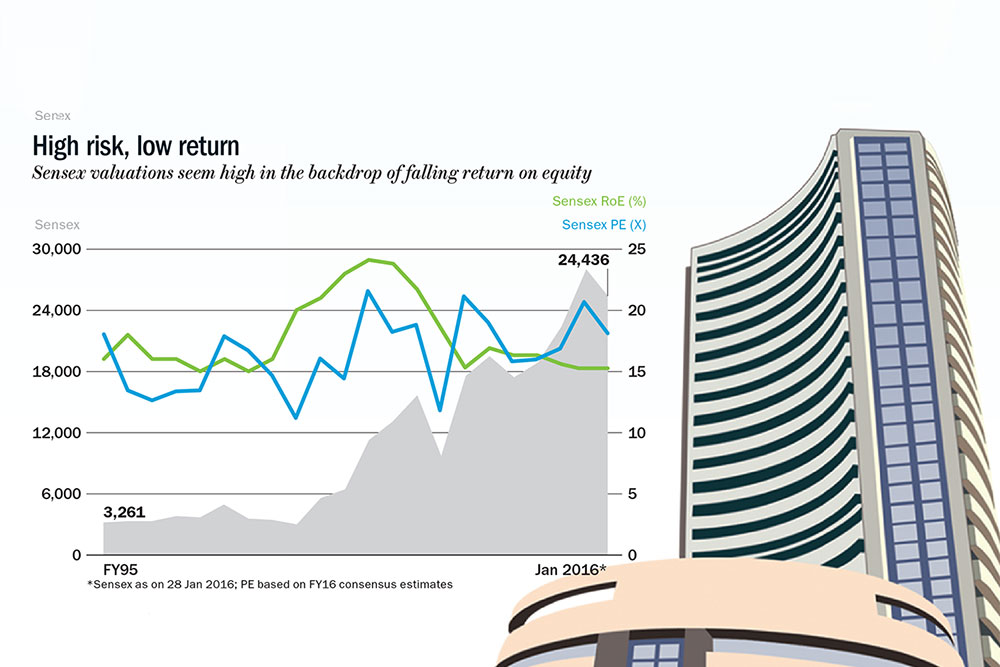

Even as markets remain tentative, with every step forward followed by two steps backward, how badly are stocks placed fundamentally? A quick look at the Sensex return on equity (RoE) chart shows that over the past 20 years, there have been only two occasions — FY01 and FY10 — when this ratio dipped to as low as 15%. And now, for the third time, RoE will hit an all-time low on the back of poor financial performance of companies. RoE, a figure that measures the final return earned by shareholders after all expenses — including interest cost — are accounted for, is derived by dividing net profit by shareholders’ equity. It is one of the most important metrics from a shareholder perspective and is a key determinant of equity valuations. The high RoE earned by Indian companies is one the main reasons why Indian stocks have enjoyed higher valuations. Typically, stocks with consistently high RoE tend to attract higher valuations.

The last two times that RoE dipped below 15%, the economy was going through severe contraction. But both those times, RoE bounced back within a year, and stock prices began their next surge the year after. In 2010, India’s economic growth had plunged to 6.8% from the high of 9.6% in 2007. In this period, the Sensex earnings per share (EPS) had marginally dipped from Rs.833 in FY08 to Rs.829 in FY10. However, between FY10 and FY13, Sensex EPS grew by 42%, ensuring a 200 basis points recovery in RoE. Similarly, in FY01, India’s economic growth had hit the low point of 4.4% compared with 6.7% in FY99. This slump was a result of the poor monsoon impacting domestic economic growth, exacerbated by a slowdown in the world economy after the tech bubble burst. While this impacted Sensex earnings and RoE, once the recovery started, earnings jumped 25% by FY03, and RoE recovered to 20%. Led by a global boom thereon, earnings accelerated, resulting in a steady rise in RoE and an accompanying rally in stocks, till the 2008 global crisis hit the brakes on growth.

