Rishabh Mariwala grew up in a South Mumbai apartment building with his grandfather, father, uncles and aunts occupying different floors. All connected to fast-moving consumer goods (FMCG) company Marico, whose products sit in nearly every Indian household, from Parachute to Saffola.

Money, Succession and Legacy: Inside the Family-Office Playbook of India's Billionaires

India’s wealthy are creating family offices to preserve legacy, compound riches, fund philanthropic passions—and are emerging as a reliable source of domestic capital

Illustration: Saahil

Advertisement

Mariwala’s path was charted out: joining the family business and carrying forward the legacy. And he did just that for a while. But he wasn’t convinced of this script.

“I was proud of what my father had built,” he recalls. “But I realised that it was my father’s identity. It is not my identity. What am I doing for me?”

He started his own business, a soap company, in 2010. It took him five years, but he realised he was a better investor than an entrepreneur. He exited by selling the business to Marico in 2015.

The same year, Mariwala leveraged a family dividend payout to set up a family office after convincing his father to diversify investments. His father gave him just enough capital to see what he could do. That’s how Sharrp Ventures came to be. Today, it backs about 40 start-ups.

Across the country in Lucknow, Shrishti Sahu faced a similar conundrum. A third-generation member of the Sahu Group, which has interests spanning automotive, real estate and financial services, she did not want to join the traditional business. Her heart belonged to tech.

Advertisement

After graduating from the UK’s University of Warwick, she founded fintech company Aqaya, which she exited in 2017. She then worked in an investment fund for a year to gain insight into the world of investors.

With liquidity in hand from the Aqaya sale, she set up a family office, Swadharma Source Ventures (SSV), consolidating the family’s scattered holdings under a single umbrella.

By 2019, she was backing start-ups that the group’s traditional businesses would never have touched. “I could do my duty, making the family’s capital more forward-facing,” says Sahu.

Today, SSV has made around 60 investments.

Versions of this story are now playing out across India. More business families are setting up family offices. The timing is not accidental. The founders who built post-liberalisation India are ageing.

As these founders sell stakes, list companies or hand over control, a massive $1.5trn in private wealth could change hands over the next decade. Historically, this is the exact moment family fortunes begin to dissolve as families struggle to manage wealth across generations.

Advertisement

To avoid this fate, India’s next-generation heirs are setting up family offices to preserve and create wealth, but with an intention to shape the next generation of businesses.

No wonder, India now has roughly 400 family offices, up from just 45 in 2018. The future of Indian wealth is no longer being built just inside the legacy companies. It is being forged by scions in these family offices.

The New Munshi

Long before the term “family office” entered the vocabulary of India’s ultra-wealthy, there was the munshi. Immortalised in 1970s Bollywood cinema, this trusted figure carried a red, cloth-bound bahi-khata. He managed the household budget, mediated disputes and harboured secrets that no formal legal document could ever hold.

Off-screen, every great Indian business family relied on a real-life version of him. He was the trusted chartered accountant, the loyal family lawyer or an adviser. But back then, wealth was simple. It consisted of a promoter stake, a bank locker full of gold, a few fixed deposits and a few acres at the edge of a city. It was an empire small enough to fit inside a single person’s memory, easily discussed around a dining table.

Advertisement

The problem is that wealth has changed. Memory is no longer enough as fortunes exploded.

Simple assets transformed into hyper-complex webs of global investment portfolios, multiple operating companies, trusts and offshore properties.

The cost of failing to adapt to this complexity is brutal. A study tracking 3,200 wealthy families over two decades found that roughly 70% lost their wealth by the second generation. By the third, it rose to a staggering 90%. The culprit is rarely a bad business decision; wealth just becomes too complex to manage.

Two of America’s greatest business dynasties—the Vanderbilts and the Rockefellers—illustrate how differently this script can play out.

Railroad and shipping titan Cornelius Vanderbilt died in 1877, leaving an estate exceeding the US Treasury’s worth at the time. Yet, within just three generations, the family fortune completely dissolved. At a family reunion in 1973, not a single one of his descendants was a millionaire.

