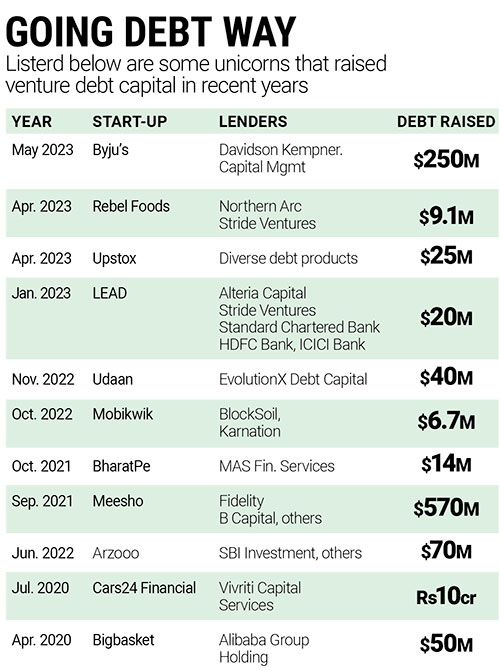

When in doubt, turn to debt. That seems to be the mantra for a growing number of start-ups looking to raise capital. Last month, Think & Learn, which runs the edtech decacorn Byju’s, raised $250 million from Davidson Kempner Capital Management, a US-based investment firm. This is part of an ongoing $1 billion funding round which it hopes to close soon.

This funding comes when the Indian edtech giant faces several headwinds. In April 2023, BlackRock, which has less than 1% in Byju’s, slashed the value of its investment by nearly 50%. The US-based asset manager pegged its per-share value at $2,400 in December 2022, down from $4,600 in April 2022.

In the same month, global investment group Prosus put the fair value of its 9.67% stake in the edtech at $578 million. This slashes the valuation of the edtech major to around $6 billion from the $22 billion valuation last year.

Recently, Bloomberg reported that Alpha, Byju’s non-operating holding company in the US, was sued by its lender, Glas Trust Company, which claimed the former had defaulted on a $1.2 billion loan. The lawsuit against Alpha, Byju’s director Riju Raveendran and Tangible Play Inc alleges that the company also hid $500 million from its lenders and transferred it out.

3 February 2026

Get the latest issue of Outlook Business

Calling the accusations of hiding the money “bewildering”, Byju’s stated that though it did transfer the funds to other operational entities, this act did not “contravene any Credit Agreement”. Instead, it claimed that the money was transferred to other operative entities for growth and expansion in its global operations.

The constant barrage of news about its financial dealings is symptomatic of the challenges that the edtech has been facing for the past couple of years. Could this be why it finally decided to raise capital from investors specialising in debt financing rather than traditional venture capitalists (VC) like Sequoia Capital, Prosus, General Atlantic, Sofina, Tiger Global and CPP Investments that backed it? A mail to Byju’s for responses to a few queries remained unanswered till the time of going to print.

Crashing of Dreams

Founded almost a decade ago by former school teacher Byju Raveendran and his wife Divya Gokulnath, Byju’s has raised over $5 billion in funding from equity and debt investors to date. Over the years, it made many overseas acquisitions, investing around Rs 9,000 crore, to fuel growth, roped in actor Shah Rukh Khan and later footballer Lionel Messi as its brand ambassadors, sponsored the jersey for the Indian cricket team, became the lead sponsor of the country’s cricket team and also an official sponsor of the FIFA World Cup.

Byju’s meteoric rise was the stuff that dreams were made of for most self-made entrepreneurs; its valuation shot up from $1 billion in 2018 to an eye-watering $22 billion by 2022. However, its voracious aspirations for global dominance soon took precedence over all else, including financial prudence. Its aggressive expansion strategy and breakneck spree of acquisitions sowed seeds of impending disaster.

Byju’s delayed the filing of its FY2020–21 audited results for almost 18 months after its auditor, Deloitte, raised concerns over several controversial issues in its accounts. Questions about its accounting practices and reluctance to come clean were also raised by parliamentarian Karthi Chidambaram on social media, putting more pressure on the edtech company.

The poster boy of the start-up ecosystem started earning side glances of suspicion because of charges of financial irregularities, poor corporate governance policies and failing reputation amongst its customers.

When the Chips are Down

Byju’s clocked a revenue of $305.6 million in the financial year, which was way below its own projections. Losses ballooned to $577.4 million, up from $32.9 million in FY20.

In a conversation with The Economic Times, Raveendran maintained that the company had recorded “significant growth in revenue compared to financial year 2020 but because of revenue recognition changes, it’s getting pushed to the next financial year”.

Earlier this year, some of Byju’s early investors, including Lightspeed Investment Partners and Chan Zuckerberg, sought to sell their stakes of 2.4% each in the company.

