S Krishnakumar’s interest in equities began during his college days in the mid-80s. His uncle was a banker and in the evening he and his friends who would discuss stocks and the market in general. Krishnakumar would hear about how much money they had made. IPOs were the flavour of the season then. Krishnakumar’s first few investments were IPOs since they were considered cheap and information about them were readily available.

After completing his engineering in 1988, he joined Lucas TVS, a TVS Group company that manufactures automotive electrical systems. While working, as he pursued a part-time MBA in finance and portfolio management, his interest in investing kept growing every passing day. So, the next natural move after completing his MBA was to quit Lucas to join Anush Shares & Securities as a research analyst in 1995. His engineering background and several years of experience with the auto component manufacturer gave Krishnakumar a natural edge in analysing the auto and auto components industry. It was here that he made his first secondary market investment. “There was a company called SRF Nippon Denso which competed with Lucas-TVS. They were strong in technology thanks to the Japanese partner Nippon Denso, but were operationally very weak. They were not able to scale up but the product and the technology was very good,” says Krishnakumar. It was a loss-making company and the stock was available at Rs.7. “I believed a turnaround could create huge value. The idea was to buy and hold on till somebody bought out the domestic promoter,” adds Krishnakumar. Denso finally bought over the Indian promoter and the company became its wholly-owned subsidiary, Krishnakumar sold the stock post the takeover, making almost a 10x return.

While Krishnakumar developed competence around the automobile business, working in a three-member analyst team meant he had very little option but to track multiple sectors. “Even if a person went on leave or someone put in their papers which happened often, I ended up taking up more sectors. But I enjoyed doing that since I was developing a diverse knowledge base,” says Krishnakumar. It paved the way for a bigger role for him, as he was later promoted as the head of research at Anush. “We were closely tracking small and midsize companies, particularly in the south. As the number of institutional investors grew, our knowledge about these companies became an advantage,” says Krishnakumar. The brokerage was soon empanelled with institutional clients such as Sundaram Mutual Fund, Morgan Stanley, ICICI, LIC and many others.

2 March 2026

Get the latest issue of Outlook Business

After Anoop Bhaskar joined Sundaram Mutual Fund, the fund was looking for a candidate who could assist him to launch a mid-cap fund. Krishnakumar, who was already in touch with the team at Sundaram and had an extensive understanding of mid and small cap stocks, became the natural choice.

Different perspective

After spending eight and a half years on the sell-side, Krishnakumar found working on the buy-side a completely different experience. “As an analyst, you can go wrong and change the assumptions, but as a fund manager when you are handling public money you do not have that luxury,” he says. So he spent the initial few years learning the rules of the game and it helped to have one of India’s best fund managers on his side. “I learnt a lot from Anoop. He is very detail- oriented and meticulous. He spends lot of time reading balance sheets and what numbers convey as against what is written on the page…he interprets numbers very well,” reminiscences Krishnakumar. For instance, Bhaskar was one of the earliest to identify winners such as Unitech and Ansal. Incidentally, in 2005-06, when land prices were moving up and builders were left with huge inventory, he was one of the first to spot that the industry was heading for trouble. He would look at customer advances to visualise the growth in revenue and profit of these companies. “A thorough analysis of the balance sheet, understanding and interpreting the financial implications of each of these numbers was something really worth learning from Anoop,” points out Krishnakumar.

Over time, Krishnakumar developed his own investment framework. A five-step framework that comprised: scalable opportunity, sound management, sustainable competitive advantage, strong cash flows and RoE. He also looks at a company’s ability to grow over the next three to five years and compares it with its current market cap to assess at what level can the stock trade in the future given its growth assumptions.

Apollo Hospitals was one stock that ticked all these boxes. “We knew there will be an increasing demand for quality healthcare with rising affordability. It has built credibility and a good brand for itself in the organised space. Given its track record, pricing power, margins and growth potential, we were quite optimistic that it can actually become a large cap.”

Krishnakumar prefers to cap the exposure to individual stocks at 5-6% of the total portfolio. So, the decision to sell a particular stock is either when it crosses that exposure level or valuation turning expensive. Take the case of Bosch. The fund bought the stock in 2010 at Rs.4,900 and exited completely at Rs.20,700 in December 2014.

