Twenty-six-year-old Nikhil Tyagi, a digital marketer working in Delhi, says he never thought of investing in fixed deposits (FDs). He puts all his savings in stock markets and mutual funds (MFs), encouraged by the 29% returns he has earned so far.

Lucknow-based Rakesh Mishra (name changed), 55, does not invest more than 40% of his total savings in MFs and stocks and has a good amount of savings in FDs, public provident fund and other traditional instruments. However, in the last one year, he has withdrawn a substantial amount to invest in real estate, confident that it will give good returns in the long run.

Tyagi and Mishra mirror the sentiments of an increasing number of people who are willing to trade the safety of bank deposits and their low returns for more profitable, even if riskier, assets. They do not believe traditional investment instruments offered by India’s banking sector can deliver the returns they want in the long run. However, for the banks, this public wisdom means a threat to their growth prospects—deposits are good sources of bank lending.

Not Quite Lucrative

1 June 2026

Get the latest issue of Outlook Business

At a time when inflation has been in the range of 5%–6%, average returns offered by banks on several instruments range from 3%–9%. On the other hand, stock markets are witnessing a prolonged bull run. Benchmark Nifty delivered over 20% returns in 2023. The number of demat accounts in the country has increased from four crore in April 2020 to 15.4 crore in April 2024.

The net financial savings of Indian households fell from 11.5% of GDP in 2020–21 to 5.1% of GDP in 2022–23. As per Reserve Bank of India (RBI) data for households, banks received Rs 12.4 lakh crore as deposits in 2020–21. This figure fell to Rs 10.2 lakh crore in 2022–23. At the same time, investment in MFs increased from Rs 64,000 crore in 2020–21 to Rs 1.7 lakh crore two years later.

Meanwhile, data from real estate intelligence firm Colliers-Liases Foras showed that the average per square foot prices of homes in major cities like Delhi, Bengaluru and Kolkata jumped by over 30% between 2021 and 2023. An SBI Research report said that the share of financial savings in physical assets was expected to reach 70% in the total household savings in 2022–23 from 48% in 2020–21.

Amid high growth in the economy and resilient credit demand, the pressure on banks is coming from their inability to attract deposits.

The Deposit Crunch

There have been two noticeable trends in the banking sector from 2021–22. One, credit in India is rising at a rapid pace. In the last two financial years, S&P Global Market Intelligence data shows, the credit growth of scheduled commercial banks in India has touched 17.4% and 16.3%. This has been attributed to the strong momentum available in the economy, with gross domestic product (GDP) growth above 7% consistently.

However, the banks have not been able to attract deposits at the same pace. The gap between credit growth and deposit growth stood at 3% in 2021–22, 6.4% in 2022–23 and 4% in 2023–24. Since the 2008 global financial crisis which shook up financial institutions, deposits in India’s banks have never lagged credit growth by such a wide margin for a stretch of three financial years.

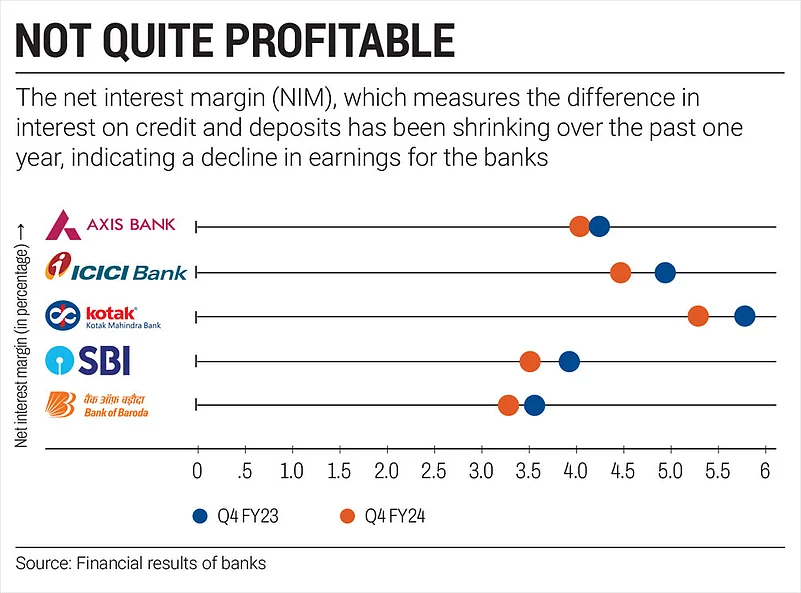

The primary earnings model of banks in India is dependent on the difference in interest offered on deposits and interest levied on credit, because of which the gap is of significance. The net interest margin (NIM), which measures the difference in interests on deposits and credit, has been shrinking at several banks for the last one year. Between March 2023 and 2024, HDFC Bank’s NIM slipped from 4.1% to 3.4%, Axis Bank’s fell from 4.2% to 4.1% and that of ICICI Bank fell from 4.9% to 4.4%.

