One of our investment thesis is to find a good company going through a temporary bad phase, because when good times come these companies make the most of the opportunity and go on to deliver multi-bagger return through a combination of growth in earnings and re-rating of valuation from a depressed state.

One such stock that makes the cut is Greenply Industries, which makes plywood & allied products, and medium density fibreboards (MDF). The stock is down more than 60% from its recent high. For a company like Greenply, which has a strong track record of operating performance, and considering other factors, the correction offers a good opportunity to invest from a three- to four-year perspective.

Beefing Up

3 February 2026

Get the latest issue of Outlook Business

Greenply recently commissioned a new MDF plant with a capacity twice that of its older plant. In doing so, its total MDF capacity has increased from 180,000 cubic meter (CBM) to 540,000 CBM. Though, currently, supply is outstripping demand, we believe it is already being discounted by the market. With the new plant, the project execution and delay risk are also behind the company.

The plywood industry is worth Rs.190 billion as of FY18, though organised players account for only 25%. With rationalisation of GST from 28% to 18% on plywood and stricter implementation of e-way bill, organised players are hopeful of increasing their market share. The industry is estimated to post a 11% CAGR with organised players expected to clock a much higher growth rate between now and FY22.

The Rs.190 billion market is divided into three major segments. Till now, Greenply largely operated in the luxury-premium segment, but is now slowly increasing its presence in the medium and mass market, which is 85% dominated by the unorganised sector. The products in this segment range between Rs.70 and Rs.90 per sq ft.

With the expected shift in mix towards organised players, Greenply has launched two new brands ‘Bharosa’ and ‘Jansathi’. The company doesn’t compete in the low-end plywood segment, though it believes that MDF will take over the share of low-end plywood market in India.

Plying The Goods

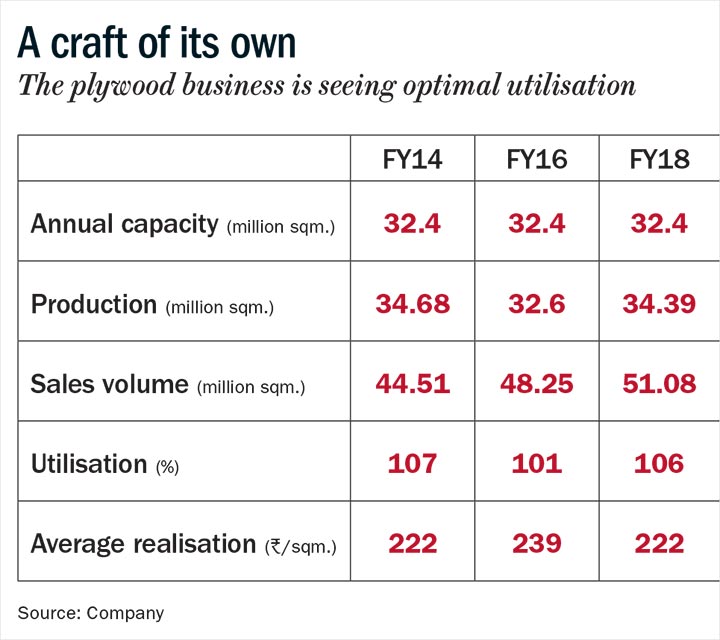

Greenply has 35.4 million sq mt of plywood capacity spread across four manufacturing facilities, which have been running at more than 100% capacity over the past few years, but is still managing year-on-year growth, thanks to its outsourcing model.

The company currently outsources 30% of its overall volume requirement and the same accounts for 22% of plywood sales, in value terms. With an increasing focus on the medium-mass segment, the management intends to increase the proportion of outsourcing over the next few years, while continuing to manufacture premium brands at its own facilities.

As a backward integration initiative, Greenply has set up a veneer plant in Myanmar and has also commenced operations at the 36,000 CBM veneer unit in Gabon, West Africa, through a step-down subsidiary. The management believes, that unlike Myanmar, Gabon has sustainable forest policies and has embarked on the process of expanding the Gabon facility for peeling of logs from 36,000 CBM to 96,000 CBM by the first quarter of FY20.