With its equity capital drying up, costs mounting and profits looking increasingly like a mirage, it was predictable that Raveendran would turn to alternative credit to sustain the edtech firm’s business operations. This all-weather product would give the company’s founders, including wife Gokulnath, access to capital without giving up ownership.

Vinod Murali, managing partner at Alteria Capital Advisors, which offers long-term debt capital to VC-backed start-ups, says, “The utility of debt to extend cash flow runway is understood more acutely in contemporary situations when equity is harder to come by. Founders can use the debt to accelerate growth or to extend runway.” According to him, any instrument which allows founders to reduce dilution and improve their ownership levels is worth its weight in gold and in difficult macro conditions, the weight is felt even more.

Skirting Challenging Terrains

For now, raising venture debt capital fits Byju’s requirement perfectly as profits remain elusive. However, Ravi Chachra, the founder of venture debt firm 8vdX, notes that companies that are not profitable or do not have a clear path to profitability could be required to pay higher interest rates while adhering to stricter terms. Since borrowed money needs to be paid back with interest, it is a struggle for companies with limited cash flow, few assets or uncertain revenues to meet repayment obligations. Moreover, Chachra believes, for entities which are unable to service their debt, the risk of default and potential loss of control of the company is higher.

For Byju’s, debt finance is in addition to the firm’s ambitious plans for a $1 billion IPO for its subsidiary Aakash Foundation, which got pushed after the Enforcement Directorate (ED) started investigating Byju’s over alleged foreign exchange violations under the Foreign Exchange Management Act (FEMA).

There are also reports that Byju’s has not paid several of its vendors for months. The Morning Context reported that “some of the payments are due since March and there is trouble with their clearance. In the eight months to October 2022, cumulative dues to vendors have crossed Rs 90 crore.” Byju’s did not comment on this allegation.

Byju’s Dilemma

While auditing its FY21 financials, Deloitte had pointed out that that the edtech firm had reclassified interest paid to lenders on behalf of its customers in respect of the loans which it extended to them from its finance cost. This was adjusted against revenues since these payments were in the nature of payments to customers. For instance, if it sold a three-year course, it would consider the complete sale amount as revenue for that financial year. In reality, though, these revenues were deferred over the span of time the three-year course.

In such a situation, venture debt finance can act as an interim support system to meet working capital needs. However, ultimately, the start-up has to display a modicum of profitability to repay lenders and manage the cash flow that can keep its business functioning. “This is only a stop-gap arrangement until the company turns profitable. In the current funding winter scenario where even equity money has dried up, it will be extremely challenging for companies with no clear path to profitability to service venture debt,” says Ankur Bansal, co-founder and director, Blacksoil Capital.

Signs of Impending Implosion?

Byju’s is reportedly trying to repay part of the $1.2 billion term loan B it raised in 2021 and was renegotiating terms with some lenders seeking a prepayment of $200 million. However, since these lenders are a minority in the matrix, the chances of they being able to swing the previously agreed terms is marginal.

The big dilemma facing Byju’s is how it will recalibrate its complex financial web amid mounting losses and declining sales. It will also have to trim its expenses drastically since its total expenditure increased from Rs 2,873.34 crore in FY20 to Rs 7,027.47 crore in FY21. Notably, business promotion expenses was where it spent the most in that fiscal, increasing its marketing spend from Rs 900 crore in FY20 to Rs 2,251 crore in FY21.

Taking prudent steps is more vital now than ever, as Byju’s is gearing up for a $700 million fundraise at a flat $22 billion valuation, as reported by The Financial Express. It had last raised a $250 million round in October 2022 at the same flat valuation.

The ongoing funding winter will make any kind of fund raising an uphill task, especially as recession fears frost over the global economy. Macroeconomic issues like the Ukraine-Russia war and the global supply chain crisis will further strain its potential to grow against such external dynamic factors, coupled with declining number of takers for online education, which was Byju’s mainstay.“To survive the funding drought, start-ups may have to sacrifice growth and operate with frugality to edge towards better unit economics and chart a pathway to EBITDA breakeven. With the squeeze of capital limiting growth opportunities, founders may have to settle for more conservative valuation multipliers to raise capital,” Chachra advises.

Should Byju’s consider securing more debt to tide through these tricky times, it will have to be prepared for higher interest rates and stricter terms and conditions. Additionally, a lack of revenue growth may make it difficult for the company to service its debt obligations, leading to financial strain and potential default.

While an imminent fund infusion can give the edtech more time to navigate its liquidity crunch, especially as it continues renegotiating terms with its creditors, Byju’s is undeniably on a sticky wicket financially. Will it be able to pull itself out of this self-created mess and regain its former glory?