Every market that is rising quickly is not a bubble. And any market that has been rising for a long time and is not falling is also not necessarily a bubble. They could be, but you will never know ahead of time. Instead, why not just continue to follow the existing trends and not worry about bubbles

— GREGORY HARMON, founder, Dragonfly Capital Management

This pithy comment from the US-based options trader could well be running through the minds of Indian mutual fund (MF) managers given that the benchmark indices, the Sensex and Nifty, ended CY19 with 15% and 12% gains, amid growing dissonance between the economy and equities. The year gone by was marked by a 45-year low employment rate, seven consecutive quarters of falling GDP growth from 8.1% in Q4FY18 to 4.5% in Q2FY20, rising bad loans, and promoter defaults. Add to that, skeletons tumbling out of NBFC closets.

What’s more stark is that in the past decade, according to a Motilal Oswal Research report, Nifty earnings has not even doubled -— it stood at Rs.251 in FY09 and grew to Rs.481 in FY19, revealing a challenging business environment for India Inc. It’s not without reason. R Srinivasan, head-equity at SBI Mutual Fund, explains: “Corporate earnings, especially over the past five years, have been extremely disappointing owing to a breakdown in the correlation between nominal GDP growth (already impacted by lower inflation) and sales growth, a resultant negative operating leverage, high real interest rates and higher taxes as a percentage of sales. Monetary policy, for now, is easy and should address interest rates. If sales pick up, hopefully, the operating leverage will turn positive.”

Yet, the indices have been courting new highs — with foreign investors pumping in Rs.1 trillion into equities (a six-year high) and MFs mopping up stocks worth half a trillion in 2019. But what’s disconcerting is that amid the surge, the polarisation towards large-caps that existed before the Sebi reclassification move in 2017, has only gotten acute in the following years. To ensure uniformity across schemes and to make return comparisons accurate for investors, the regulator had introduced categorisation and rationalisation of schemes. Prior to the move, each fund house followed its own criteria and definition of market cap. Following the reclassification, as per reports, nearly Rs.8.5 trillion of Rs.9 trillion equity assets have been parked in the top 100 stocks.

Anoop Bhaskar, head-equity, IDFC Asset Management, expects the trend to continue. “I think large-caps will get more expensive before they correct. If you look at consumer staples, companies such as Nestle India or Hindustan Unilever are clearly trading one standard deviation higher than their past five-year average, which is a scary valuation level. The market has been cynical. So, anything that has had decent earnings growth has been rewarded disproportionately. The market is focused on next quarter’s earnings growth rather than long-term earnings.” In Q3FY20, fund managers raised stake in 17 Sensex heavyweights but pared stake in 12 scrips, including Reliance Industries, HDFC Bank, HDFC, TCS and Asian Paints. As per rating agency Crisil, large-cap and multi-cap funds cornered Rs.3 trillion of assets under management (AUM) in FY20, while mid and small-cap funds have AUM of just Rs.121 billion.

The corporate tax cut from 30% to 15% for newly incorporated manufacturing companies and 22% for existing domestic companies served as a further boost to large-caps. Shreyash Devalkar, senior fund manager, Axis Mutual Fund, points out: “CY19 was a flat year until the corporate tax cut happened. After the cut, the Nifty delivered 13% return.” Harsha Upadhyaya, CIO-equities, Kotak Mutual Fund adds, “The tax rate cuts are beneficial to large companies as they were paying full tax. So that’s what has created a market where a handful of stocks are trading at higher valuations.”

