Ask not why, but it is difficult to beat the market over long periods with mutual funds.Your fund manager has to get a whole bunch of things right to race ahead and make superior returns. First, he has to pick the right stocks at the right price which of course sounds so easy but is the most difficult thing to do. Depending on the fund size, getting the allocation right becomes critical. Simply spotting multi-baggers won’t do any good – you got to deploy enough cash in your conviction to move the needle. Then there are a whole bunch of restrictions fund managers have to adhereto based on the investment mandate of the scheme.

The fact that fund houses keep launching new schemes to cash in on prevailing trends and shore up assets without regard to the long-term potential of a trend also poses a serious challenge in maintaining performance.

And then, there is the challenge of managing fund flows in the case of open-end funds. Ironically, in the stock market there is higher demand at high prices, which means mutual funds tend to attract maximum flows when the market is approaching a peak, and maximum redemptions in a falling market. And given the self-imposed, save-your-backside approach that mutual funds take of remaining invested at all times, there is no chance to escape deep dives in the market to preserve capital either, nor can you exercise a period of inaction when stocks prices are elevated.

All this simply makes the odds of earning a high return from mutual funds highly improbable. Load on to this, the expense fee of 2.5% charged annually by the asset manager, and you are impoverished even further over time. To give you an idea of how this miniscule percentage difference can alter your overall return over a long period, here is the math. In 10 years, your Rs.100,000 will grow into Rs.259,000 compounding at the rate of 10% per year, but at the rate of 7.5% the amount would be Rs.206,000. Essentially, you would earn Rs.53,271 less, which is 50% of your principal amount. The difference grows enormously over long periods. At the end of 30 years, at 7.5% the same Rs.100,000 will turn into Rs.869,000 — that’s nearly half of what your amount would have grown into at the rate of 10% (Rs.1,745,000).

Against this backdrop, it’s quite commendable that there are fund managers in India who have generated a return in excess of what the indices have delivered over a long period.

