West Asia conflict disrupts energy flows, hitting India’s fuel supplies and daily life

Rising crude prices threaten inflation, growth, and fiscal stability

Multiple global chokepoints expose India’s structural economic vulnerabilities

How the West Asia War Threatens India’s Goldilocks Economy

As war in West Asia chokes vital energy routes, India’s “Goldilocks” moment risks unravelling under the weight of rising prices, supply shocks, and hard policy choices

Representative image generated using AI

Summary

Advertisement

2025 may have ended as one of the worst for the global economy since the Covid-19 pandemic, with the United States (US), under President Donald Trump, throwing the world into a state of uncertainty and raising fears of a deeply disrupted global order.

Backers of the Indian economy, however, argued that India ended the year with flying colours, entering a “Goldilocks phase” of high growth and low inflation, in sharp contrast to the situation at the end of 2024.

As the country entered 2026, there was growing optimism that this momentum would sustain. And while things initially seemed to normalise, with India and the US moving towards a much-awaited trade deal, Washington’s priorities shifted by the end of February.

From arm-twisting its trade partners, the US moved to backing Israel in a military push to bring Iran's nuclear ambitions back under control. The headline of a trade war in 2025 has now changed to something far more ominous in 2026: the prospect of a world war.

Advertisement

Collateral Damage

India is no stranger to the economic fallout of major geopolitical events — be it the Russia-Ukraine war, Trump's 'reciprocal tariffs', China's rare-earth blockade, or indeed its own military standoff with Pakistan last year.

However, the US-Israel-Iran conflict feels closer, even though India is not even a party to it. Just days in, it already started affecting the everyday life of Indians, most visibly in their kitchens.

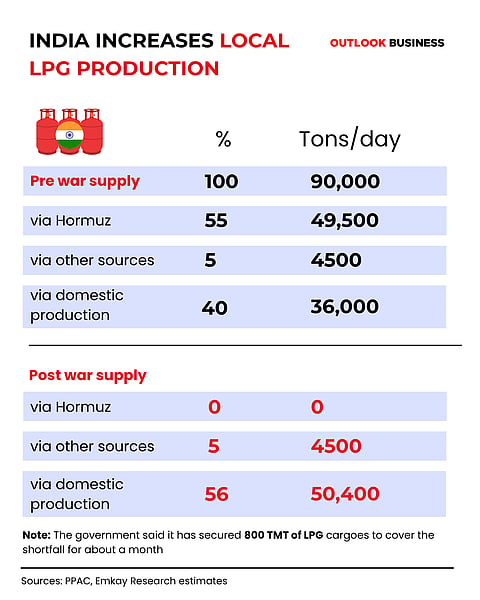

The disruption traces back to the Strait of Hormuz, a narrow passage that carries a large share of the world’s energy supplies and is now effectively shut. For a country that gets around 90% of its LPG imports through the strait, the impact has been immediate. The route also accounts for 54% of its crude oil and 60% of its liquefied natural gas imports.

With so much of the country’s energy lifeline tied to a single chokepoint, the disruption has manifested itself in the lives of ordinary Indians in the form of longer, uncertain waiting times for domestic cooking gas, and restaurants that have shut down due to lack of fuel.

Advertisement

Moreover, there seems to be no signs of respite on the horizon. With limited headroom to switch suppliers, the country’s ports are expected to receive only around 1.2 million tonnes of LPG in March, according to media reports, nearly 1 million tonnes lower than the 2.15 million tonnes it received in February.

The outlook for April points to a further squeeze. Incoming shipments are projected to fall again, with global loading sufficient to meet barely three to four days of the country’s demand, raising the risk that today’s disruption could deepen into something more prolonged.

Prime Minister Narendra Modi, in a statement in the Lok Sabha, his first in Parliament since the outbreak of hostilities, said India had faced similar challenges during the Covid crisis through unity, and must prepare to do so again. “With patience, restraint, and calmness, we must face every challenge. That is our identity, that is our strength,” he said.