But what’s pertinent to note is that large-cap funds have been struggling to beat the benchmark total return index (TRI). For example, CY19 Sensex TRI has delivered 15.66% return, while the large-cap funds have managed 10.16%. Similarly, on a three-year basis, the benchmark TRI delivered 17.33% return against 11.38% by large-caps. But despite their weak performance and concerns over valuation, especially for FMCG stocks, it’s unlikely that large-caps will fall out of favour, given the increasing velocity of passive money. Nilesh Shah, managing director, Kotak Mutual Fund, says, “Last year, the Employee Provident Fund Organisation (EPFO) invested Rs.400 billion in equities, taking the cumulative flow over the past three years to around Rs.1 trillion. Since their mandate is only to invest in Nifty 50 exchange traded funds (ETF), imagine what will happen to large-cap stocks. For instance, irrespective of HUL’s valuation, by mandate, the ETF will invest in the stock. Further, if passive flows are going to continue, why would any investor sell?” The compulsion of maintaining a higher interest rate at 8.65% in a falling interest rate regime has prompted the EPFO to increase its exposure to equities from 5% to 15% recently, and it could possibly go up to 25%, thus increasing the quantum of flow into large-caps. Besides, the largest foreign ETF, iShare MSCI, which holds assets under management of close to $5.5 billion (Rs.400 billion), has also seen net inflows in CY19.

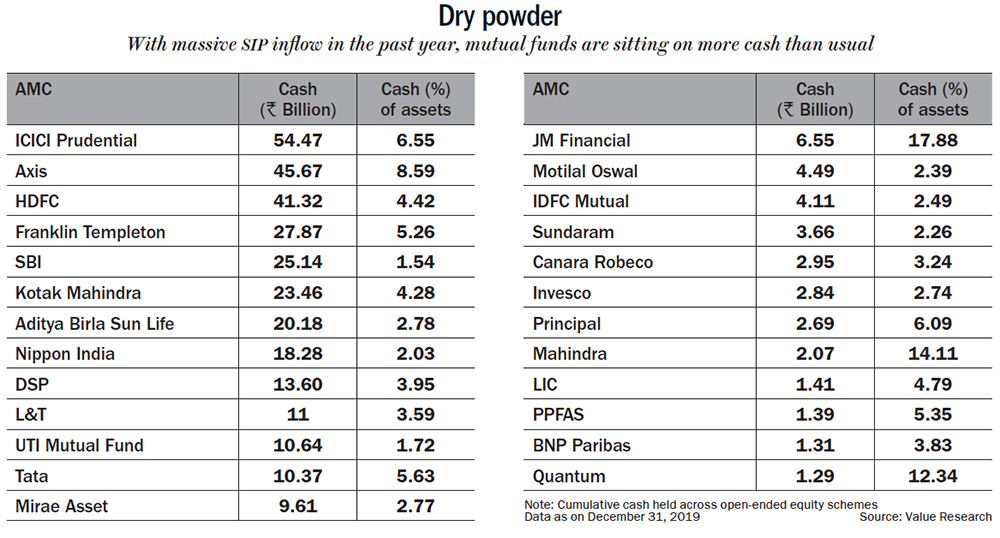

While the AUM of index and ETFs (excluding gold ETFs) has increased nearly 22x from Rs.75.66 billion in 2014 to Rs.1,660 billion in 2019, fund managers don’t see passive investing taking off in a big way and are looking at a universe outside of large-caps. A trigger for that could be funds seeing robust inflows through systematic investment plans (SIPs), which have more than doubled from Rs.417 billion in CY18 to close to a trillion (Rs.986 billion) in CY19. Besides, as per Value Research, taking Rs.1 billion as the cut-off, 25 fund houses were cumulatively sitting on nearly Rs.346 billion of cash, as of December 2019 (See: Dry powder).

While the AUM of index and ETFs (excluding gold ETFs) has increased nearly 22x from Rs.75.66 billion in 2014 to Rs.1,660 billion in 2019, fund managers don’t see passive investing taking off in a big way and are looking at a universe outside of large-caps. A trigger for that could be funds seeing robust inflows through systematic investment plans (SIPs), which have more than doubled from Rs.417 billion in CY18 to close to a trillion (Rs.986 billion) in CY19. Besides, as per Value Research, taking Rs.1 billion as the cut-off, 25 fund houses were cumulatively sitting on nearly Rs.346 billion of cash, as of December 2019 (See: Dry powder).

