India Inc has a new worry line. Apart from the usual labour issues, bottom lines, capex, expansion many companies are increasingly being affected by geopolitics.

Geopolitics Shackles India Inc’s Green Transition, Says Teri-Outlook Business Survey

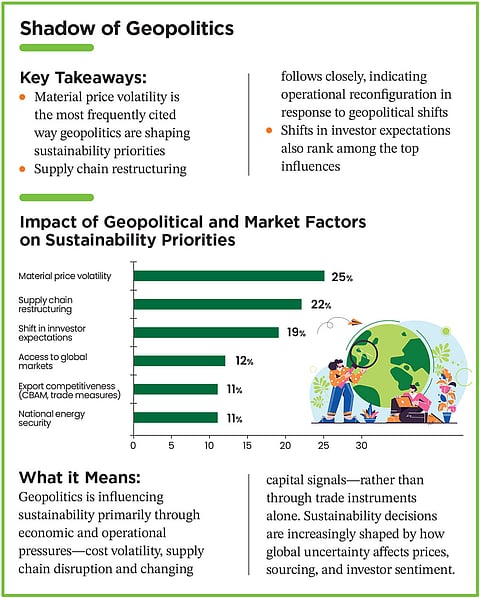

Over 70% of respondents from India Inc say geopolitics is influencing sustainability strategy, with supply chain disruption, price volatility and market access emerging as key concerns, as per Teri-Outlook Business survey

There is need to link net-zero targets with climate ambitions and financial planning

Advertisement

Take for example China’s decision last year to restrict export of rare earth elements. The shock waves were felt globally, including in India. Several auto players, like Mahindra & Mahindra, had to address rare earth magnet shortages, critical for electric vehicle production, by securing short-term alternative sourcing options. EVs are critical for M&M’s plans. The group has set a target of EVs accounting for 25% of total sales by 2028.

Just as businesses are no longer insulated from global power shifts, sustainability priorities are now directly influenced by global events. Irrespective of whether a business caters to domestic demand, or have cross-border exposure, corporate sustainability strategies must now contend not only with environmental and social objectives, but also with geopolitical realities, including access to capital and technology, evolving trade barriers.

“In a volatile global landscape, sustainability is no longer just a 'green' initiative—it is a resilience strategy. As energy and material markets fluctuate, resource efficiency and supply chain security have transitioned from operational tasks to core board-level priorities,” says Naveen Ahlawat, president and head of sustainability and decarbonisation at Jindal Steel.

Advertisement

Jignesh Sharda, chairman, Sustainability Council at RPG Group agrees with this assessment. Geopolitical changes have effectively turned sustainability from a linear “2030 roadmap” into a continuous exercise, where energy-security shocks, supply-chain disruptions, and shifting compliance expectations affect both timelines and capital cost, he says. The RPG group has interests in tyre, infrastructure, pharmaceuticals, energy, among others.

Sustainability decisions are being shaped by how global uncertainty affects prices and investor sentiment

Butterfly Effect

Last month the US administration, in keeping with President Donald Trump’s love for fossil fuel, “officially terminated” Endangerment Finding (EF). The EF is a body of scientific studies that form the basis of determining the threat posed by greenhouse gases to the environment.

Businesses, including those beyond the US borders, are anticipating a hit on investor sentiments for clean-tech technologies, including renewable energy, electric mobility and climate-tech solutions. Analysts at Environmental Defense Fund estimate that the EF repeal could lead to a staggering $1.4trn in fuel costs up till 2055.

For India, the implications are more indirect than direct. Global capital flows may become more cautious in the short term, affecting financing for large-scale climate infrastructure. Technology and supply chain geopolitics could intensify, particularly in batteries, critical minerals and clean manufacturing.

Advertisement

The “Teri-Outlook Business Chief Sustainability Officers’ Survey on Sustainability Leadership & 2030 Outlook” showcases corporate India’s dilemma. Over 70% respondents say geopolitics has moderate to significant influence on their organisation’s sustainability strategy and decision-making for 2030.

Survey respondents consistently identify price volatility, supply chain disruption and market access constraints as the most immediate ways in which geopolitics is affecting sustainability-related decisions. This mirrors broader global developments, where energy security concerns, resource nationalism and shifting trade alliances are reshaping cost structures and operational feasibility across sectors.

A recent study by government think tank NITI Aayog, Scenarios Towards Viksit Bharat and Net Zero–Sectoral Insights: Industry, too captures this mood. “India stands at a strategic crossroads in the evolving global industrial landscape. Geopolitical shifts, the restructuring of global value chains and a global push toward sustainability are driving demand for resilient, diversified and low-carbon manufacturing hubs,” the study notes.

