Beyond Geopolitics: What’s Blocking India Inc’s C-Suite from Achieving ESG Targets?

The Teri-Outlook Business survey reveals financial, regulatory and operational hurdles India Inc’s C-suite faces in achieving sustainability and ESG targets

Technology gaps, weak demand and lack of proven use cases are key barriers on the path to sustainability Designed by Freepik

Advertisement

Sustainability budgets are being directed towards areas with clear cost, compliance or revenue linkages

What it Means: Organisations are planning for measured, selective scaling, not step-change spending. The preference for renewables and circularity suggests that sustainability budgets are being directed towards areas with clear cost, compliance or revenue linkages, while market-based mechanisms remain supplementary rather than central.

Key Takeaways:

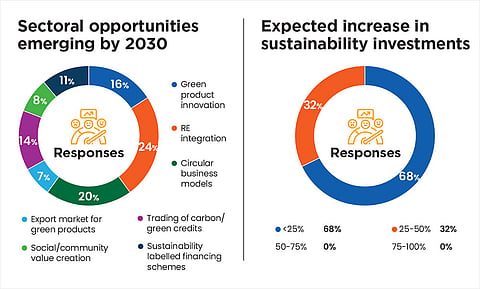

A clear majority of respondents expect modest budget increases, with over two-thirds indicating growth below 25% by 2030.

Renewable-energy integration is the most frequently identified opportunity, accounting for nearly one-fourth of responses, followed by circular business models and green product innovation.

Carbon and green credit trading appears in the opportunity set, but trails operational levers such as energy and material efficiency.

Technology gap is key barrier to 2030 sustainability target

Organisations are willing but not fully equipped to move faster

What it Means: The findings suggest that organisations are willing but not fully equipped to move faster. The constraint is not only access to capital or policy clarity, but the absence of mature technologies and market pull required to justify large-scale deployment before 2030.

Advertisement

Key Takeaways:

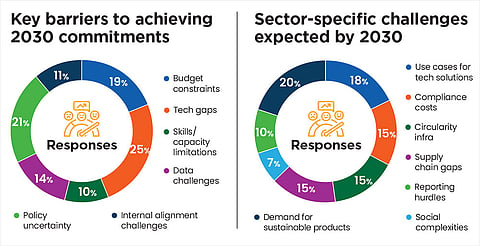

Technology gaps are the most cited constraint, followed by policy uncertainty and budget limitations.

Weak demand, lack of proven use-cases, and rising compliance costs lead to slow adoption.

Climate transition and physical risks are expected to intensify by 2030, supporting the sustainability goal.

RE incentives emerge as top priority to accelerate transition

Organisations seek a national sectoral road map

Sector-specific guidelines rank high for most organisations

What it Means: Sustainability leaders are signalling that implementation-enablers now matter more than intent. The emphasis on incentives, sectoral pathways and supply chain support points to a demand for policy clarity, financial support and ecosystem-level coordination, rather than additional commitments or targets.

Key Takeaways:

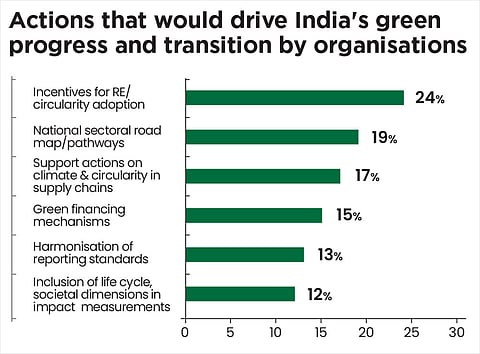

Incentives for renewable and circularity adoption are the most frequently selected action to accelerate green transition.

National sectoral road maps and pathways rank high, underscoring the need for clearer, sector-specific guidance.

Green financing mechanisms and harmonisation of reporting standards would support sustainability. So would leadership commitment and cross-functional coordination within organisations.

Corporate sustainability action must align with India’s SDG goal

Advertisement

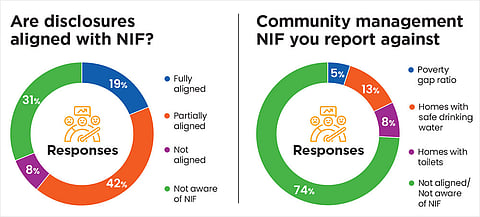

Most companies are not aligned or unaware of the government's SDG scoreboard—NIF

What it Means: Corporate sustainability efforts remain only partially connected to national SDG tracking. Without stronger alignment to NIF indicators—particularly beyond energy—corporate transition plans risk remaining inward-looking and difficult to aggregate into India’s broader 2030 progress.

Key Takeaways:

Close to 40% of respondents are either not aligned with or unaware of the National Indicator Framework, while only 19% report full alignment.

Reporting is strongest on energy-related indicators but drops sharply for circular economy and community-related parameters.

More than 70% report no alignment or awareness of community-management indicators under NIF.