Advertisement

John D Rockefeller took the opposite route. In 1882, he established what is widely regarded as one of the world’s first formal family offices, hiring independent professionals to manage investments, philanthropy and family governance. More than a century later, Rockefellers remain among the world’s wealthiest.

So, institutionalisation could be one of the ways Indian legacy businesses ensure wealth preservation. And the Burmans, the family behind FMCG giant Dabur, did just that. They were among the first in India to officially retire the munshi model.

In the mid-1990s, they made a decision unheard of at the time: ownership would remain with the family, but management would be professionalised. This allowed individual family members to pursue independent investments without competing with the flagship.

The family members remain part of Dabur in non-executive roles. They are represented on the board but don’t draw salaries. “To avoid conflict, no one works in the business,” says Dabur’s Mohit Burman. “If your son is so smart, he can work anywhere. Why come and mess up this business?”

The family office became the vehicle through which the Burmans’ wealth came to be organised, invested and eventually passed across generations.

The transition created absolute structural clarity, says Burman. As the family expanded and individual branches developed distinct interests, the original centralised investment pool was dismantled to let individual branches build their own specific family offices. Yet, the overarching governance architecture held firm.

Today, the rest of India Inc is catching up. Driven by a post-Covid surge in markets, blockbuster listings, private-equity payouts and newly minted entrepreneurs, wealthy families are putting their capital on a professional footing.

Numbers back this explosion. Roughly 71% of Indian family offices were established after 2010, according to a study by wealth-advisory firm Sundaram Alternates.

Governance and greater control over decisions are the common reasons the affluent choose to build family offices. But behind this choice is also a generational showdown.

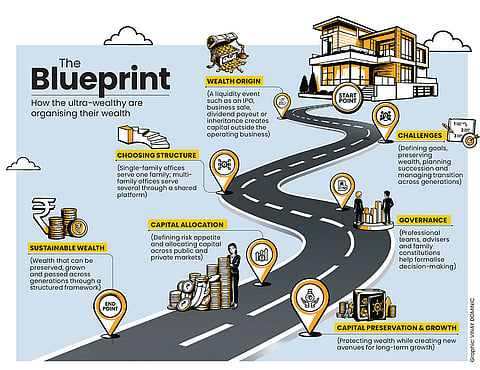

Family office at a glance

The Negotiation

Every well-to-do Indian family has lived through a dinner-table disagreement where the father insists the money belongs in a safe, predictable fixed deposit or a piece of land. The son wants to buy a limited-edition luxury watch, swearing it will double in value. The daughter is willing to bet on cryptocurrency. By the end of dinner, nobody has relented.

This core friction is visible in family businesses: the patriarchs built the empire by pouring every single spare rupee back into the core operating business. The heirs, fresh out of global B-schools, want to hunt for aggressive growth elsewhere.

“Some fathers say, ‘Okay, he’s busy, let him do it’,” observes Jayesh Faria, director and regional head at wealth-management company Motilal Oswal Private Wealth. “Others say, ‘Focus on the core business’.” Ultimately, the older generation keeps a tight grip on the capital, giving a small slice to the next generation to see if they sink or swim.

Anirudh A Damani knows this intimately. When he returned from the US in 2012, he wanted to build a professionally managed family office that would not fall apart if he stepped away. But when he started investing family capital into unlisted early-stage start-ups, his father was not convinced.

“Beta unlisted mein kaam kar raha hai [My son works in unlisted markets],” Damani recalls his father saying this at high-society Mumbai parties.

To his father, it was less like investing and more like gambling. The scepticism didn’t go away until 2015. That was the year Damani’s early bet on hospitality start-up Oyo hit a spectacular exit. The massive premium returned every single rupee the family office had invested in. This changed his father’s view of start-up investing and helped convince other family offices that the asset class deserved attention.

For 29-year-old Rachit Poddar, the reckoning arrived with a global lockdown. His father had arrived in Surat from Assam with just ₹500 in his pocket, building one of the city’s most formidable textile empires from scratch. But when Covid-induced lockdown forced the factory gates shut, father and son stared down a disconcerting question: What happens to family wealth if the operating business cannot run?

“That was the trigger point for us,” says Poddar. It sparked an immediate pivot with Poddar establishing a formal family office, which made more than 80 private-market investments over five years. Today, he is expanding the textile business while building an investment portfolio.

