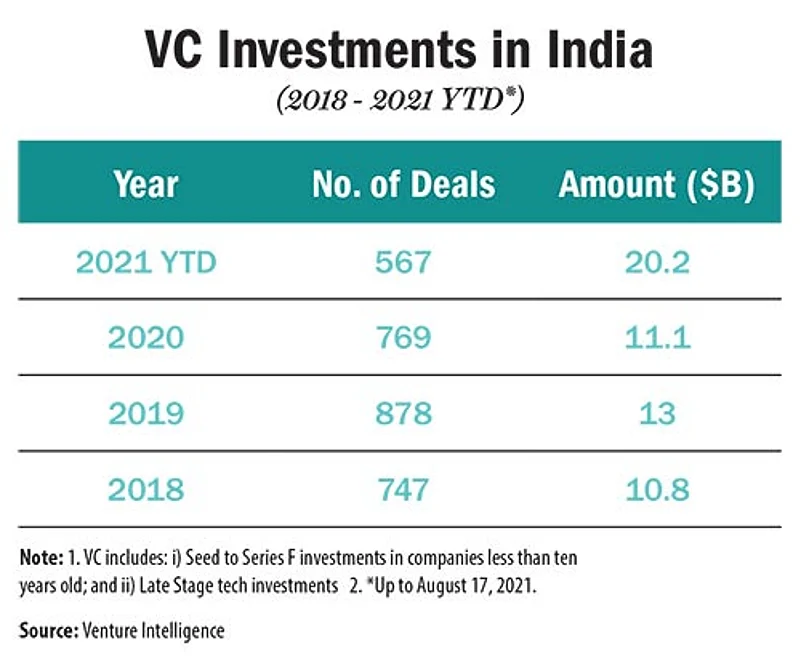

A seed funding of anything above $2 million would have made Indian entrepreneurs content until 10Club, an e-commerce marketplace aggregator, raised $40 million last June. It sowed in its peers the dreams of mopping up more from American investors who benefitted from the quantitative easing that came as a COVID-19 relief measure. As the money found its route to the Indian shores, start-ups received $15.6 billion in 2021 alone. This was a whopping 218 per cent more than what they had garnered a year ago, says Tracxn Technologies.

The cash jab has spawned hope for many Indian start-ups of the over 41,000 government-recognised ones by indicating that the days of liquidity crunch are behind. The Zomato public issue has stoked optimism further with fear of missing out or FOMO perceptible in the investor community ever since a host of start-ups have lined up for listing this year.

3 February 2026

Get the latest issue of Outlook Business

“For the first time, retail sentiment is going crazy behind these IPOs. It’s a new era that we are entering, with all the right ingredients in place. The companies are maturing and proving their economics. The retail investor pool is growing rapidly in terms of active equity investing,” says Manasi Shah, vice president at Accel.

The IPO frenzy has gripped the equity market as well. Aided by a consistently falling rate of daily COVID-19 infections, positive global cues, and impressive corporate earnings, the benchmark indices have scaled record highs. The untamed rally in equities has triggered a suspicion of a bubble that’s waiting to bust. The IPO wave is expected to separate the wheat from the chaff. “Fundamentally strong businesses will be separated from those which were just fuelling growth,” says Shah.

Reliance & Tata on shopping spree

It’s not just foreign money that’s making inroads into Indian start-ups. Corporate India, too, has joined the rally. Mukesh Ambani-led Reliance Industries has invested $3.41 billion in 21 Indian start-ups. The Tatas come second with $380 million spent on various tech start-ups with a majority stake in prominent ventures like 1mg and BigBasket, Tracxn says.

Reliance filled its shopping cart with companies that add to the infrastructure of Jio services. The Tatas, on the other hand, focused on consumer internet companies in the hope of turning around its fortunes and reducing dependence on TCS for cash flow.

“It was unfortunate that Indian corporates were least likely to adapt to technology,” says Siddarth Pai, founding partner at 3one4 Capital. “Infosys, HCL, Wipro and the likes were the breeding ground for innovation but these tech giants have hardly invested in the start-up ecosystem. It’s heartening to see that major corporates like Reliance and Tata have started looking into this actively and have become an important component,” adds Pai.

The China effect

When India banned Chinese apps like TikTok and SHAREit, and online games like Clash of Kings and PUBG, Indian entrepreneurs experienced a difficult phase for a few months. The fear of being called anti-national forced start-ups that are Decacorns, Paytm, for instance, to denounce the presence of Chinese investors on their boards. But the crisis was resolved faster than anticipated and global funds like SoftBank and Tiger Global rushed in to fill up the vacuum to increase their India play.

