The Tata group has been making headlines, thanks to a battle royale playing out between the Mistrys and Ratan Tata. While there has been a lot of board room drama that has captured media attention, as investors you have to cut off the noise to see what really matters. That brings me to my stock of the year, Tata Motors. The stock has outperformed both the benchmark and peers over the past one year on the back of strong performances of JLR and India units. We believe this should continue owing to strong lead indicators of its performance in the coming quarters.

The foreign subsidiary is beating its peers, Audi, BMW and Mercedes, in the volume growth game. For the eight months of FY17, volumes surged 63% on the back of strong demand increase in its key markets, including the US (+39%), the UK (+28%), Europe (+31%) and China (+49%). Most of the incremental volume is coming from the new XE, F-Pace, and Discovery sports. The volume for Jaguar brand is rising at over 80% owing to a low base and significant new product launches in the past four years. It is outperforming the growth rate of its peers given its low base, competitive cost of production, and consistently successful new products. After the major success of LR Evoque in 2012, the company invested significantly in new models and engines. Its expanded range, including the entry-level Jaguar XE and F-Pace, has provided significant incremental volume. The Land Rover sports model also contributed strongly to volumes. But the overall volume growth for Land Rover brand was marginally negative owing to cannibalisation among its products.

Given its investments in new plants in China, Brazil, and Europe, JLR is heading towards the one million volume mark over the next few years. It may also start joint production using Tata Motors’ facilities in India. It is also working towards a connected car program and electric car development over the next five years. We expect JLR to sustain a double digit volume expansion for the next few years off a low base, supported by new products, geographies, and plants. Even though, JLR’s profit came down in first half owing to a sharp decline in GBP vs USD and EUR, we believe it is temporary. JLR has clarified that it will not be negatively affected by Brexit in the long term because it will benefit from GBP weakness as 80% of its volume from the UK is exported and this will offset the cost of the 40-50% component imports from the region.

3 February 2026

Get the latest issue of Outlook Business

The catalysts for 2017 and 2018 for JLR will come from a) expected launch of new full-body aluminium products, including the new Evoque convertible which was just launched. The Discovery Sports in January’17, mid sized Range Rover in June’17, a smaller F-PACE and an I-PACE by late 2018, b) new plant at Brazil which started operations in June and a new plant in Slovakia which will start operations in late 2018. JLR has earmarked an annual capex of £2.5-3 billion and by the end of 2019 it would have completed most of the gaps in its product line vis a vis its global peers. By 2020, its total volume could reach up to a million units per annum from less than 600,000 units expected in FY17.

Even though, JLR is almost 1/3rd in sales compared with its peers, it is competing very well with the other German luxury car makers. It has significantly improved its cost competitiveness, has invested in new design, engine technology and revamped the old product line to woo young buyers. JLR has a long way to go, owing to its relatively small size but given that the luxury car segment is just 5% of global car production, there is plenty of room for JLR and its peers to grow.

The worst is over back home

Tata Motor’s India business consists of truck and passenger cars. In the trucks business, it is the leader with a market share of 49%. This segment forms 80% of its standalone revenue. In the medium and heavy trucks category, Tata has 50%-plus market share. In this segment, its volume growth is expected to be in the single digit. But the company is confident of a pick-up in demand for heavy trucks in the 4QFY17 and, thereafter, owing to the implementation of compulsory BSIV emission norms. This would require truck owners to change their fleet. Truck prices are expected to rise by Rs.60k-100k from April next year, following a change in components. The truck business of Tata Motors India has been generally profitable and enjoys significant operating leverage as it utilises only 60% of its capacity, at present. Tata Motor has consistently upgraded its truck technology and design in order to increase market share amid growing competition from Daimler, Eicher, Mahindra, Ashok Leyland, SML Isuzu and others. Of late, it has also concentrated on government business for bus tenders under the urban renewal mission, besides bidding for defence contracts and exports to Asian, African and Latin American markets.

Passenger car pain

In the passenger car segment, the company’s market share has come down to 5% from 9% about four years ago. This happened owing to various factors including a) gap in product portfolio versus Maruti, Hyundai, Renault, Honda and others, b) lack of investment in new product platform and c) lack of strong leadership. The company seems to have addressed most of these problems and is now looking confident of attaining back its 9-10% market share. It has introduced a new Revotron engine for its small cars, enabling more fuel efficiency and smooth running.

The same engine has been used in its new models Zest and Bolt, thus addressing the perception that the company was not interested in growing its domestic car business. The big breakthrough, however, has come following the launch of Tiago this year. It has been a runaway success with its attractive design aimed at millennial customers. The company has now lined up the launch of new Hexa, a compact SUV, which is a fast growing segment in which Tata does not have a presence. It is also planning to launch the Kite V sedan, a compact SUV Nexon in the next fiscal and an all-new modular platform in late 2017 or 2018. More importantly, the company has strengthened its brand in the car segment by separating its truck and car dealers. We believe, it is a matter of time before the company starts showing a strong performance in the domestic business.

Sound bet

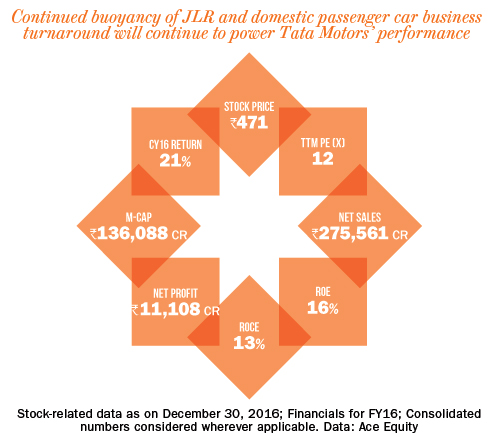

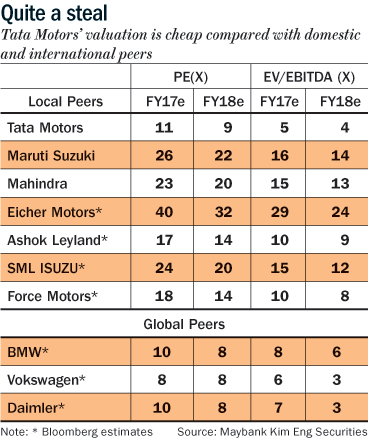

Overall, the company’s balance sheet is very healthy with a net debt-equity of 0.1x. Its free cash flows should be significant after it completes the capex cycle at JLR in another two years and it could also unlock value by monetising some of its subsidiaries, including Tata Finance, Tata Technologies among others. At 4.5x estimated FY17 EBIDTA, the valuation is undemanding. Our target price of Rs.726, based on an 5x estimated FY18 EBIDTA - same as its long-term average and 30% discount to peers.

The author does not hold the stock in his personal capacity, but has recommended to clients of Kim Eng securities