Yet, as the family office boom accelerates, business titans like Uday Kotak and Harsh Goenka have publicly questioned these heirs, criticising them for choosing the comfort of capital allocation over the rigour of the factory floor.

Mariwala understands the root of this criticism. “The stereotype is family offices sitting on golf courses and partying in different parts of the world. People assume it means unstructured, non-strategic, no discipline. That has to change,” he points out. For him, Sharrp Ventures is a full-time job. “We’re not silent spectators. We’re active investors.”

How the ultra-rich is organising its wealth

Not Just Money

On any given weeknight, actor-investor Vivek Oberoi’s family sits around the dinner table discussing the family’s investments. His children, aged 11 and 13, already know which company the family has backed, the thesis behind the bets and the mistakes they made along the way.

These talks are important for Oberoi. He believes waiting for a crisis to have these conversations is a catastrophic failure of leadership. “The family office is not just about passing down capital,” he insists.

“It’s about passing down governance, values and relationships,” he adds.

Yet, the moment a family office is set up, the talks immediately become about investments. Will it be public markets, start-ups or real estate?

“The most common mistake we see is that there is no goal defined,” says Vikas Satija, managing director and chief executive of Shriram Wealth, a wealth-advisory firm.

When building their core businesses, these titans had clear goals: grow revenue, expand capacity and enter new markets. But with money, the objective is usually less obvious. Is the goal to preserve their wealth, fund an extravagant lifestyle, start a business or fuel philanthropy?

Once the goal is clear, the rest falls into place: how much risk to take, where to invest and what role the next generation plays. This is where the family office playbook begins.

“Wealth management is the entry point,” says Motilal’s Faria. “That’s how you get a seat at the table. Then you start discussing succession, cross-holdings and estate structures.”

Questions of ownership, succession and control have tested some of India’s most prominent business families and the market has not always been forgiving.

When Reliance founder Dhirubhai Ambani died unexpectedly in 2002, he left no will and no succession plan. Within two years, the rivalry between his sons, Mukesh and Anil, spilled into public view, creating uncertainty around the group’s future and adding volatility to its share price. The eventual 2005 split of the empire stabilised the markets, but the feud became a cautionary tale for every boardroom in the country.

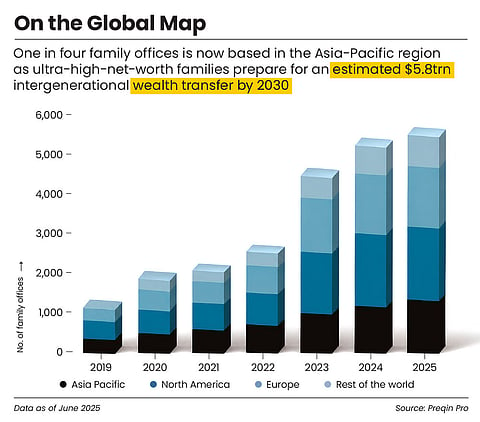

Apac on the global map

From the Bajaj family spending a decade reorganising ownership to the Birlas fighting inheritance battles in open court, history proves that when a dynasty cracks, the collateral damage hits everyday shareholders.

According to a joint report by accounting major EY and wealth-management firm Julius Baer, only 59% of wealthy Indian families have a documented succession plan. The rest still rely on informal arrangements.

However, succession is only one part of the equation. Families also have to decide how future generations are introduced to wealth, how philanthropic commitments are carried forward and how the family’s reputation is protected.

Family offices invest their own money, which can stay invested for longer and move across asset classes

“You can build the most sophisticated structure and still have the family fighting in court the moment the patriarch is gone,” says Satija. “If you do the inheritance planning well, the assets transfer smoothly.”

To achieve this, many business families are drafting family constitutions. While not legally binding, this document acts as a cultural and operational code of conduct. It maps out who gets a vote, how spouses are integrated into financial decisions and exactly what happens when siblings disagree over shared assets.

When textile heir Poddar put his family through the exercise, the level of detail surprised him. “Budgeting everything—from your personal lifestyle to wealth creation, investments, business expansion, diversification. Defining everything,” he recalls.