Advertisement

Modi’s comparison with Covid is not accidental. In Surat, the LPG shortage has led to a large number of migrant workers thronging railway stations to return to their native villages in a scene reminiscent of the Covid chaos.

If constraints persist, economists warn that difficult choices will have to be made over how limited supplies are allocated between households and commercial users. The instinct may be to prioritise households, given the immediate impact on daily life. But a sustained squeeze on restaurants and firms would come at a greater cost. If businesses are deprived of LPG and gas for long enough, production and employment will begin to suffer, with the effects eventually circling back to households themselves.

“The first-order impact would stem from supply disruptions that could interrupt schedules and lead to export-order cancellations,” says Abhishek Bhattacharya, Senior Director for Corporates at India Ratings & Research. “Sectors heavily reliant on fuel, feedstock, or logistics are likely to experience stress within three months.”

Advertisement

This would prove to be too much for some businesses to endure. “If an establishment shuts down, and lets go of its workers, this process is often hard to reverse,” writes Sajjid Z Chinoy, Head of Asia economics at JPMorgan, in a column, pointing to the Covid experience. Disillusioned with cities, several workers across India have chosen not to return to urban hubs in the post-pandemic years, preferring to stay closer to their families. On the fiscal side, this has resulted in an increase in state handouts, even when work opportunities exist in cities.

Given India’s limited diplomatic success in persuading Iran to let her ships pass through, experts suggest that a meaningful way to cushion these disruptions is to scale up domestic capacity. That would mean boosting the domestic production of LPG, as well as those of alternatives like induction stoves. This can be done in a fashion similar to how the government subsidised the manufacturing of personal protective equipment in the early days of the pandemic.

According to a press release issued by the Ministry of Petroleum and Natural Gas, domestic refinery output of LPG, following the LPG Control Order, has been ramped up by 40%, taking daily LPG production to 50 Thousand Metric Tonnes or TMT, over 60% of India’s roughly 80 TMT daily requirement. This has reduced the net import requirement to about 30 TMT per day.

To bridge the remaining gap, the Ministry said it is securing cargoes from the United States, Russia, Australia, and other countries. But experts offer caution. “Supply outside the Middle East is unlikely to close the gap,” says Madhavi Arora, Chief Economist at Emkay Global Financial Services. “The potential supply shock is simply too large. Sustained losses from the region would overwhelm all available alternatives.”

More importantly, the volume constraints are only one side of the problem. India’s so-called “Goldilocks phase” is now running into price pressures as well, ones that could last well beyond the immediate crisis.

Price Pressure

Even if the situation in West Asia de-escalates, crude prices are likely to remain elevated, and this could lead to what economists call a terms-of-trade shock. In simple terms, India ends up paying more for what it imports without a matching increase in what it earns. For perspective, every 10 dollar rise in crude prices translates into a loss of about 0.5% of GDP for the economy.

Hence, what happens in a high-crude-price scenario is a difficult trade-off. The burden of higher oil prices has to land somewhere, and how it is distributed will shape the outcome for both growth and inflation. That choice of which one to prioritise — price stability or growth — rests squarely with policymakers.

One option is to shield consumers by not raising retail fuel prices. In this case, the hit is absorbed by oil marketing companies or OMCs, which either see their profits shrink or seek government support. This keeps inflation in check, but comes at a cost. Lower revenues or higher subsidies mean less room for public spending, which in turn weighs on growth.

The other route is to pass on higher prices to consumers. This eases the pressure on government finances and companies, but pushes up inflation and risks hurting demand and consumption.

So far, the government has maintained that it will shield consumers from rising fuel prices by cutting excise duties on petrol and diesel, even at the cost of its own finances.

In reality, the outcome could lie somewhere in between. As Emkay’s Arora puts it, the most practical approach in a prolonged crisis is to spread the burden across all stakeholders. “This could imply inflation hit to be sub-35bps, and OMC burden falling to 0.35% of GDP. However, the effective fiscal hit of 0.5% of GDP would crowd out other policy spending,” she adds.