Deepali Seth Chhabria, associate director for financial institutions at S&P Global Ratings, says, “Deposits are lagging behind loans as some of the savings are being channelled into MFs, equity investments and real estate. This has led to the deterioration in the loan-to-deposit ratio, creating liquidity issues for banks. To put it in perspective, Indian investors’ holdings in mutual funds rose 43% year-on-year [YoY] in the last fiscal.”

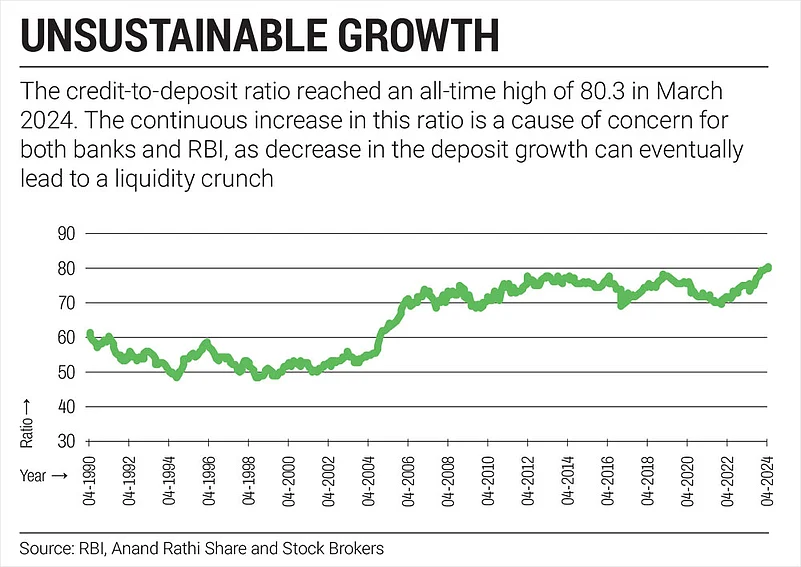

The loan-to-deposit ratio (LDR) reached an all-time high at 80.3% in March, according to data compiled by brokerage Anand Rathi Share and Stock Brokers. This figure has remained in the range of 65%–75% over the past 20 years. While the problem of high LDR was limited to private sector banks in the past few financial years, public sector banks too are now witnessing pressure in attracting deposits.

S&P data shows that State Bank of India, India’s largest bank, saw an increase in its LDR from 67.5% at the end of financial year 2021 to 74.7% by the end of December 2023. A similar rise of about 6%–7% was seen in other public sector banks like Bank of Baroda, Punjab National Bank and Canara Bank.

In January, The Financial Express reported that the RBI had raised concerns about high LDR ratio of some banks. As India’s regulations require banks to set aside some funds for buying government securities, high amount of funds tied up in credit can make things difficult for the sector.

A higher-than-desirable LDR directly affects the banks’ ability to lend effectively. RBI data shows that banks issued certificates of deposits to raise Rs 6.2 lakh crore between April 2023 and January 2024, a rise of 15% compared to the same period last year. However, a cause of concern for the banks is the rising cost of funds on account of the increase in the interest they have to offer. From 7% in mid-September, the interest rate on three-month certificates of deposits increased to 7.8% by February 2024.

New World Problem

As per RBI data, the weighted average domestic term deposit rate (WADTDR) on fresh deposits increased by 14 basis points in the 12 months through March 2024 at 6.4%. This is an attempt by the banking sector to attract deposits. Several commercial banks have also resorted to increasing FD rates, a popular investment instrument. Ranging from 7%–8% in several private banks depending on the tenure, FD rates are at a decadal high amid an inflationary environment.

But the rush towards depositing money in banks has still not returned to the pace the big players are targeting. The current account savings account (CASA) deposits to total deposits ratio, an important metric which measures the availability of low-cost current account deposits and savings account deposits, highlights this situation. The CASA ratio dwindled to 40.1% at the end of last year from 42.8% in 2022. The latest quarterly results have not brought a relief on this front. On a YoY basis for the March 2024 quarter, the ratio declined by 6 percentage points for HDFC Bank, 4 percentage points for Axis Bank and 7.3 for Kotak Mahindra Bank, among others.

“The bull run in the stock market has resulted in a lot of money flowing through SIPs [systematic investment plans] or via other means in the markets. This could be posing challenges for the banking sector as they need to mobilise deposits at a time when other avenues have given more returns,” says Dnyanada Vaidya, banking, financial services and insurance analyst at Axis Securities.

Devarsh Vakil, deputy head of retail research at HDFC Securities, says that the trend could only become bigger. “[The trend of] people shifting from fixed-interest instruments towards market and equity-linked options was majorly fuelled by high returns witnessed during the post-Covid market rally. As retail investors become more mature, their inclination toward equity-linked instruments will grow, especially among younger individuals starting their financial journey,” he says.

With no such product in the arsenal which can compete with the sky-high returns of equity markets, banks must rely on the long-term stability they provide for investments.

Investing in stock markets has been made easy using digital channels with the help of smartphones, making it crucial for banks to offer their services smoothly and safely by leveraging technology. However, the digital transition has not entirely been smooth.