Most of the companies on the Sensex that are eroding RoE today are from the energy, commodities and engineering space, though that is not to suggest that domestic consumption is not affected. “Today, RoE is impacted because of external factors such as commodity prices and exports. Close to 50% of the Sensex revenue is linked to the commodities space. And if we take others like exports into account, that exposure goes to close to 60%. Considering these facts, it was quite obvious that RoE would fall,” says Vinay Khattar, senior vice-president and head of research, Edelweiss Financial Services. Based on FY15 numbers, out of the Sensex 30 companies, 13 have an RoE of less than 15%, including loss-making Tata Steel with an RoE of negative 11%. These 13 companies cumulatively have 35.14% weightage on the Sensex. The prime reason for worry is demand, which has dragged down both realisations and capacity utilisations. About 11 of the Sensex companies (except banks) that have less than 15% RoE had an average asset turnover ratio of 0.74x compared with 0.84x in FY14 and 0.88x in FY13. Reliance Industries, Tata Steel, L&T and BHEL have all seen a large drop in asset turnover, indicating that their assets are less utilised compared with the past.

Most of the companies on the Sensex that are eroding RoE today are from the energy, commodities and engineering space, though that is not to suggest that domestic consumption is not affected. “Today, RoE is impacted because of external factors such as commodity prices and exports. Close to 50% of the Sensex revenue is linked to the commodities space. And if we take others like exports into account, that exposure goes to close to 60%. Considering these facts, it was quite obvious that RoE would fall,” says Vinay Khattar, senior vice-president and head of research, Edelweiss Financial Services. Based on FY15 numbers, out of the Sensex 30 companies, 13 have an RoE of less than 15%, including loss-making Tata Steel with an RoE of negative 11%. These 13 companies cumulatively have 35.14% weightage on the Sensex. The prime reason for worry is demand, which has dragged down both realisations and capacity utilisations. About 11 of the Sensex companies (except banks) that have less than 15% RoE had an average asset turnover ratio of 0.74x compared with 0.84x in FY14 and 0.88x in FY13. Reliance Industries, Tata Steel, L&T and BHEL have all seen a large drop in asset turnover, indicating that their assets are less utilised compared with the past.

For RoE to recover, strong earnings growth is necessary. In the first half of FY16, the Indian economy grew by 7.2% and is expected to grow in the region of 7-7.5%, which is again almost similar to 7.3% GDP growth in FY15. This is also reflected in the Sensex earnings for the current fiscal — the consensus Sensex EPS growth and RoE is expected to remain flat or slightly better. Currently, the consensus is for better earnings in FY17, with the Sensex EPS growth projected in the region of 18-20%. Importantly, a large part of this is projected to come from cyclicals — including commodities — where analysts are building in some recovery in demand and prices, particularly in the metals and energy space. “I think the positive impact of spending on infrastructure and the focus on manufacturing, along with the stabilisation in commodity prices from hereon, will help in better earnings and cash flows over the next 12-18 months. When cash flows start to improve, the interest burden will ease and that will also in turn boost profitability and return on equity,” asserts Khattar.

2 March 2026

Get the latest issue of Outlook Business

Most analysts are hoping for a recovery from here on, as they predict better profitability in 2017 led by higher economic growth. Saurabh Mukherjea, CEO, institutional equities, Ambit Capital, agrees, “RoEs will certainly improve from the current levels. There is a fair chance of RoE bouncing back, with the cyclical and commodities spaces showing some recovery. Our sense is that it will start to reflect in the calendar year 2017.” But that prognosis has a caveat built in: if there are external shocks, particularly because of lower commodity prices and China, analysts do not rule out further deterioration in Sensex RoEs. “Today, we are much better off compared with the last two times this happened — both the fiscal deficit and inflation are under control. We have low interest rates and are growing reasonably. But then, the fear today stems from external factors. If China collapses, we might have a situation that is worse than 2008-09, and in that case, it is quite obvious that RoE will fall further,” says UR Bhat, MD, Dalton Capital Advisors.

The only silver lining, however, is that falling return ratios are not only in the case of Indian equities, but across all world markets. Other emerging markets such as Brazil and Russia have been battered because of their high exposure to commodities. In that sense, Indian equities may be slightly better poised, but the lower ROEs only mean that current valuations cannot be justified fundamentally.