In the pharmaceutical industry circle, turant was the name used when one spoke of the Ahmedabad-based Torrent Pharmaceuticals. Turant is ‘immediate’ in Hindi and the word was really to drive home the point on the company’s ability to move quickly, be it launching new products or the pace of decision-making. It was a title, which was used in a big way in the late 1980s and early ’90s.

At that point, Torrent was known to launch at least two products for one from competition. The foray into power by the group in 1996 shifted the focus away from pharma and precious time was lost. Now, Torrent appears to be determined to get back a slice of the pharma story, which it ceded to rivals. The buyout of Unichem’s branded businesses in India and Nepal, earlier this month, for a handy Rs.3,600 crore is a step in that direction. This move helps Torrent to become the fifth-largest player in the Indian pharma industry from its thirteenth position. The deal has been struck at an EV/sales valuation of 4.3x (Unichem’s Rs.860 crore sales from these two markets). The acquisition gives Torrent, which clocked a revenue of Rs.5,850 crore in FY17, a portfolio of 120 brands, a plant in Sikkim and 3,000 employees.

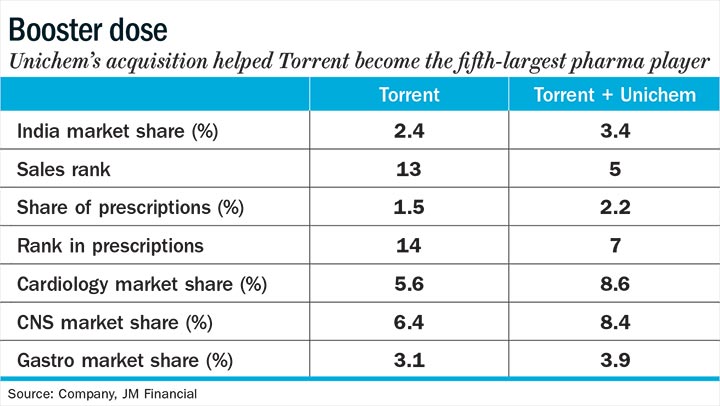

In a statement following the announcement of the deal, Samir Mehta, Torrent Pharma’s chairman, said the acquisition will strengthen his company’s presence in cardiology, diabetology, gastro-intestinals and CNS apart from realising cost and revenue synergies in the Indian branded business. (See: Booster dose)

3 February 2026

Get the latest issue of Outlook Business

This also marks the company’s fifth acquisition since the Rs.2,000 crore buyout of Elder Pharma’s domestic formulations business in late 2013. Apart from the Elder acquisition, Torrent acquired a couple of brands from Novartis, a manufacturing facility from Glochem and the derma-formulations manufacturer ZYG Pharma. The buyout of Unichem is substantially larger and brings to the table Losar, a cardiovascular drug with a turnover of close to Rs.200 crore, and Ampoxin (anti-infective) and Unienzyme (gastro-intestinal), together bringing Rs.130 crore besides improving its reach to an additional 2,100 stockists. Unienzyme will be Torrent’s first OTC (over-the-counter) drug. The deal will be funded with a debt of Rs.2,400 crore and the rest coming from internal accruals.

A key part of Torrent’s strategy is to increase its presence in the domestic market, which is growing at 10-12%, while the US market, a big story for most players, is under some serious stress. In the case of Torrent, in the September quarter of FY18, the US business, was down 21%, while the domestic formulation business grew by 22%. “The US market is getting to be a lot more challenging with a more stringent USFDA and a lot of pressure on the pricing front. For Torrent, the domestic market, by contrast, has always been its stronghold and one it understands well,” thinks Praful Bohra, research analyst, Equirus Capital.

Torrent will bank heavily on its learning from the acquisition of Elder Pharma. The seller here was financially troubled and the sweetheart deal came only with the brands. At the time of the acquisition, each of Elder’s medical representatives brought in, on an average, Rs.3 lakh revenue. In less than three years, that number has doubled to Rs.6 lakh on the back of a relentless focus on two key brands, Shelcal and Chymoral. Consequently, the Elder brands have grown at an average of 23% every year over the past three years compared to an industry growth of 11%.

The challenge at Unichem is no different, with its key brands not harnessing their potential. Besides, the revenue from each medical representative is around Rs.2.7 lakh, with the industry leader, Sun Pharmaceutical Industries at Rs.14 lakh. Losar, Unichem’s largest drug, has just got out of price control and Bohra says even a marginal price hike will healthily improve Ebitda margins. “A rationalisation of workforce is quite likely since both companies deal in the same therapeutic areas. There will be a thrust in the OTC segment and all these put together will positively impact margins.”

There have been some questions on the valuation of the deal to suggest it is on the higher side. Mayur Sirdesai, director, Somerset Health Capital Advisors does not think so since it is difficult to find an asset of this size easily. “Also, there are some large brands in both Rx (prescription) and OTC, which can justify higher multiples and many of them being older brands, mean higher margins. There have been larger multiples paid before and it is not expensive as long as Torrent can scale this business further over the years.”

What also works in Torrent’s favour is Unichem’s presence in Tier 2 and 3 towns for its key brands. There was a perception in the past that in smaller centres there would be demand only for acute therapies. “Now, it is obvious there is a significant opportunity for chronic as well, with older companies seeing a lot of stickiness for their legacy brands. Torrent is buying over Unichem’s legacy brands, which saves it time, apart from opening up the market immediately,” says Sirdesai. For Torrent, the domestic story is what is now tickling it.