The recent RBI action on Kotak Mahindra Bank highlighted concerns that the investment in IT infrastructure development has not been robust. The RBI stopped the onboarding of new customers via the bank’s mobile and online banking platforms. Similar restrictions were imposed on Bank of Baroda’s ‘bob world’ app which accounted for 35% of additions in total fixed and recurring deposit accounts in the second quarter of 2023–24. This restriction was lifted recently after RBI was convinced about the measures taken by the bank. ICICI Bank also suffered a data glitch, leading to leak of data of 17,000 credit cards.

Pratik Shah, partner and financial services consulting leader at EY India, a consultancy, says that it is important for banks to get the digital channels right. “It is a matter of hygiene now. It is the only cost-effective way of connecting with a customer and servicing them. While banks have invested significantly in their digital channels, it is about time they put equal importance on regulatory and governance issues. In the new world order where digital is so dominant, not putting in place proper tech infra means that you lose the very ability to compete,” he says.

Amid a strong bull market, falling deposits, high competition and now a regulator unhappy with the effort by banks to build and maintain their tech infra, banks find themselves between a rock and a hard place. The question is, can they find a way that will be sustainable in the long run?

Facing the Challenge

The earnings call of several banks which recently announced the results of the fourth quarter of 2023–24 revealed that deposits and attracting new customers are on top of the minds of analysts and banks’ leadership. Axis Bank chief executive officer (CEO) Amitabh Chaudhry said, “We have been talking about it for quite some time that at some stage, the deposit growth and the credit growth need to converge. This gap cannot continue forever.”

The first line of action appears to be getting the tech infra right. Kotak Mahindra Bank CEO Ashok Vaswani told the media recently that the bank will invest Rs 1,700 crore to upgrade its technology. UCO Bank has also announced a Rs 1,000 crore to boost its tech infrastructure. SBI chairman Dinesh Khara said recently that the bank will hire over 10,000 engineers, a move that will aid its digital infrastructure needs.

EY India’s Shah believes that banks also need to make a strategic shift. “Merely focusing on CASA deposits is a conventional approach. Banks might do well to consider the entire portfolio of customer funds they manage. In a buoyant market, the goal should be to become the preferred banker and deposits will follow,” he says.

Banks are slowly taking note of this fact and working to increase their presence in the range of financial products which include United Payments Interface (UPI) payments and wealth management. Mobile banking apps which offer customers most of the existing financial solutions in the market are common now. Analysts assert that this will help in building a solution-oriented approach to establishing a relationship with customers.

One such indication of this strategy taking root in the sector is the amount of attention wealth management space is attracting.

Late last year, HDFC Bank launched its own trading app, known as HDFC Sky, to compete with the likes of Zerodha and Groww. Similarly, in July 2023, Business Standard reported that SBI appointed a consultant to deliberate over the revamp of its wealth management business. At the end of 2022–23, ICICI Bank had also set a target to double the number of wealth bankers to boost assets under management from clients.

The focus is also on expanding the branch network to win over new customers and increase visibility. HDFC Bank plans to add over 1,000 branches in calendar year 2024 and ICICI Bank plans to increase its presence by over 600 branches in 2024–25. Axis Bank informed shareholders recently that it added 475 branches in the last financial year to cross the mark of 5,000 branches.

Neeraj Sinha, partner and leader, financial services, BDO India, a consultancy, says that market capitalisation of stock markets and the country’s economic growth move in tandem. “In a high economic growth environment, people want higher returns. But the crucial factor here is trust. Indian banks will continue to deepen digital capabilities but with an enhanced focus, in parallel, on the physical expansion of their branch network, as these physical touch points bolster the element of trust when dealing with customer’s money.”

Sinha adds that in the long term, banks remain the custodian of people’s trust and the challenge from the bull market makes them sharper in their reach, approach and offerings.

Need for Caution

S&P estimates suggest that banks will have to slow down lending because the current gap with deposit growth is not sustainable. Credit growth is expected to slow down from 16% in 2023–24 to 14% in 2024–25. Moderating credit can help in easing the cost of funds and tightness in liquidity. However, the business of banks will be affected in such a scenario, which can create complications in the long run.

An analysis of 24 scheduled commercial banks data shows that profit growth of the banking sector is also slowing down, which will further impact the ability to grow credit lending activities. According to data from ProwessIQ, an interactive querying system, the YoY growth in aggregate net profit slowed down to 17% in the last quarter of 2023 from 34% in the preceding quarter.

For an economy growing at over 7%, any moderation in credit lending activities can hinder growth. Investors are closely watching the developments as banks struggle to attract deposits. While many remain bullish in the long-term, questions remain on how the sector will compete with the lucrative options of investment available elsewhere.

For Tyagi, Mishra and millions like them, greener investment pastures stand elsewhere, and one cannot hold them back from walking the more lucrative path. But for the banks, this poses a daunting challenge, one that does not have simple or straightforward solutions.