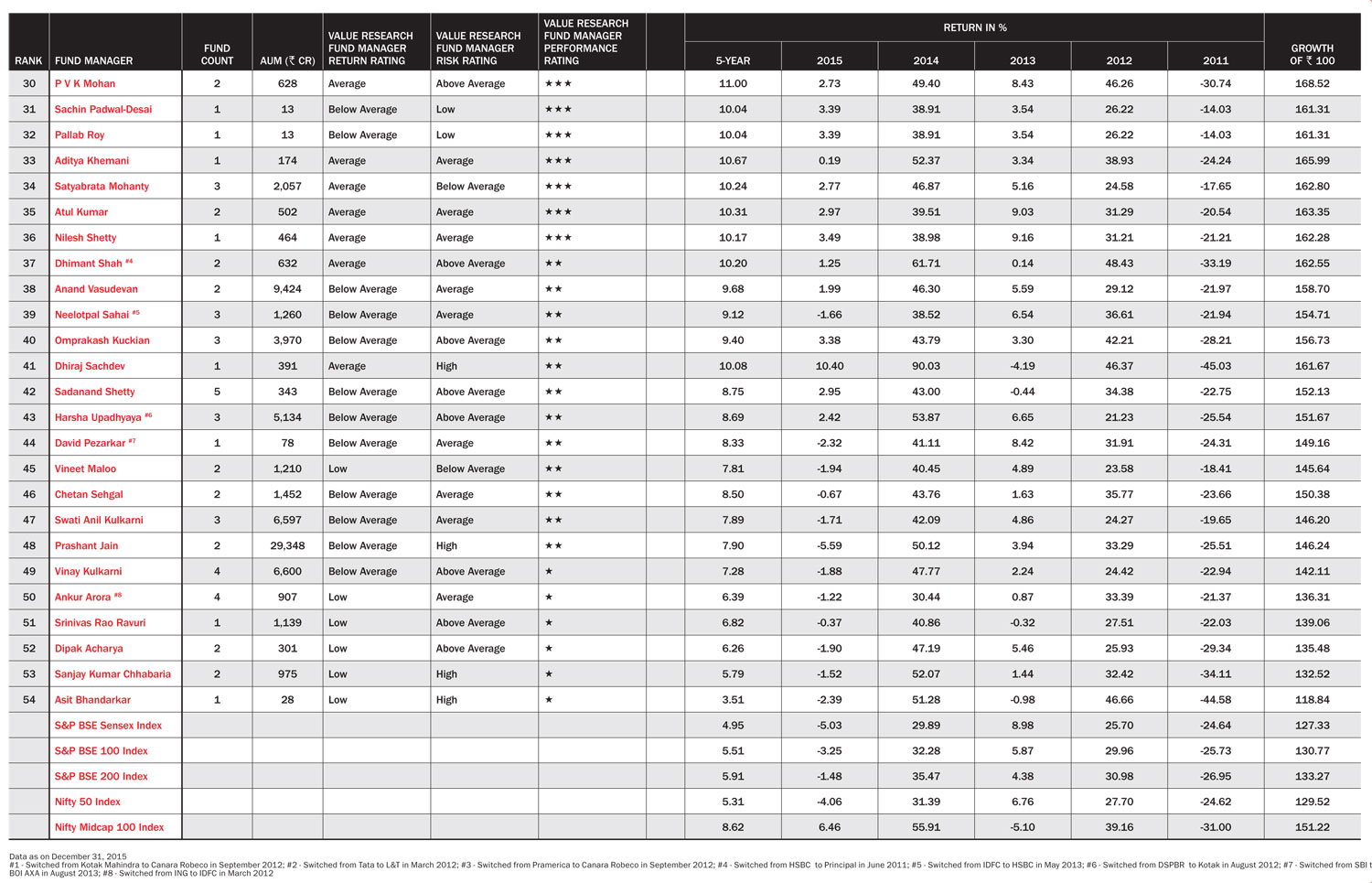

But we do not have too many managers with a long track record as several experienced hands have either quit the industry or moved to other fund houses. As it is, choosing the right fund or manager is anyway a complicated exercise. This is where the Outlook Business-Value Research Fund Manager Ranking will help. The ranking is based on the average risk-adjusted performance of all fund schemes managed by a manager and across fund house in case s/he has switched the fund house. We have presented rankings based on both 10-year and five-year, and profiled the top 10 managers based on the five year track record and the top two based on 10-year track record.

Although a five-year history is too short to assess the abilities of a fund manager because the period does not make up for even one market/business cycle, watching this record is important as most investors would expect that their funds deliver over a five-year period. Not just that, a five-year period is a reasonable time for you to wait and see if you have made the right choice. If you stay put for 10 years and found that the fund manager you handed your money did not do a good job, you have no hope of making good that damage. If you take a peak working life of 30 years, 10 years accounts for a third of your savings and you better not have made a wrong call for that long.

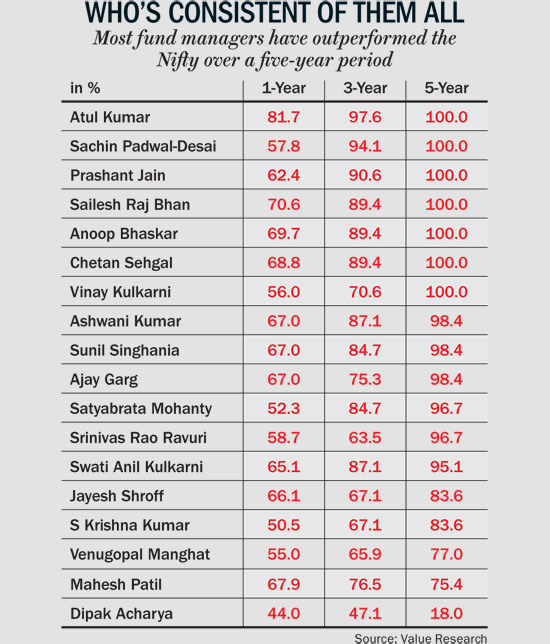

So far, fund managers with a 10-year track record have done a tremendous job of beating the indices. Out of the 18 fund managers rated on 10-year performance, seven outdid the Nifty 100% of the time based on five-year rolling return — rolling returns were calculated month-wise (see: Who's Consistent of Them All). What this essentially means is that if you handed these managers your money for any 60 month (five-year) period after January 2011, it would have grown better than the Nifty.