Delving into the interplay between geopolitics and sustainability, the study highlights how the global shifts in trade, energy and industrial policies impacts India’s sustainability goals. For instance, levies under European Union’s (EU’s) Carbon Border Adjustment Mechanism (CBAM) on imports like steel, aluminium and fertilisers, is creating a global push for decarbonisation.

Advertisement

“India must align its industrial practices with global standards to maintain competitiveness in international markets,” the Niti Aayog study adds.

Events like the EU's carbon tax regime is influencing decision making in India Inc's boardrooms

Carbon Footprints

However, that’s easier said than done. An analysis by S&P Global, an analytics firm, on the impact of CBAM estimates at least $15bn in added import cost of goods originating in more carbon-intense countries. This could reshape global supply chains by encouraging EU importers to pivot to suppliers with smaller carbon footprints. The CBAM regime went into full effect from January 1.

“The CBAM and disclosure regimes such as the Corporate Sustainability Reporting Directive ensure that carbon intensity will increasingly affect market access. Sustainability, therefore, is becoming more about competitiveness,” says Santhosh Jayaram, adjunct professor of practice at the School of Sustainable Futures, Amrita Vishwa Vidyapeetham.

In the US, political polarisation has led to what many describe as “green hushing”. Chief executives are less vocal about ambitious net-zero pledges. However, the underlying market expectations have not weakened. “Large global buyers continue to demand lower-carbon products and transparent supply chains. For export-oriented Indian companies, that pressure remains real and commercial,” adds Jayaram.

Advertisement

A spill-over effect of the decarbonisation drive is visible on global availability of scrap steel. Use of scrap steel is one of the cheapest ways to reduce dependence on virgin iron ore and bring down carbon content in steelmaking. Over the past four years at least 48 countries have put restrictions on export of scrap steel, largely to make them available to domestic industries.

For India, ready availability of scrap steel is crucial for success of its decarbonisation strategy in steelmaking. The country is already the second-largest importer of scrap steel globally. Plans are to enhance scrap usage in steelmaking from current levels of 20% to 50% by 2047.

However, globally scrap availability is estimated to tighten by 15% in 2030. That could have a bearing on price competitiveness of Indian steel in global markets.

“India has to wait to generate its own scrap domestically as steel consumption grows,” says Prabodha Acharya, group chief sustainability officer, JSW Group, that has interests in steel and cement industries.

Businesses are still trying to figure out impact of climate change causing more frequent and extreme weather events. Corporate progress on climate adaptation remains slow

Green Transition

S&P Global's Top 10 Sustainability Trends to Watch in 2026 points out that the world is heading towards an increasingly fragmented, multiregional approach to action on sustainability. “Divergent approaches to energy and climate by the world’s largest economies dominate the narrative,” the report said.

Businesses are still trying to figure out impact of climate change causing more frequent and extreme weather events. Corporate progress on climate adaptation remains slow. According to the S&P Global Corporate Sustainability Assessment, in 2025 only 42% of companies (out of 6,751 surveyed) disclosed climate adaptation and resilience plans. Less than 500 Indian companies have committed to science-based emission reduction targets—of which just 249 are validated by Science Based Targets initiative (SBTi). SBTi is a global body that validates corporate emissions reduction targets and around 10,000 companies are registered with it.

Clearly, there is need to link net-zero targets with climate ambitions and financial planning. Aligning targets with capex allocation, technology choices and R&D investments is critical to demonstrate how transition commitments translate into real business decisions.

Moreover, transition cannot just be a narrow view of decarbonisation—it needs to be broader on sustainability. “The top 200 listed companies in India respond very differently on sustainability compared to the next 200-500 companies,” points out an analyst.

Changing Perceptions

There is a clear shift in investor expectations on corporate sustainability practices. Investors are maturing from giving credit for ‘long-term pledges like Net Zero by 2050’ to more ‘near-term performance’, such as percentage reduction in carbon intensity by 2030," says Hardik Shah, head–sustainable investment at DSP Asset Managers.

The weightage given to geopolitical risks in an investment portfolio has increased significantly. Topics such as supply chain concentration (such as, China +1 strategies) and resource security (such as, critical minerals for transition to RE) are now given more attention in sustainable investment assessments.

Shareholders too are asking tougher questions. There has been a clamour among shareholders for greater climate accountability at the US-based tech companies. Data centres are known to be power guzzlers. Massive expansion of data centres and increase in use of AI technologies have a direct impact on emissions and use of resources like land and water among others.

As India bets on attracting global data centres in setting up base in the country, the same questions would be asked of companies setting up such centres, and those using their services.

For corporate India, the sustainability journey towards 2030 is simply becoming more pragmatic, more regulatory and more closely tied to trade, finance and long-term competitiveness.