Beady eyes

Unlike the large-caps, the BSE MidCap and SmallCap Indices fell 3% and 8%, respectively, thus ending up with negative return for the second year in a row. That the going was tough in the mid and small-cap space is evident given that only 16 funds in the mid-cap category out of 26 were able to deliver positive one-year return and just two small-cap funds out of 21 managed double-digit return as of December 31, 2019. What’s more worrying is that though SIP flows have been robust over the past couple of years, investors are yet to see any return. Even on a three-year basis, as of 2019, as per Value Research data, against the average three-year SIP return of 1.33% in the mid and small-cap category, 13 of 36 mid and small-cap funds have shown negative SIP return, with just five funds managing less than 1%. It’s not without reason. “Frankly, it’s been a very polarised market, as good quality stocks have continued doing well even in the small-caps category with 30-50% increase in share price. Our absolute returns have been negative since the beginning of 2018 when the market breadth peaked out, but we’ve done better than the market maybe because we focused on capital-protection-type-ideas and relatively better quality businesses,” says Srinivasan of SBI Mutual Fund.

Devalkar, whose Axis Small Cap Fund topped the list with one-year return of 19.38% in the small-caps category, adds: “Mid and small-caps have underperformed large-caps. But if you look at the percentage of stocks performance-wise in each category, there has been a 30-35% success rate in all the three categories. It is just that the companies that have performed in the small and mid-cap categories don’t have enough weight in the indices,” he says.

Some top funds in these categories went with contrarian bets to better their chances. Case in point, Upadhyaya, who manages Kotak Equity Opportunities Fund. He moved out of consumption-related segments such as auto and went underweight on FMCG and consumer durables. Alternatively, Upadhyaya increased his mid-cap exposure from 35% in 2018 to 45% in 2019. According to him, the fund managed to achieve 19% one-year return, as of February 2020, against the Nifty 200 return of 10%. “Cyclical headwind was there, but we were sure that once this phase passes, the structurally good companies would do well. The valuations were attractive because the broader market had corrected quite a bit since the beginning of 2018,” reveals Upadhyaya. Further, the price and volume correction seen over the past couple of years has made the small-cap space attractive.

The share of small-caps in the overall market capitalisation is down to 13%, the lowest in the past five years. Finally, from its 2018 peak, trading volume of small-cap index is down 66%, which is close to the lowest it has hit in the past. Sensing undervaluation, four new-fund offers (NFOs) targeted at small-caps raised Rs.3.71 billion in 2019, and two more NFOs from ITI and IDFC have been lined up this year. “We believe, over a 10 to 12-year cycle, there has only been one block period of three years where small-caps were the worst performers. This is the second time that we are seeing two years of negative return. Given where the valuations are, we are at a similar stage to what we were in early 2013. After which we had a good rally in small-cap for three to four years,” explains Bhaskar.

While there is opportunity, the reclassification of small-caps has created a headache. “With the revised categorisation norms, the small-cap limit turned out to be higher than our internal definition. We had to re-open a fund we had closed long back for fresh flows,” says Srinivasan, whose SBI Small Cap Fund clocked an annualised return of 6.10%. He admits that his portfolio of 46 stocks is too vast and he would have ideally preferred 30 stocks in it. “But, we had to own a minimum of 65% in small-caps,” he says. Even as the fund managers gingerly explore options outside large-caps, there is not much change in terms of sectors preferred.

Hobson’s choice

Going ahead, fund managers unanimously expect consumption theme to do well, thanks to the rural economy. Last year, there was ample rainfall in various regions that helped improved crop yields. Overall consumption from the rural pockets, which covers roughly 55% of the population, account for nearly 35-36% FMCG sales, according to Vinit Sambre, head of equities, DSP Mutual Fund. Taher Badshah, CIO of Invesco, concurs, “Rural economy will be better than what it was in the past two years, simply because inflation, and particularly food inflation has come back and this will help in improving rural disposable incomes. Besides, improving government support to spending on rural welfare and employment programmes will support rural consumption demand.” In fact, consumption funds as a category dished out 13% return over the past one year. Devalkar calls his portfolio 100% consumption-based with a bullish bias on retail, consumer staples, jewellery and auto. He explains, “There will be cyclical ups and downs in particular segments, but broadly, the portfolio will be around consumption. Though there were some challenges in the discretionary part, surprisingly, now retail is doing much better than others.” The other factor that is expected to play out in the coming year is the base effect in sectors that have underperformed in the past year. For instance, if four-wheelers saw a decline of 10-15% last year, this year, it might see a recovery.