It would leave the Centre with a difficult balancing act. The budget is already under pressure to generate enough resources to sustain growth, even as the government tries to boost consumption by putting more money in the hands of taxpayers.

Despite this dilemma, JPMorgan’s Chinoy argues that there is a stronger case for gradually raising retail prices of gasoline and diesel if global oil prices remain high. “..only if retail prices are slowly increased, to reflect global crude prices, will domestic economic agents scale back on energy volumes in response to higher prices. In effect, (lower) imported volumes can partially offset (higher) energy prices and provide some relief to the current account,” he writes.

On a positive note, the economy does have some room to absorb the shock, thanks to positive growth and inflation in the run-up to the disruption.

However, the same cannot be said about the country’s balance of payments. India’s current account deficit, which was expected to remain a manageable 1% of GDP in 2025–26, is now at risk of widening due to higher oil and gas prices, weaker remittances and softer exports to West Asia.

If crude averages around 85 dollars a barrel this year, the deficit could nearly double to about 2% of GDP, making it significantly harder to finance at a time when global capital flows are slowing.

So if prices are kept artificially low, consumption will stay high and the import bill will keep rising. Allowing prices to adjust, even gradually, helps reduce demand and limits the damage.

However, with assembly elections due in four states and one Union Territory in the coming weeks, the timing of any decision by the Centre to pass on higher prices to consumers will be closely watched, if it happens at all.

But the more delicate call may lie with the Reserve Bank of India. The rupee has been slipping to record lows, giving a chance to the opposition to use Modi’s own statements to attack him, given how he had viciously pounced on his predecessor for “failing to protect” the value of the rupee.

However, a weaker rupee, over time, can help narrow the current account deficit by making exports more competitive and imports more expensive.

The challenge then lies in how much the currency can be allowed to weaken. Too little may offer limited relief, while too much could worsen the problem by feeding into inflation rather than absorbing the shock.

Nonetheless, if the conflict drags on longer than initially expected, the Indian economy is likely to face far deeper shocks in 2026 than it did last year, largely because the pressures are now layered and reinforcing each other

One Chokepoint after Another

There is little clarity on how long the West Asia conflict will last, and even less on how long its economic effects will linger. What is clearly evident, however, is that the crisis has exposed yet another supply chain vulnerability for India, this time in energy.

Last year, China’s move to tighten rare earth exports disrupted production in India’s automotive sector, leaving the country with no immediate alternatives. Moreover, India’s lack of a significant leverage in response to the US’ reciprocal tariffs, in contrast to China’s strategic hold over these minerals, showed how exposed it remains in an increasingly fractured global order. India was forced to give in to pressure from the US to stop buying Russian oil.

The events prove that India’s global dependencies are creating multiple chokepoints. Whether it is energy imports, rare earth minerals or key industrial inputs, disruptions in one region or a shift in a trading partner’s policy choice are quickly cascading across sectors and human lives.

This has turned policymaking into a constant balancing act across foreign and economic policies. The present moment, therefore, calls for more than short-term fixes. It demands a shift towards building resilience, including ramping up domestic production and expanding strategic reserves of essential and critical commodities.

Economists say there is precedent for such course correction. After the Taper Tantrum in 2013, India moved to strengthen buffers and institutional frameworks to safeguard macroeconomic stability. The payoff is visible today in the role that foreign exchange reserves have played in cushioning the rupee against external shocks over the past decade.

As this year’s Economic Survey rightly notes, India is a country of 145 crore people seeking to become significantly more prosperous within a generation. It is trying to do so within a democratic framework in an increasingly uncertain global environment where each year seems to bring a disruption larger than the last. In such a setting, the margin for error is narrow.

Political leaders would do well to focus less on rhetoric and more on policy action that prepares the economy for shocks that are becoming less the exception and more the norm.