The decision to sell also becomes easier when the original premise of the investment changes. “If the basic premise of the investment no longer holds true we tend to exit the stock,” mentions Krishnakumar. For instance, the fund bought one of the leading wind energy companies (Inox Wind) as a lot of incentives were being doled out to the wind power sector and huge investments were being made by companies wanting to claim the tax benefits. When solar power became more viable, a lot of businesses shifted to solar energy. “Demand was not growing, SEBs were not paying them on time, leading to slower growth in revenue and profit. We completely exited the stock,” reveals Krishnakumar.

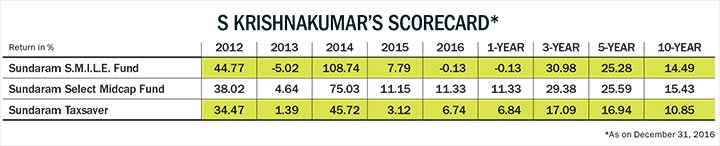

Sundaram Rural India Fund, which has generated a return of 33.77% in the last one year and 29.11% over the past three years, is another scheme that Krishnakumar manages. Some unconventional bets have helped him generate these stellar returns. For instance, investors stayed away from Heritage Foods because of the political risks associated with the company as it is promoted by Chandrababu Naidu, the chief minister of Andhra Pradesh.

“We were one of the early investors in the company. Investors didn’t want to enter the stock because of the political connection. But contrary to investor concerns, the company brought in professional management to run the business. We believed that buying packaged milk will become the norm. We were already seeing people slowly moving to packaged milk,” says Krishnakumar. That apart, the company is also gradually expanding to other states such as Tamil Nadu, Karnataka, Kerala, Maharashtra and NCR region. “This will give it the desired scale and growth,” adds Krishnakumar.

According to him, this was the period that the government was allowing the private sector to enter the dairy space and he believed that players with good established brands will help improve pricing power. He was also betting on the fact that value added products like ghee, cheese, butter and other products will generate higher margins and profitability for the company. The fund made its first investment when the stock was trading at around Rs.300-350. His conviction paid off and the stock is now trading at Rs.1,200.

Buying into cyclical businesses is not always this easy but Krishnakumar managed to learn the winning trick there as well. His bets on sugar stocks for the Rural Fund paid off rather well. It was both a combination of an upturn in the cycle and some stocks being available below replacement value,” says Krishnakumar. The global demand-supply was getting better, which meant higher sugar prices for the coming year.

The Rural Fund has in the past one year invested in companies like Dhampur and Balrampur which have done really well. “In some companies where we invested, the replacement value itself was 2x of the market cap at that point in time,” he says.

Learning curve

Not all bets have paid off though. Take the case of some of his power, engineering and infrastructure bets including Crompton Greaves, TD Power, and Gammon Infra where initial expectations never played out due either owing to policy changes or inaction. “An important learning for us from the previous slowdown has been that we have to be cautious while investing in businesses that are closely linked to government policies. While infrastructure may be a great top-down opportunity, it is quite possible that you will not make money investing in some of these stocks,” says Krishnakumar. For now he is betting on a few EPC firms which do not rely too much on funding, have an asset light business and have shown good execution capabilities.

Rural markets and agriculture as a theme is something that Krishnakumar is now betting on, because of the changes that the sector is undergoing. He believes government emphasis on agriculture and driving rural income higher will drive demand. “The government is connecting farmers and mandis with the market place, thus enabling farmers to get the right price and reduce arbitrage enjoyed by middlemen,” he says.

He believes the government’s initiative to pay crop insurance (75% premium is paid by the government and the balance by farmers) will bring in a lot more stability to incomes of farmers. “If there is more prosperity, more jobs and more income, there is bound to be a positive impact on sectors such as automobile, white goods, and FMCG,” says Krishnakumar. He is betting on the fact that demonetisation has resulted in a large part of rural India coming into the mainstream banking system. Besides, as a long-term investment theme, he is also betting on farm automation and the agriculture inputs space.

In an investment journey spanning over three decades, Krishnakumar’s ability to analyse, understand and interpret various sectors has helped him outperform on a consistent basis in the past. It’s unlikely to be any different in the future.