This spectacular performance has come on the back of superior stock selection in a market that has seen a burgeoning number of small and mid-cap companies. “Way back in the mid-nineties, fund managers used to by and large follow the same strategy. Our framework for evaluating them in the mid-nineties used to be how much was their exposure to consumer, pharma and technology when those sectors were doing well. That has seen a stark change since 2008,” says Dhirendra Kumar, founder, Value Research.

Ever since the market surge of 2003, many small and mid companies have become a playing ground for fund managers. While the infra boom ensured that the market paid disproportionate attention to mid-caps in core sectors, in the aftermath of the crisis the other sectors came alive. “Especially after the 2008 fall, identifying the right stocks at the right time became the big driver of returns. Managers who identified the right stocks and backed them took rich rewards,” says Kumar. After all, in a market where business visibility and macro fundamentals have dilly dallied, stock selection has become the secret sauce to success. Over the past five years, mid-caps have outperformed large-caps and accordingly larger funds with large-cap focus have lagged behind. The five-year track record bears out this skew. But this party may not continue forever.

Markets move in cycles and trees don’t grow to the sky. This proposition, however, is not something everyone subscribes to. And this difference in approach — a value-focused, contrarian approach versus growth-oriented approach — is visible in the fund industry more than ever. There are managers like SBI Mutual’s R Srinivasan who are betting on growth and others like Prashant Jain who are sticking to value. This contradictory stance taken by managers will ultimately get reflected in their performance over time. Being with the right manager will therefore be more important.

Another aspect that will make a difference across managers, more importantly across schemes, is the size of funds. Even though big funds say that size does not affect their performance, in relation to the liquidity in our market, their size will be a deterrent. Some managers like Jain argue that the size of funds is not an issue (see: Prashant Jain vs Mr. Market). But it will be even more important for the bigger funds to get their big calls right. Kumar feels size will alter the game for a lot of managers. “Yesteryears funds are a victim of their own success. The trend is visible in the numbers. For example, Sunil Singhania’s bigger funds are struggling while the smaller ones are doing very well,” says Kumar.

More than whether size is an impediment to outperformance or not, the context in which fund managers have outperformed all these years is important to note. By and large, ever since 1993 when mutual funds were opened to private players, most funds in India have succeeded with a bottom-up stock selection process. How else could you have made money when the indices went nowhere? The shallow nature of the market and huge inefficiencies gave more than ample room to beat the indices by picking the right stocks. That’s an approach managers have mastered.

Now some of them will have to graduate from looking at large outperformance from tiny islands of opportunity to decent outperformance with large bets avoiding landmines on the way. That is both a challenge and an opportunity for the big fund managers. This being our first edition on mutual funds, we have confined it to giving you a flavour of their investment strategy. What finally counts is the rigour of your research and how much conviction you show in your own independent analysis.

Coverage

Fund managers

The study covers fund managers having a track record of managing at least one fund for the past 5- and 10-year periods ending December 31st, 2015, leading us to a universe of 54 fund managers.

Funds

- The study covers diversified equity funds across large-cap, mid-cap, small-cap, multi-cap and tax planning categories as defined by Value Research. All sector funds, thematic funds and passively-managed funds (index, ETFs, quant) have been excluded.

- This led us to a starting list of 169 equity schemes managing Rs 230,607 crore for the five-year period and 81 equity schemes managing Rs 121,714 crore for the 10-year period.

Performance record

- The study is based on the performance record of the past five years (January 2011-December 2015) and 10 years (January 2006-December 2015).

- Only the relevant portion of a fund’s performance history, corresponding to a fund manager’s tenure at that fund, has been taken into account to rate that manager.

- The performance of co-managed funds has been taken into consideration for each of the co-managers.

Evaluation methodology

- We collated a simple average of the percentage return delivered by a fund manager in each of his covered funds. If the fund manager moved from one fund to another, the relevant track records were aggregated. This gave us the unified performance history of a fund manager. The same process was followed for both 5- and 10-year periods. Think of it like this: if a fund manager was managing only one fund in the past five years, this would be its performance record.

- We deployed the Value Research fund rating methodology, which is based on risk-adjusted return, to arrive at the relative ranking of fund managers.

- This is purely a quantitative study based on risk-adjusted performance. No qualitative assessment has been performed.