Despite the challenges in the banks and NBFC space, fund managers’ bets are equally high on financials. Most believe the sector is slowly recovering, especially after the government’s numerous policies to ensure the same. The government has been actively pushing banks to lend to NBFCs, which will aid in improving their liquidity. Further, insurance continues to be an underpenetrated segment with huge potential. “There is a clear market share shift happening from the PSBs to private sector banks. Apart from high quality NBFCs, insurance is one sector where there is a very long runway for growth. In terms of growth metrics, they are equal or better than private sector banks,” says Sambre. Incidentally, five bank ETF NFOs raised over Rs.3 billion last year. However, Bhaskar says that, in the first year, a large part of his ETF’s exposure will be through large-caps. “Most small-cap financials are NBFCs or smaller PSUs, which are under stress,” explains Bhaskar.

While slowdown has been the talk of the season, fund managers are also looking at gain in market share, which in the past couple of years has happened either through consolidation or organised players gaining at the cost of unorganised. Consolidation has largely happened in the financial, NBFC sectors and even in jewellery retail. “Success is also about consolidation rather than betting only on GDP and industry-specific growth. Industries where there hasn’t been much consolidation, you haven’t made money either. For instance, in the infrastructure sector, road sector’s execution was better and even orders were good. But because the sector didn’t really see any major consolidation, we haven’t seen profitability there,” mentions Devalkar. In the past six months, stock price of top road construction companies such as Ashoka Buildcon, Dilip Buildcon and KNR Constructions have been volatile as the NHAI continues to be neck-deep in debt.

Crystal ball gazing

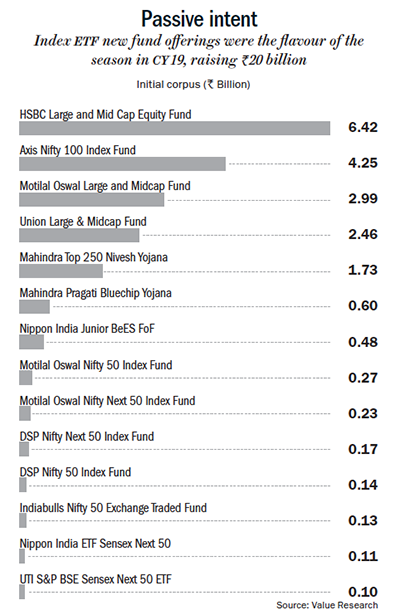

If investment return is any indication, in 2020 year-to-date, large-cap funds at 0.07% have lagged mid and small-caps, which have clocked 6.80% and 8.25% return, respectively. Even as Bhaskar is optimistic about his new small-cap fund, he adds a caveat. “Our weight on small-caps will never go to 100%. The maximum we will go is 80% and as valuation increases, we will reduce our weight in small-caps to 65-70% and increase cash to 30%,” cautions Bhaskar. As to whether large-caps or small-caps are better, nine NFOs have raised bulk of the money (Rs.42.17 billion) via multi-cap funds, which gives fund managers the flexibility to move across large, mid to small-caps. About Rs.20 billion of the new NFO money has gone towards Index ETFs (See: Passive intent), an indication that investors want to play it safe. Not surprising that fund managers have knocked on the regulator’s door to ease the strict classification criteria to help them in their chase for alpha. While no one wants to hazard a guess on the level of return they can generate, Upadhyaya strikes an optimistic note. “When you are coming out of a slowdown, obviously, it’s not going to be a V-shaped recovery. But there is money to be made when investing for the long-term. All one needs is to be patient.”