Problem Of Plenty

The domestic MDF market is around Rs.18 billion and almost entirely accounted for by few organised players such as Greenply, Centuryply, Action Tesa, and Rushil Decor, besides imports.

The market is highly under-penetrated with a consumption of just 0.8 million CBM against China’s 43 million CBM annually. Similarly, India’s MDF production capacity is only around 1.3 million CBM against a global capacity of 108 million CBM.

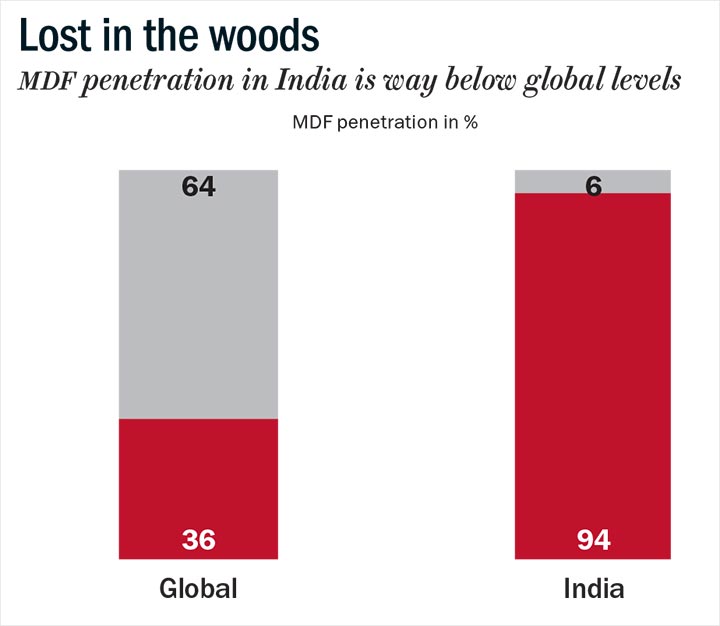

The low penetration in India can also be judged from the fact that plywood still accounts for 94% of the wood-based panels in India, while, globally, MDF accounts for the bulk of the share at 64%.

Going forward, MDF demand, currently less than a million per annum, is expected to grow at 15-20% CAGR on the back of substitution for low-end cheap plywood, transition of furniture industry from unorganised to organised, increasing use of ready-made furniture, and so forth.

India’s MDF manufacturing capacity will be around 1.3 million CBM by mid-2019, up from 0.52 million CBM in 2015. Currently, Greenply has a capacity of 0.54 million CBM, Action Tesa’s capacity is around 0.51 million CBM and Centuryply’s capacity is around 1.98 million CBM.

The aggregate domestic capacity is still paltry in comparison to the global production capacity of 108 million, of which China constitutes 43 million. Another concern for domestic manufacturers is the rise in imports, mainly from China. At present, imports account for nearly 30% of the demand.

Before Greenply’s 0.36 million CBM capacity came up in Andhra Pradesh, most MDF units were located in the north and transporting to the south wasn’t a very viable option as imported MDF cost around Rs.18,000/CBM against Indian MDF value of Rs.24,000-26,000/CBM. Though the demand for MDF is growing at 15-18%, excess capacity and imports are still high in comparison to overall demand, and with the sudden influx of so much capacity, the market has seen a price war and a fall in realisation for most players.

To counter imports, the government has levied anti-dumping duty on thick MDF, creating a price difference of 8-10% and in the thin segment, where there is no anti-dumping duty, the price gap is about 25%. It is believed that share of imports will reduce to 20% by FY21 from 30% over the past few years.

But the excess capacity is likely to pose problems of lower utilisation and realisation for domestic players over the next two years. However, as demand is growing rapidly and with some of the capacities getting used up for exports, the situation should start normalising two years from now. It is also important to note here that as the capital cost of setting up a MDF plant is high (around Rs.5 billion for 0.2 million CBM capacity), the market is dominated by organised players. With existing players unlikely to augment capacities for, at least, the next three years, the demand-supply mismatch is likely to normalise over the same period.