With China hounding its own tech giants like the Ant Group, Didi Chuxing Technology Co. and its entire edtech sector, there is a possibility for a spurt in flow of funds into India’s digital economy. “India is reaping from China’s crackdown on its tech-based start-up ecosystem. The spillover effect has come to India tremendously because India has, over time, streamlined its foreign direct investment regulations. In sectors like insurance, edtech, anything in IT/ITES, FDI is almost unrestricted and start-ups operate mostly in these sectors. So, the amount of foreign capital that is coming in has actually increased. India is also in a sweet spot right now in terms of basic infrastructure to leverage the capital,” Pai says.

Behind the euphoria

Much like the rally in equities, the exuberance in the start-up ecosystem, too, has led to the fear of a fiasco. “Money supply has increased. That’s what is playing out in the early-stage Indian start-up ecosystem where the risk is very high but return is also very high,” points out Sandeep Aggarwal, CEO and founder of Droom. “I don’t think it’s a bubble waiting to burst but I will say that the market is frothy and rich and will correct in the next one or two years,” adds Aggarwal, who is also an angel investor.

Zomato was in the red when it floated its maiden public issue. The issue was subscribed more than 38 times, valuing the company at Rs 643.65 billion. Zomato’s success has driven all eyes to Paytm which is also incurring losses. Another success story would catapult the Indian start-up ecosystem to a far higher orbit.

E-commerce giant Amazon had skid into losses a year after it went public. Founder Jeff Bezos had a two-point agenda to revive: Looking at a long-term objective to rule the market and taking bold moves without craving for profit. India’s tech IPOs are perhaps planning to toe the Amazon line. “We have a history of net losses,” says the draft red herring prospectus (DRHP) of One97 Communications which owns payments app Paytm. “We may not be able to achieve and maintain profitability,” it says.

In the last three financial years, Paytm logged net losses of Rs 42.35 billion, Rs 29.43 billion and Rs 17.04 billion. While declaring its plan to go public, One97 Communications said it aims to raise Rs 166 billion from the issue.

Most of the tech companies such as Nykaa, MobiKwik and Policybazaar, besides Zomato and Paytm, scheduled for listing this year are loss-making companies. The listing of Uber and Lyft were the most sought-after events in the US financial calendar for 2019 but both the issues suffered major failures, inexorably questioning the credibility of the American tech economy.

One such failure of an overhyped listing would be potent enough to drown the entire sector in a state of gloom, warn experts. They call it the ‘Greater Fool Theory’ where one can make money by buying overvalued assets and selling them for a profit later, because it will always be possible to find someone willing to pay a higher price.

Veteran investor Rakesh Jhunjhunwala does not believe that the euphoria around the IPOs of loss-making companies would last long. In fact, he fears that one fiasco might turn out to be lethal for others that are not even racing for the bourse.

Informal sector is another major threat for the tech IPOs. Various lobby groups, formed by stakeholders from the informal sector, are questioning the aggressive business practices followed by these start-ups. Confederation of All India Traders (CAIT) had recently geared up to take on both Amazon and Flipkart. It alleges that the e-commerce ventures have violated foreign investment policies. CAIT has also accused them of destroying livelihoods of small traders in India because of their anti-competitive policies. Federation of Hotel and Restaurant Association of India (FHRAI), too, has raised concerns over the alleged anti-competitive practices of hospitality unicorn Oyo. It says Oyo’s business model could permanently damage the larger hospitality industry in the country.

Not that bad, really

Start-ups valued over $1 billion are called unicorns. India has added 25 unicorns to its start-up books so far this year as against nine in the whole of 2020. Despite producing so many unicorns, the country hardly has listed digital players.

The rise of unicorns shows that India’s tech start-up ecosystem is on a growth path on the back of rapid digitalisation and adoption of modern technology as the world crawls out of the COVID-19 pandemic. As a nation with 65 per cent of its 133-crore-strong population falling within the age bracket of 25 to 35 years, India stands at a demographic sweet spot. The rise of the millennials is its biggest hedge against a catastrophic setback from the tech IPOs.

Markets watchdog Securities and Exchange Board of India (Sebi) has allowed loss-making companies to get listed but it has a mechanism in place to protect retail investors. Unlike in normal cases where profitable companies can offer 35 per cent of the book to retail subscribers, loss-making companies can part only 10 per cent with retail investors at the time of listing. The rule tries to protect investors from trusting companies which have not shown any road to profitability.

Many like economic historian Jairus Banaji feel that the digital start-ups are focused on exits and valuations, and are not really invested in long-term growth. But Sajith Pai, director of Blume Ventures, disagrees. “Zomato has 162,000 riders. This means that 1.6 lakh families are benefiting from the earnings that this job provides. The millions of gig workers that Zomato, Swiggy, Urban Company, Rapido, Dunzo, Uber and Ola employ are creating a new urban and semi-urban lower middle class, pulling their families out of poverty and darkness,” he says.

(With inputs from Shruti Sonal)