Drafted with external mediators, these constitutions draw a legal firewall, separating corporate money, shared family assets and personal lifestyle choices.

The family office is, ultimately, the institution built to hold all of this together, the wealth, the succession, the governance. It gives wealth a structure, making it easier to deploy beyond family business. “A family office is not just about creating alpha,” says Mariwala. “It is not just wealth preservation. It is wealth creation.”

Desi Capital

A few months ago, Damani received a phone call from a US-based founder he had backed years prior. The company, now a unicorn, needed $5mn in fresh capital. Damani reached out to his network of fellow Indian family offices.

In less than four weeks, they assembled a special purpose vehicle of $10mn. “Ten years ago, nobody in India could have pulled that together,” he says.

For over three decades post-liberalisation, foreign capital, be it private-equity firms, sovereign-wealth funds or venture capital, played an important role in financing parts of India’s growth story. That capital has helped build some of the country’s most successful businesses and remains important. But recent events have also shown how quickly they can retreat due to geopolitical forces.

The danger of relying on global money became painfully clear in 2020. Chinese investors were among the most active backers of Indian start-ups, sitting on the cap tables of 18 of India’s 30 coveted unicorns. Then came the Galwan border clash.

New Delhi swiftly tightened investment regulations, and massive capital flows from Beijing slowed dramatically.

The lesson extended beyond China. Interest rates in the US and shifts in global risk appetite increasingly influence where money flows.

India’s net foreign direct investments have nosedived from a robust $44bn in 2020–21 to less than $1bn in 2024–25, before staging a modest recovery to $7.6bn in 2025–26.

Foreign portfolio investors have withdrawn roughly $34bn from Indian equities so far this year, outpacing about $18bn pulled out during the 2025 calendar year.

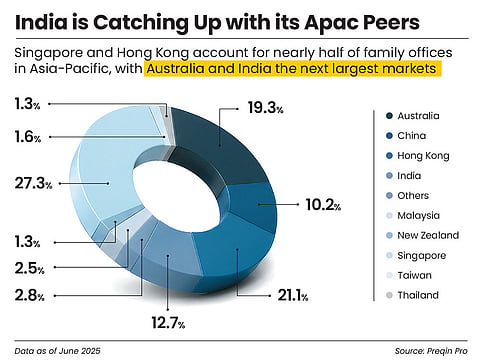

India catching up with its Apac peers

That is why building domestic capital is vital. Not as a replacement for foreign money, but as a counterweight to it. “It matters enormously because global capital is becoming less reliable,” says Mariwala. “If domestic capital, whether from family offices or local institutions, doesn’t back the India story, we remain entirely dependent on foreign money that can leave at any moment.”

Family offices are emerging as one part of that domestic capital base. Unlike PE/VC funds, they invest their own money. Unlike institutional investors, they do not answer to limited partners or fund cycles. Their capital can stay invested for longer and move across asset classes.

“Instead of three years they can go to five,” says Motilal’s Faria. “Instead of 18% IRR [internal rate of returns] they can agree to 17%.”

For a young company, that 1% can mean the difference between an investor pushing for an exit and one willing to wait.

Damani describes this as the flying-geese effect. As wealth creation ripples across the economy, one generation of family offices is funding the creators of the next. Those who benefit from that growth eventually accumulate enough wealth to build family offices of their own.

What makes India unusual is how broad the base already is. The country’s billionaire population has risen from around 59 in 2012 to more than 200 today and is projected to grow sharply over the coming years.

However, experts argue that India’s domestic capital base is still in its infancy. “We have about 400 family offices in India today,” says Rishabh Shroff, partner at law firm Cyril Amarchand Mangaldas. “I think we are ten times too short for where we need to be. The US has 8,000.”

Damani agrees. If India wants to achieve its $30trn goal by 2047, it will need far more institutions capable of deploying long-term domestic capital, he argues. “It is a nation-building exercise. Not just for families.”

And as family businesses account for over 70% of India’s GDP and 60% of its employment, the question is no longer whether they can create wealth. They have already proven that. The question now is whether family offices can become part of the long-term desi capital base that will fund India’s next phase of growth.