Of the total MDF capacity in India, Greenply has the bulk share at 0.54 million CBM spread across two plants - 0.18 CBM plant in Pantnagar, Uttarakhand, and the recently commissioned 0.36 CBM plant in Andhra Pradesh. Before the capacity deluge in MDF space, that is, till FY18, Greenply was running its Pantnagar plant at more than 100% capacity utilisation with realisation of around Rs.25,000-26,000/CBM and an operating margin of around 28%.

Coming Back

As far as the performance of the plywood division is concerned, it has been steady across the years, though the company could not grow much on account of several factors including demonetisation, GST implementation, and the overall slowdown in real estate. However, growth has started to come back with the company reporting 14.8% growth in sales of plywood in H1FY19.

The company is expanding its plywood capacity by 12-13 million sq mt by setting up a plant in UP for Rs.550-600 million. The plant would commence operations in FY20. This will be a major expansion (in terms of volumes) and will be after a gap of several years. The two brands “Bharosa” and “Jansathi” will be outsourced from other vendors. Considering the size of the mass market is Rs.97 billion and is largely unorganised at 85%, the shift from unbranded to branded will result in the company maintaining 8-10% annualised growth rate over the next few years.

The management is looking to achieve Rs.15-16 billion in revenue and an operating margin of 11-11.5% in the plywood business post its de-merger in mid-2019.

The Numbers Are Telling

The MDF division, which in the past was working at a capacity utilisation of 100% and an operating margin of 27-28%, has come under pressure over the past two quarters on both utilisation and realisation fronts. In fact, the commissioning of the company’s Andhra plant coincided with the capacities of other major players coming on stream as well. As a result, Greenply witnessed pressure on both sales volume and realisations.

Going forward, till the domestic demand picks up to match the supply, the company will be looking to ramp up the sales from the Andhra plant by doing a substantial volume of exports, though it is important to note here that realisation on exports is much lower at Rs.16,000-17,000/CBM against Rs.24,000/CBM for domestic sales.

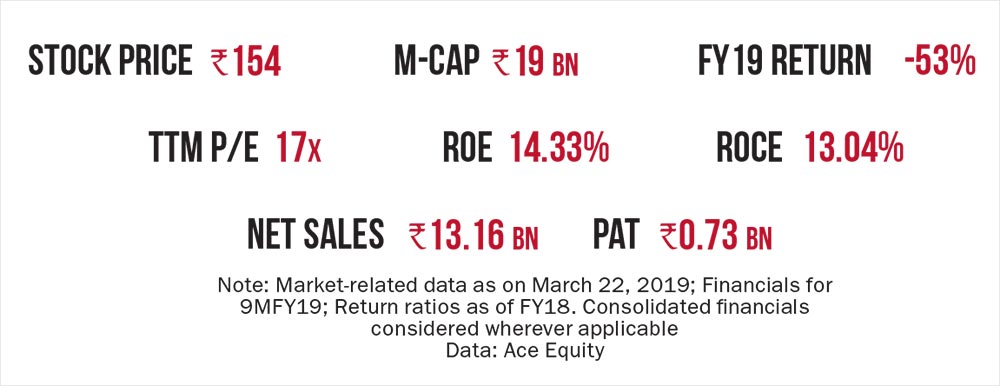

As envisaged, if the domestic demand for MDF is sustained at 15-20% over the next three to four years, then the entire domestic capacity of 0.8 million CBM will get utilised with players achieving 90-100% capacity utilisation. Greenply’s management is targeting blended (AP and Pantnagar) capacity utilisation of around 60% by FY20. Though not in the next two years, we believe the company might achieve maximum capacity utilisation in three to four years with margins stabilising around 20-23%, thus boosting the profitability of the MDF division. Over the past one year, the stock has more than halved from its high of Rs.385 to Rs.154 at present. Hence, I believe the downside from the current level is low and there could be decent upside once the MDF business recovers.

The writer has invested in Greenply Industries, and the stock has been recommended to clients as well